Your summary with links, if you’d like to curate your content:

Sod’s Law: Scenario Planning: Last week’s Iran crisis delivered an unscheduled stress test for global portfolios, highlighting the value of scenario planning as a strategic discipline. The key lesson is that complex systems react in messy, unpredictable ways, and a small shock in one area can cascade across interconnected markets, supply chains, and corporate strategies. Scenario planning is not about predicting events precisely but about building resilience to survive surprises.

The AI Bun-Fight (Anthropic & Pentagon) Anthropic’s Dario Amodei broke off Pentagon negotiations after demanding assurances that its AI would not be used for mass surveillance or autonomous weapons, and Defence Secretary Hegseth labelled Anthropic a “supply-chain risk.” Discussions have since resumed, and a resolution would allow military access to Claude while avoiding an official blacklist. Anthropic is valued at $380bn, on track for around $20bn in revenue, and recently topped Apple’s app download charts amid a surge of public support.

Trump’s Latest War: Iran Update. US-led strikes on Iran, followed by Iran’s attacks on neighbouring states, have created widespread market disruption and geopolitical uncertainty, with Trump already hedging on a 4-6 week timeline. The US dollar has strengthened as a safe haven, reversing two months of emerging-market outperformance and pushing currencies like the Indian rupee to record lows. Europe faces renewed energy price pressure, and emerging markets, including South Africa, remain vulnerable to dollar strength and capital outflows.

AI: Is My Job Safe? AI threatens not just individual jobs but entire business models, with the key difference from the 1990s internet boom being that it disrupts cognitive production broadly, not just information distribution. US labour productivity surged 4.9% in Q3 2025, with debate ongoing over AI’s contribution, while Jack Dorsey’s mass layoffs at Block signal what some believe is coming industry-wide. Whether AI proves pro-worker or destructive depends less on the technology itself and more on how leaders choose to deploy it.

NHI Update: Health Minister Motsoaledi continues to insist NHI preparation is proceeding “full force,” despite Ramaphosa freezing the proclamation of any NHI sections pending a Constitutional Court ruling in May. The NHI faces 14 court challenges, no budget allocation, and the practical impossibility of funding a scheme costing R450bn to R800bn+ annually without coalition support the ANC no longer has. The arrest of the Health Department’s Director-General for fraud this week further undermined the NHI’s credibility.

Is SaaS Dead? AI has raised fears that businesses could bypass SaaS providers by using AI to build custom software, causing significant derating of SaaS stocks like Fiserv. However, replacing deeply embedded, mission-critical business applications with AI-generated code remains largely impractical, and the question of accountability when things go wrong still favours established providers. NVIDIA’s Jensen Huang argues AI will more likely make SaaS companies more efficient as “agentic” operators rather than replace them outright.

This Week’s Roundup

RSA:

USA Markets & Economy

Global ex RSA/USA

Sod’s law – If it can go wrong, it probably will

Last week, with Trump’s impromptu war, portfolios around the world got an unscheduled ‘stress test’ – as did the investors.

One of the things we do as advisors and asset managers is ‘scenario planning’ – so we can perhaps put up some guardrails for when things go really wrong. I am not talking about trying to scenario-build for another Pandemic (but presumably governments are), that is, hopefully, once-in-a-century occurrence, but shocks that rattle markets, like The ‘Peace’ President cosplaying Lord Farquaad.

Over the past week, joint US and Israeli strikes on Iran, followed by Iran’s unexpected attacks on its neighbouring states, have shown how fast a “controlled and well thought out plan” (NOT) operation can change. You cannot predict every event or response, but serious planners should expect the system to react in messy and unexpected ways. That is the point of scenario planning – not to guess the exact move, but to be resilient enough to handle surprises and keep competing.

Scenario planning reminds us that organisations and individuals are not isolated machines. They are complex ecosystems connected by many interdependencies. Systems theory puts it simply: a small change in one part can affect the whole structure. The butterfly effect, if you will. This is a timely warning for leaders who still act as if their businesses are untouched by local politics, global shocks or supply chain disruptions.

Good scenario planning gives a more honest view. Local factors, such as labour issues, changing regulations, and weak infrastructure, combine with global forces, such as swings in commodity prices, geopolitical tensions and currency fluctuations. None of these works alone. They interact, change assumptions and shake the foundations of corporate strategy.

That’s why scenario planning needs to link directly to strategy cycles and budgets. It shows which strategic bets rely on optimism, which cost forecasts are unrealistic and which “non-negotiables” fall apart when outside factors change even a little.

When used well, scenario planning is a disciplined way to test how strong you or your company’s ambitions really are. In the end, scenario planning is just a way of admitting the obvious – what could go wrong, probably will.

Anyone who has been engaging with the various LLMs out there will be quite aware just how inaccurate they can be – it’s euphemistically called ‘hallucinating’. I, for one, would not trust an AI model to water my plants over the weekend, let alone ‘autonomously’ give a drone the decision to kill. Yes, we’ve reached the point where ‘Terminator’ level guardrails need to be put in place – and the US doesn’t want to be shackled. To be fair, the Chinese and others are probably already using AI to do exactly that. The ethics of AI is a budding discipline and way behind the curve.

Anthropic PBC chief Dario Amodei has resumed discussions with the Pentagon about the way its AI models are used by the US military, raising the possibility that the two sides can resolve a feud that’s transfixed Silicon Valley.

Amodei had been negotiating with Emil Michael, under-secretary of defence for research and engineering, to hammer out a contract governing the Pentagon’s access to Anthropic’s technology. But talks broke down last week after the startup demanded assurances that its AI wouldn’t be used for mass surveillance of Americans or autonomous weapons deployment. Defence Secretary Pete Hegseth then declared Anthropic a supply-chain risk, a designation typically reserved for US adversaries. (Watch this space, Hegseth might be next on the chopping block following the departure of ‘Puppy Killer’ Kristi Noam.

Discussions have since resumed, a person familiar with the matter said. If both sides strike a new agreement, it would allow the military to resume using Anthropic’s AI while lessening the risk that the Pentagon would officially blacklist the company. It could also complicate rival efforts: OpenAI last week announced it had struck an agreement to let the Pentagon deploy its artificial intelligence models in its classified network (resulting in a mass uninstall of its LLM by ordinary users). OpenAI chief Sam Altman later said he was working with the defence department to add more guardrails around surveillance.

A resolution would help clear the air around one of the artificial intelligence industry’s fastest-growing and most promising firms.

Anthropic — now valued at $380 billion — is on track to generate annual revenue of almost $20 billion, a projection based on current performance, more than doubling its run rate from late last year. The Pentagon dispute, however, has muddied the company’s outlook. Any long-term impact from the Pentagon’s declaration on Anthropic’s sales to enterprise customers – which has long been its core business – remains to be seen. In the meantime, it’s gaining traction with everyday users. Anthropic’s main app (Claude) recently topped Apple Inc.’s download charts, reflecting a surge of support for the company. Much of Silicon Valley also rallied around Amodei. Tech groups representing major companies, including Alphabet Inc.’s Google and Apple, are urging President Donald Trump to reconsider designating Anthropic a national security risk, arguing that it would cause detrimental ripple effects for the rest of the industry.

We’re now a week into Trump’s 5th ‘War’/’Bombing’/ ‘Military incursion’ in only this second instalment of the Kafkaesque Trump second term – three more years to go.

It’s still unclear whether the US can achieve the swift, conclusive victory it wants in Iran. Trump is already hedging his bets out at 4-6weeks. It’s very unclear what the future holds for Iran and its regime.

To fully understand some of the nuances, it’s important to understand some of the (vast) history of the region – specifically the animosity between the Shia (Iran) and Suni (Saudi, Iraq) varieties of the Muslim religion, not dissimilar nor less violent than the Catholic/Protestant rivalries that led to the ‘Troubles’ in Ireland.

The tension between Sunni and Shia Muslims goes back nearly 1,400 years and began as a political dispute over leadership after the death of the Prophet Muhammad in 632 CE. What started as a succession argument gradually evolved into theological, political, and cultural divisions that still influence the Middle East today. When Muhammad died, he hadn’t clearly designated a successor (at least not in a way everyone agreed on). As a result, two camps formed:

Sunni view:

Most of the community believed the leader should be chosen by consensus. They supported Abu Bakr, a close companion of Muhammad, who became the first caliph (political and religious leader).

Shia view:

Another group believed leadership should stay within Muhammad’s family, specifically through his cousin and son-in-law Ali. “Shia” comes from Shi’at Ali — “the party of Ali.”

Ali eventually did become the fourth caliph, but the dispute had already hardened into factions.

The defining moment came in 680 CE during the Battle of Karbala. Ali’s son Husayn ibn Ali challenged the rule of the Umayyad caliph Yazid I. Husayn and a small group of followers were killed in Karbala (modern Iraq). For Shia Muslims, Husayn became the ultimate martyr for justice against tyranny. For Sunni Muslims, the event is tragic but not the central theological moment it is for Shia. This difference in emotional and religious weight still shapes identity hundreds of years on.

Over centuries, the split developed into bigger doctrinal differences. Shia Muslims concentrate the highest in Iran (90-95% of the population), Iraq (65-70%), Azerbaijan (65-75%), and Bahrain (65-75%). Sunni Muslims dominate nearly everywhere else, with near 100% concentrations in countries like Saudi Arabia, Egypt, Turkey, Indonesia, and Pakistan.

Sunni Islam emphasises community consensus. Religious authority comes from scholars and legal traditions. No formal priesthood hierarchy.

Shia Islam Leadership should come through divinely guided figures called Imams, starting with Ali (in other words, by killing Iran’s Supreme Leader Ayatollah Ali Khamenei, it was tantamount to killing the Pope). These Imams are believed to have special spiritual authority. Clerical leadership (like Ayatollahs) developed more formally.

Despite the headlines, most Sunni and Shia Muslims coexist peacefully in many countries. The hostility tends to flare up when political leaders weaponise the divide.

Think of it less like two totally separate religions and more like a very old family feud that occasionally gets hijacked by modern politics.

You may remember that the Iran-Iraq War (1980-1988) was a brutal eight-year conflict sparked by Saddam Hussein’s invasion of Iran on September 22, 1980, aiming to seize the oil-rich Khuzestan province and Shatt al-Arab waterway amid post-revolution chaos in Iran. Iraq initially advanced deep into Iran using air strikes and chemical weapons, capturing Khorramshahr by October 1980. Iran counterattacked from 1982, reclaiming lost territory through human-wave assaults by Revolutionary Guards and Basij militias, notably recapturing Khorramshahr in May 1982.

The war stalemated into trench warfare with city bombings, ending via UN Resolution 598 ceasefire on August 20, 1988. Iran suffered around 500,000-1 million deaths; Iraq around 250,000-500,000, with massive economic devastation and no territorial gains for either side. Iraq’s chemical attacks (mustard gas, nerve agents) killed tens of thousands, setting precedents for later atrocities.

It’s a mess, and all I can suggest is to find a diversion, take up an absorbing hobby, and wait this out. Assume that travel through the Middle East, including Dubai, is going to be on hold for weeks. NATO could be pulled into this war – Turkey was bombed and is part of NATO.

So far, the winner of this conflict has been America. The losers have been more or less everyone else. That’s in part because of the way markets were positioned before the outbreak of hostilities, with the rest of the world enjoying its strongest streak of outperforming the US in years. That created the grounds for a reversal.

It’s also because the US dollar still functions as a safe haven in markets. There was refuge in the dollar, particularly as it had been falling. The DXY chart shows that there has been some recent appreciation, but not near the levels seen at the beginning of Trump’s term (remember, in the DXY index, 100 is considered ‘neutral’, below that is ‘weak’).

The US is protected by geography – oceans on either side from the events in Iran. Everyone outside the Americas is closer to it. It hurts them more. If the Donald was unpopular in Europe before… guess what! Trump didn’t even bother to get Congress’s permission, let alone give his allies the heads-up. Those Middle Eastern leaders who were so busy brown-nosing him last year must be really miffed!

Europe has barely had time to recover from the energy crisis that hit it after the Ukraine invasion of 2022, when natural gas prices spiked. Now it’s happened again, and that’s hugely dangerous politically for governments if not reversed quickly. From the graph below, there hasn’t been much of an impact on the price (yet), but the pressure is on.

The US has almost completely shed its dependence on Middle Eastern oil (“I’m okay, Jack”), but it has no control over the price, and because this is not a government resource (as it is in Saudi Arabia), those higher prices are already feeding through to the pumps across the US. High gasoline prices are politically toxic for any US government, and they have been rising in the futures market since President Donald Trump took office.

This isn’t all good for the US, of course. Rising commodity prices will always arouse fears of inflation. This latest dose of geopolitical risk makes it far harder for the next chairman of the Federal Reserve, presumably Trump’s nominee Kevin Warsh, to cut rates as advertised. Market-based estimates of the fed funds rate at year-end have jumped since the shooting started (indicating no more cuts, and maybe even a rise in interest rates) and are now as high as they’ve been in nine months. Treasury yields had been falling dramatically, and that has also reversed:

Graph: US 10yr Treasuries

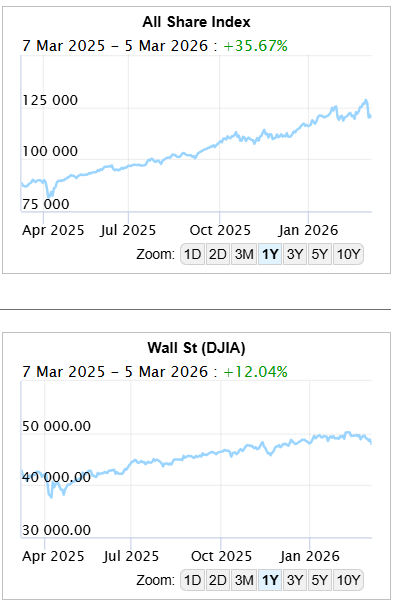

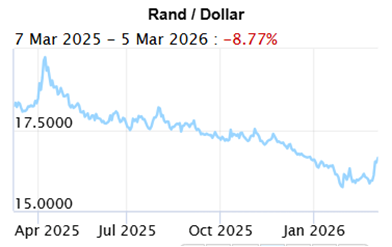

Thankfully for the US, this crisis broke when conditions were not particularly tight. There might be more of an issue for emerging markets (like us), which are traditionally treated as the inverse of the dollar; any strength in the greenback is seen as a problem for developing countries trying to finance their debt. The speed and ferocity with which that flipped after the first reports from Iran has been something to behold, as you can see from our ALSI:

The Iran attack reversed two months of outflows from the US to EM.

For one illustration, look to India. The world’s most-populous country isn’t directly affected by the conflict. Indirectly, however, it has close links to the Gulf states, and imports much energy through the bottleneck of the Strait of Hormuz. As it has large and liquid markets, it’s also an easy place to take a profit.

Put this together, and the rupee has dropped to its weakest against the dollar on record. Meanwhile, the main Indian stock benchmarks have, in dollar terms, shed all of their gains since the Liberation Day turmoil 11 months ago.

Graph: Rupee/USD

America’s victory might not last long. Indeed, its market fortunes are almost the inverse of its fate on the battlefield; these financial trends will extend and intensify if this turns out to be a long, drawn-out conflict, while a swift conclusion could well bring a relief rally for emerging markets. Until these questions are resolved, the perfect storm driving US assets to beat everyone else is likely to continue.

Much of the info in our posts and newsletters about AI has focused on the investment proposition, but there is no doubt that the AI game is about to level up. We saw that above with Anthropic butting heads (and probably losing) with the government over how AI is to be used (especially the worrying ‘Terminator’ factor of autonomous (self-thinking) warfare.

But there is a new worry rippling across the stock market lately: entire businesses, not just their employees, may be thrown out of work. While most economists say fears of an AI job apocalypse are overblown, seismic shifts have occurred in the past following major breakthroughs in big tech.

The IT revolution of the 1990s led to a surge in productivity that sped up the US economy for several years. It also rendered companies or even industries largely redundant, from travel agents and stockbrokers to classified advertising and newspapers, or video rental stores.

Blockbuster Video, once a brick-and-mortar stalwart, has all but disappeared, driven out of business by the internet. Netflix leaned into it and thrived.

Economists expect artificial intelligence to deliver higher productivity, which is key to raising growth rates in the long run. But investors are growing nervous about the damage that might be done along the way, in capital markets as well as labour markets, especially because AI threatens broader-scale disruptions than the internet boom.

The key difference from the 1990s is that the internet only disrupted information distribution; AI disrupts cognitive (knowledge/thinking) production at large. That’s a much bigger economic surface area.

To be sure, all of this is early-days speculation over a fast-changing and largely untested technology, whose ultimate promise is to make workers more productive, but forewarned is forearmed, and if companies and individuals learn to ‘lean in’ to the positives to scale their productivity, then they won’t just survive, they’ll thrive.

Productivity is essentially a measure of how much output workers can deliver with the available tools, so it tends to surge upward when someone invents important new tools, such as the internet or AI.

Productivity Data for the last three months of 2025 is out. US nonfarm business sector labour productivity surged 4.9% (SAAR) in Q3 2025, the strongest since Q3 2023. Manufacturing productivity was up 3.3% QoQ.

Economists typically don’t read too much into one quarter, since the numbers tend to jump around. Still, the trend has been ticking up. After big swings during the pandemic, productivity has grown at an average pace of 2.6% since the start of 2023. That’s more than double the average for the decade through 2019.

There’s intense debate over how much of this acceleration is due to AI. But even analysts who reckon the new technology isn’t yet making a big contribution mostly expect it will do so before long.

A more productive workforce drives the kind of efficiency gains that can allow both corporations and their employees to boost earnings, without triggering inflation. Historically, economies adapt to big tech breakthroughs – creating new industries and professions that nobody could’ve envisioned before – and living standards rise.

As of now, on US capital markets, what’s become known as the “AI scare trade” is barely a blip.

The S&P 500 is up by about two-thirds since the release of ChatGPT in November 2022. A big chunk of those gains has been driven by the surging value of AI companies themselves and their suppliers, giants like Meta Platforms Inc. and Nvidia Corp., which creates one set of risks if their technology disappoints.

But there’s another set, the one behind recent market wobbles, which is different. It stems from the possibility that AI does deliver the promised productivity leap, and then some.

That idea, captured in a research note by the little-known firm Citrini, sent the S&P into a brief nosedive at the start of last week. Citrini’s scenario of massive white-collar layoffs driven by AI was basically sci-fi, set in 2028. There’s no sign of anything like that now, with US unemployment at historically low levels. Still, interesting to watch.

Also, even if companies aren’t yet cutting jobs or wages, they are trimming in areas like health care, remote work and even free snacks. These side benefits are what the companies go after first, before they go after reducing your paycheck. When businesses can cut payroll costs because technology enables them to do more with less, that’s often good news for their profits and shareholders.

The fear that artificial intelligence will lead to mass layoffs is spreading. Jack Dorsey, the co-founder of the financial technology firm Block, laid off nearly half of its workforce last week. Citing AI’s labour-saving capabilities, he predicted other companies would soon follow suit: “Within the next year, I believe the majority of companies will reach the same conclusion and make similar structural changes.”

Widespread automation, replacing human workers and devaluing human expertise, as Dorsey predicts, is only one possible outcome of AI. Another path is “pro-worker AI,” a phrase coined by a team of MIT economists, that enhances the value of existing human expertise and creates new tasks. Unlike AI automation, pro-worker AI that raises a worker’s productivity can increase wages and expand employment into new areas.

An existing example they give is a food delivery app in China that added a voice chatbot to support hearing-impaired delivery workers, significantly improving their performance. A speculative example is an AI assistant that enables aircraft maintenance workers to transition into spaceflight maintenance workers. It may be easier to imagine the jobs that AI will destroy than the ones it will create, but job creation is common with many technologies. In fact, about 60% of jobs in 2018 were in occupational specialities that did not exist in 1940.

Whether AI is pro-worker is not principally about AI’s technological capabilities. It’s about how leaders in corporations, government agencies, schools or civic organisations deploy it. Essentially, the same AI tool could be used to support and empower workers, or to surveil and sanction them. It’s the intention, not the technology, that drives the effects on workers.

Speed is another dimension to consider. AI tools are developing rapidly, but we can still be deliberate in the implementation. Federal Reserve Governor Chris Waller recently spoke about the use of AI within the Fed system, including in its operations, such as payment processing.

Finally, there is a role for the government in encouraging a scenario in which AI broadly serves people. The goal is not to stop AI but to encourage its empowering applications and provide examples of use cases beyond automation.

Past technology booms have seen household-name businesses fall by the wayside – like camera-maker Kodak and video-rental chain Blockbuster, left behind by the internet. It’s all part of what the economist Joseph Schumpeter called the “creative destruction”, which leads to progress. Eventually, the disruption will extend to any firm whose competitive advantage lies in human expertise that AI can replicate.

Anyone who has been reading this newsletter for a while will know that I keep a very close eye on the NHI bill that was signed into law by Ramaphosa in 2024 (I still have unanswered questions as to why he would do that).

Bottom line: everyone with a sentient brain cell knows it is a no-starter. We cannot afford it, and we cannot afford the mass exodus of doctors and professionals if the ANC tried to shoehorn the bill into any kind of life. As the bill stands right now, medical aids would be outlawed, doctors would be able to practice only for the government (at rates they set), and individuals would have no choice in their health provider. I have written about this extensively in the past (you can read some of them HERE), and I brought receipts – links to and extracts from the Act.

Still, just last week, the health minister, Aaron Motsoaledi, pledged that National Health Insurance (NHI) is still a go. (Shame man, shouting into an echo chamber must be soul-destroying, it’s his job after all, I guess).

NHI, sold by ANC politicians to the public as a cure-all for a flailing public health system, would force all doctors and providers to contract with a single state-run fund (the biggest slush fund ever), from which all health services would be distributed. But the policy has become a symbol of pernicious government lawmaking: there is no plan, other than new taxes, for how to fund a scheme that could cost anywhere from an additional R450bn to well over R800bn a year (already at R304Bn), while one survey found that 38% of doctors would emigrate if this were implemented (all doctors forced to work for NHI, and charge NHI rates).

Already, there are 14 court challenges to NHI, legislation signed by President Cyril Ramaphosa in May 2024 shortly before a national election in which the ANC’s support plunged to 40% from 57%. Two weeks ago, Ramaphosa said he would “delay the proclamation of any sections of the NHI Act” until after the Constitutional Court handed down its ruling in one case in May.

Still, Motsoaledi, speaking in parliament this week, seemed entirely unfazed by the fact that Ramaphosa has put the plan on ice. “In terms of preparation, we are going full force,” he said. “We did not say we are going to pause the preparation for NHI.”

The health minister said his department will be instituting price controls for private healthcare services, introducing a national electronic patient record system, and overhauling hospital infrastructure. 🤣

In the course of my work with Michael Avery for Classic Business on Fine Music Radio, I have actually interviewed one such company that has been testing this “national electronic patient system” for well over a decade. They haven’t even got it to work for a region within Gauteng, so ‘national’ is a pipedream. This is the backbone of the system and looks like it’s more than a decade ahead.

Piet le Roux, CEO of Sakeliga, which brought the Constitutional Court challenge, has already publicly stated that they won’t stand by if Motsoaledi violates the court order.

Motsoaledi has said he wants to continue with ‘preparing’ for NHI, but the court was very clear that all elements of NHI must be halted. So if we see that the lines he does cross with respect to implementing it. Personally, I hope he does; this issue needs to have a higher profile.

I think we can all agree that the public health system is broken, and it’s not entirely due to a lack of funding. One would think that the logical first step would be to fix what is broken in the government system, not drag private health care down to that level. Some estimates put wastage and corruption as high as 30%.

The reality is that you only need Motsoaleti to start implementing some of the most onerous clauses in the act for the emigration floodgates to open, and once gone, those professionals won’t come back. Ironically, Motsoaledi acknowledged last week that the legal challenges are causing major delays. “We might be in court for the next 15 to 20 years,” he told MPs.

There is already widespread public scepticism about state-run funds, given the corruption bubbling over in similar institutions, such as the Road Accident Fund. On this score, it doesn’t help Motsoaledi that this week his health department director-general, Sandile Buthelezi, was arrested on charges of fraud and theft involving more than R1m.

Motsoaledi clearly didn’t listen to the budget speech, where finance minister Enoch Godongwana set aside no extra money for NHI, other than for smaller projects already in the works. It’s very difficult to implement anything when no funds have been allocated. This is probably not surprising, since Godongwana is no great fan of NHI. Last October, he described the scrapping of medical aid tax credits to finance NHI as an “attack on the middle class” (there are too many ANC ministers and supporters who would personally be hard hit by the NHI, and they know it).

One of the major problems with NHI’s architecture, which the government doesn’t seem willing to concede, is that private medical aid members already contribute about 75% of the public system’s funding through their taxes.

Discovery, the country’s largest medical aid administrator, estimates that people who pay for private healthcare would have to pay 31% more tax for NHI, while getting 71% less medical cover.

One reason why the NHI cannot go ahead, he says, is that the ANC no longer has the political support to make it happen. Massive constitutional changes would be needed, including removing health funding from provinces, while new taxes would have to be approved by parliament through a “money bill”. In the two decades since the NHI was first floated, there has never been any government document outlining how much it will cost and how it will be funded.

You know, Business Planning 101.

So much of what the NHI requires (like money and changes in tax laws to fund it) depends on parliament, and the ANC is at 40% – they would need the consent of coalition partners who are unlikely to give it.

But if NHI is unimplementable and dead in the water, why not just pull the plug on it? Why keep the façade alive? The answer, experts say, is that it would be politically unpalatable for the ANC, which has pinned so much of its populist appeal on delivering the legislation, to reverse course. For example, before the May 2024 election, Gauteng premier Panyaza Lesufi told an ANC rally that, on the day after the election, “you can go to any hospital of your choice, whether it’s a private hospital or a public hospital … and the government will pay that bill”. Bottom line, Motsoaledi is just sabre-rattling, but if he turned around to look for his troops, he’d find them all quietly skulking off in the background heading for the local Netcare or Mediclinic. IMHO, the best course of action for the ANC is to let the NHI die a slow death through a combination of court cases and election results. For individuals, don’t make knee-jerk reactions based on party propaganda spouted by lame-duck ministers.

Author: Dawn Ridler

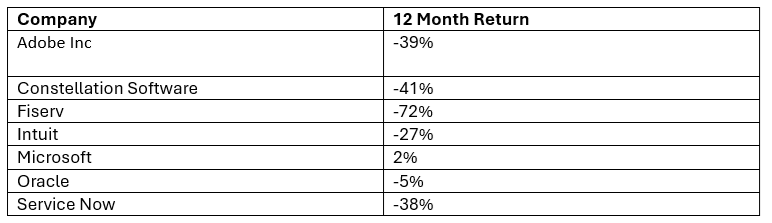

Software as a Service is a genre of IT companies that develop software and sell it to customers as a service. You, as a customer, don’t actually own the software; you rent it from the company, and today, one is probably using it in the cloud rather than running it natively on your PC, as one would have in the distant past. Microsoft is probably the best example of a SAAS company, and its ability to entrench its product into our everyday lives is unparalleled.

In the past, SAAS companies were a favourite amongst venture capitalists. They can launch quickly and develop a subscription market that finance people love. They liked the fact that a Revenue stream could be derived from a capital-light activity, and this, in turn, allowed venture capitalists to sell their shares to a broader market in an IPO (initial public offering) once they had turned a profit. Here is a collection of some SAAS companies:

But the fear now is that AI will change these organisations. The theory is that a customer would not bother hiring a SAAS company if an AI tool can build the software required for a task, thus bypassing these organisations.

Clearly, bypassing Microsoft is much more difficult than, say, Adobe, and this is reflected in the price movement of these stocks over the last year. But take Fiserv, which maintains and runs software for banks. Without them, some US banks will be unable to process transactions. So, clearly, this business is core to certain banks’ operations, but the share price suggests otherwise.

At Fiserv, debt has been rising as they pursue growth. Their returns on invested capital, though, show that they are battling to execute on this. As the threat that banks could bypass Fiserv was digested by markets last year, this stock quickly derated to reflect its low ROIC and high debt levels. Markets can be brutal.

The question investors need to ask is, will AI disrupt these companies to such a degree that they will lose their market share?

The price movements indicate that investors think this could be a possibility, but it probably warrants slightly deeper analysis. The first thing to consider is that to get AI to write code and implement it into a work process that can actually be used by an organisation is probably far-fetched. Perhaps programmers will use AI to assist in building code, but to combine all of this into an application on which a critical business system will run, whilst bypassing the very people who perfected the application, doesn’t make sense.

Perhaps customers in time are able to more easily write complementary code to their existing systems rather than only relying on a SAAS company. The tricky question of who takes responsibility if something goes wrong then emerges. It has been my experience that companies like clear tasks and deliverables, and if this falls into the scope of what a SAAS company offers, then this needs to be weighed up against the cost.

Jensen Huang of Nvidia fame thinks of AI as AI Agentic. It acts as an agent to others who drive the process forward. The best people to do this are probably still the SAAS companies, who could probably become more efficient as they use Agentic AI. And then there is the issue of incentives. We all act based on incentives. If we are not motivated to act, no action occurs. What incentive do IT departments at corporations have to switch off SaaS providers and use AI to replicate the very code that already exists in an ingrained business application? I would say very little. Their first and foremost objective is to keep their jobs. Going out on a limb trying to recreate code that already exists seems foolhardy.

Author: Cobie LeGrange

EXCHANGE RATES and other Indices:

The Rand/Dollar closed at R16.55 (R15.93, R16.01, R15.96, R16,03, R16.15, R16.10, R16.50, …R16.91, R17.13, R17.36, R17.13, R17.27, R17.31, R17.25, R17.38, R17.50, R17.22 , R17.35, R17.33, R17.37, R17.58, R17.65, R17.44, R17.61, R17.74, R18.15,R17.76, R17.72, R17.90, R17.58, R17.89, R17.99, R17.92, R17.77, R17.95, R17.88)

The Rand/Pound closed at R22.20 (R21.48, R21.59, R21.78, R21,82, R22.11, R21.97, R22.13, …R22.57, R22.68, R22.74, R22.56, R22.69, R22.76, R22.96, R23.34, R23.37, R23.19, R23.22, R23.35, R23.55, R23.73, R23.84, R23.53, R23.84, R23.84, R24.09, R23.88, R23.76, R24.22, R24.08, R24.49, R24.22, R24.35, R24.05, R24.18)

The Rand/Euro closed the week at R19.23 (R18.80, R18.87, R18.94, R18.93, R19.14, R19.04, R19.20, …R19.68, R19.86, R19.99, R19.96, R19.98, R20.02, R20.06, R20.26, R20.33, R 20.22, R20.30, R20.35, R20.38, R20.61, R20.62, R20.44, R20.56, R20.64, R21.04, R20.86, R20.61, R20.93, R 20.70, R20.91, R20.74, R20.68, R20.24, R20,37)

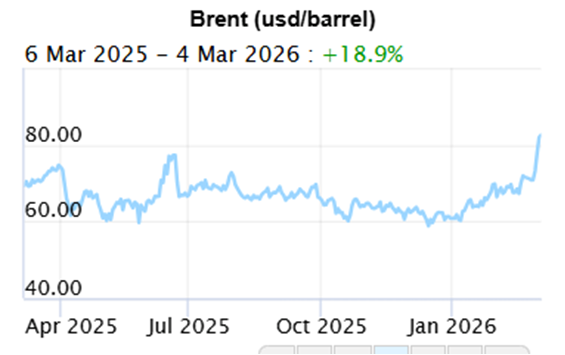

Brent Crude: Closed the week $92.88 ($73.19, $71.76, $67.75, $68,05, $69.32, $65.88, $63.34, …$63.71, $63.19, $62.42, $63.94, $63.61 $64.66, $65.04, $61.27, $62.14, $64.28, $69.67, $66.57, $66.80, $65.52, $67.38, $67.73, $66.08, $66.07, $69.46, $68.29, $69.21, $70.58, $68.27, $67.39, $77.27, $74.38, $66.56, $62.61, $65.41)

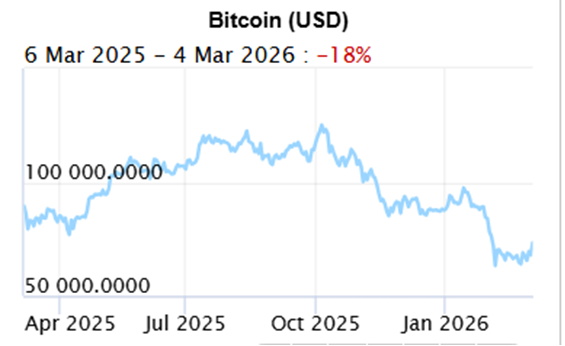

Bitcoin closed at $67,310 ($63,534, $68,04, $69,649, $68,553, $81,301, $89,295, $90,585, … $90,809, $86,334, $94,990, $101,562, $109.936, $112,492, $106,849, $111,888, $124,858, $109,446, $115,838, $115,770, $110,752, $108,923, $114,916, $117,371, $118,043, $113,608, $118,139, $118,214, $117,871, $108,056, $107,461, $103,455)

Does and don’ts of your will and Estate Planning NEW

Planning your legacy, starting with your will NEW

Holiday checklist NEW

Next year – Action Plan

Next year – Vision, Mission etc.

Medical Risk Mitigation

Next Year – Consolidation

Abdication or diversification?

Carbo-loading your retirement

Spoiled for choice

Who needs a plan anyway

8 questions you need to ask about retirement

What to do when interest rates drop

How to survive volatility in your investments

What to do when interest rates drop

Difficult Financial Conversations

Financial Implications of Longevity

Kick Start Your Own Retirement Plan

You matter more than your kids in retirement

To catch a falling knife

Income at retirement

2025 Budget

Apportioning blame for your financial state

Tempering fear and greed

New Year’s resolutions over? Try a Wealth Bingo Card instead.

Wills and Estate Planning (comprehensive 3 in one post)

Pre-retirement – The make-or-break moments

Some unconventional thoughts on wealth and risk management

Wealth creation is a balancing act over time

Wealth traps waiting for unsuspecting entrepreneurs

Two Pot pension system demystified

Cobie Legrange and Dawn Ridler,

Rexsolom Invest, Licensed FSP 45521.

Email: cobie@rexsolom.co.za, dawn@rexsolom.co.za

Website: rexsolom.co.za, wealthecology.co.za