Your summary with links, if you’d like to curate your content:

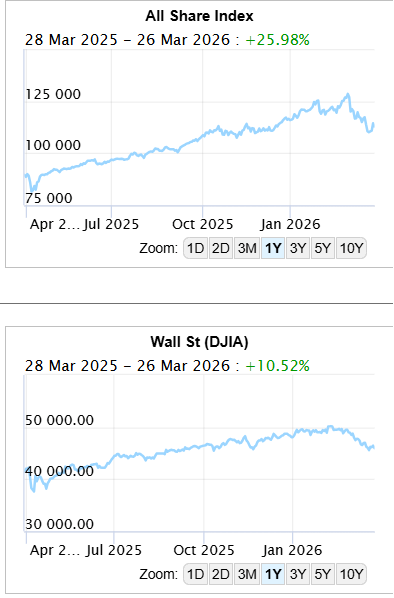

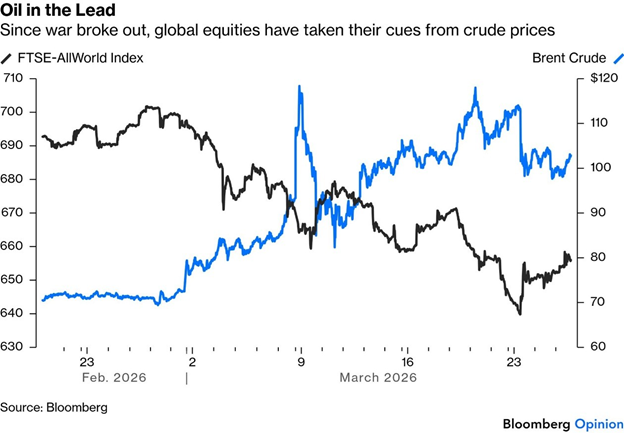

A volatile week across global markets. The JSE remains ~10% below its February high, while the SARB held the repo rate at 6.75% amid rand weakness and rising oil prices. South Africa’s GDP grew 1.1% in 2025. The US Fed held rates steady as jobs data weakened and inflation proved sticky. Markets sold off sharply. The US-Israeli war on Iran — closing the Strait of Hormuz — has caused the largest oil supply disruption in history, rippling across global economies.

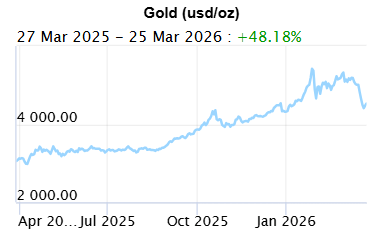

Golden Stumble: Gold surged to an all-time high in late January but has since lost roughly a fifth of its value. The Iran war exposed gold as neither a safe haven nor anti-fragile, adding portfolio volatility rather than reducing it. Comparisons are drawn to the Nasdaq dot-com bubble. Retail investors piled in at the peak, and selling pressure is expected to persist until market volatility settles and inflation/rate expectations stabilise.

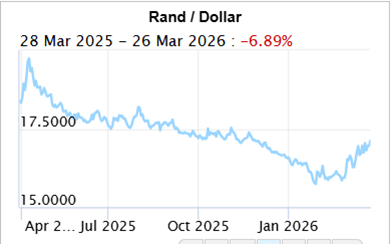

Stronger Dollar: The USD has appreciated ~4% since January, driven by safe-haven demand, the Iran conflict pushing oil higher, and fading rate-cut expectations. The rand has suffered — partly from dollar strength, but more from the global flight to safety.

Beleaguered Britannia: The UK is the developed economy most damaged by the Iran conflict. 10-year gilt yields briefly broke 5%, surpassing even the Liz Truss crisis of 2022. The Bank of England has shifted from expected rate cuts to likely hikes. Politically, Prime Minister Starmer faces 68% odds of leaving office before year-end, per prediction markets.

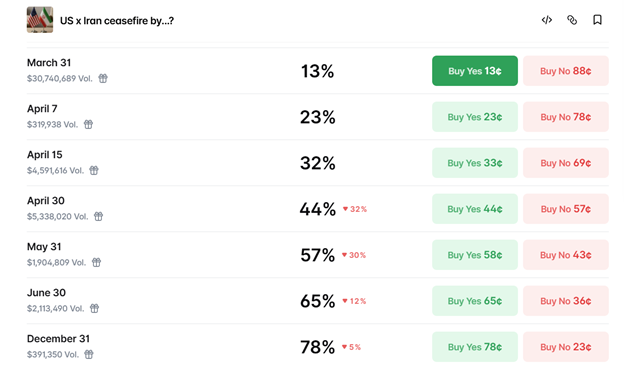

Iran War – TACO Wins Again?: Both the US and Iran appear to be seeking an off-ramp, but markets remain uncertain. Trump extended his ultimatum to 10 days. Prediction markets put ceasefire odds at roughly 50/50. Oil and equities are range-bound pending clarity. The prevailing view is that the worst will be avoided — and that this represents a buying opportunity — but only if a deal is found.

Cutting the Fat: Novo Nordisk has lost nearly $500 billion in market value over 21 months despite strong demand for Ozempic. Patent expirations in India and China (40% of the world’s population) will open the door to generics at a fraction of the price. Competition is intensifying across the GLP-1 sector, and global obesity-drug revenue forecasts have been trimmed to ~$120 billion by 2032.

RSA Interest Rates: The SARB held rates at 6.75%, with expectations now shifting toward potential hikes rather than cuts. Oil up ~40% and the rand down ~6% since the war began are fuelling inflation fears. The SARB’s 3% inflation target adopted in July 2024 is under pressure, and similar challenges are playing out across African economies.

Yields and Volatility: A clear divergence has emerged between policy rates and bond yields globally. Rising yields — driven by oil-fuelled inflation fears — threaten to dampen growth. Two scenarios are outlined: a peace accord that eases yields and restarts a debt refinancing cycle, or a deeper military confrontation that opens US control over Iranian energy resources. Either way, the Strait of Hormuz is seen as the pivotal battleground for the future of the petrodollar system.

This Week’s Roundup

The FTSE/JSE All Share Index has been navigating a volatile period, rebounding approximately 3.17% after a significant drop earlier in March, though the index remains around 10% below its February all-time high of 129,339.

Here in RSA Inc, gold is obviously important, perhaps not as important as it was half a century ago, but much of the market movement we saw last year in the JSE came from that often sleeping giant. Unfortunately, the war in the Middle East has revealed that gold isn’t much of a haven anymore. It’s almost exactly the opposite. The metal has lost about a fifth of its value since it surged to an all-time high in late January. At that point, it was buoyed by the belief that the US administration was “debasing” its currency, which peaked when President Donald Trump said he was content to see the dollar move “like a yo-yo.”

It also provided a haven from Russia’s invasion of Ukraine. This Trump-Iran war has been very different. Gold is roughly where it started the year, but only after an epic roller-coaster ride:

The selloff from its January intraday peak to the trough earlier this week was an epic 27%, while the week leading up to Trump’s post, threatening to attack Iranian energy installations, was its worst five-day decline since 2013. That discouraging precedent was the start of a lengthy (over 12-year) bear market.

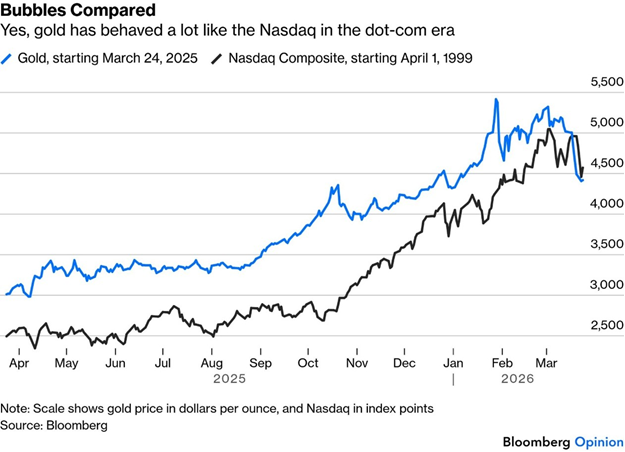

For gold investors and for us South African asset managers, the question is whether this conflict marks a tectonic shift in the underlying assumptions that have driven its rise (like the bear market of 2013, which came as investors grew to accept that the monetary easing that followed the Global Financial Crisis was not going to cause inflation), or a simple reaction to idiosyncratic factors tied to the war. Gold’s trajectory in the last year looks strikingly similar to the Nasdaq Composite in the lead-up to the bursting of the dot-com bubble, which offers little comfort. Sure, this could be a coincidence.

Both the Nasdaq and gold topped shortly after hitting the 5,000 landmark. Gold has been around for centuries, and the Nasdaq covers a huge list of well-researched public companies. An 80% gain in a matter of months proved madness for the Nasdaq, and will it be the same for gold?

Another similarity with the Nasdaq bubble is that it appears to have dragged in the little guy, retail investors, at the top. There were record global sales of exchange-traded funds tied to gold in January 2026. Asia, where investors were trying to avoid getting caught up in any downdraft from the dollar’s decline, saw particularly enthusiastic buying. Was it ‘overbought’ (massive FOMO) in the lead-up to the war, and this is the ‘rightsizing’ that was waiting to happen?

The current situation is similar to the early 1970s: sharp price surges followed by sharp corrections, then another sharp rise once the recession was over.

Does this point to a path back for gold once geopolitical tensions ease? It continues to amaze me how eager retail investors are to believe the nonsense that comes out of Trump’s Lie Social Media Account or press conferences. The rebound in the price after Trump’s decision on Monday to delay planned attacks on Iranian energy infrastructure underscores how eager gold investors are for an off-ramp.

In this crisis, gold is showing itself not to be an “anti-fragile” asset and has added more volatility to portfolios than most investors likely expected. As such, selling pressure is likely to persist until overall market volatility abates and/or until companies and countries feel comfortable returning to “just in time” inventory management rather than “just in case.”

Another argument is that gold investors, like many others, have been flummoxed by the return of inflation. From the GFC (2008) through to early 2022, inflation was barely an issue, and gold had a very strong inverse correlation with real yields. Remember also that gold does not give you dividends, income or interest – as with all commodities.

For us, asset managers in South Africa, we face the dilemma: how do we capture the upside of this (and other niche asset classes) without risking exposing portfolios to a sector that goes through marathon hibernation followed by short, massive spurts of activity?

It appears that gold’s surge over the last six months has shown it to be unmoored from any sensible fundamentals. The shock of the war provided the necessary slap in the face.

Another explanation is the change in interest-rate expectations.

The war has dampened rate-cut hopes amid surging inflationary pressures. That’s not great for the US economy, but neither is it good for those who had been eagerly betting on the “debasement” trade. Now that the conflict has left investors in doubt, they are pulling back from gold — even though inflation expectations are rising.

The impending arrival of a new Federal Reserve chairman, probably the president’s nominee Kevin Warsh, adds a further argument about debasement and excessive easing. As we have discussed over the last few weeks, Kevin Warsh still has to have his nomination approved by the Senate, and with more Republicans breaking ranks and wanting to distance themselves ahead of the midterm elections, that is not a foregone conclusion. New Fed chairs are generally tested by the market and have to prove their willingness to be tough. For all the pressure to cut from the White House, the pressure in the other direction from markets could be stronger. If gold’s strength really was a rational way to hedge against debasement, which is questionable, then that would explain why it has pulled back.

The US dollar has strengthened notably in recent months, driven by a confluence of factors. Most significantly, the escalating conflict with Iran has pushed oil prices sharply higher, driving safe-haven demand into the dollar and forcing the Federal Reserve to delay its next rate cut. Since its January lows, the greenback has appreciated by almost 4%, supported by geopolitical tensions, structural advantages in the global energy market, and shifting expectations for US monetary policy.

Graph : DXY Index

On the interest rate front, traders have scaled back expectations for Federal Reserve rate cuts this year and now anticipate no reductions for the time being. Higher rates make dollar-denominated assets more attractive to global investors seeking yield. US economic performance is also still outpacing its competitors, and American firms, particularly in the tech and AI sectors, remain dominant, while employment has held up better than expected.

Finally, the US benefits from its position as a net energy exporter, meaning that rising oil prices strengthen the US economy’s resilience relative to energy-importing regions like Europe and parts of Asia, further widening the growth gap and underpinning dollar demand. The renewed dollar strength is behind SOME of the rand depreciation over the last few weeks, but a flight to ‘safe haven’ assets (you know, countries that start a war on a whim) is a far bigger driver.

Britain is approaching the 10th anniversary of its fateful decision to “take back control” in the Brexit referendum of 2016. It doesn’t feel that way, and I am sure, with the privilege of hindsight, many ‘Yay’ voters would vote ‘Nay’ given the chance again. (Don’t expect a reversal of that decision any time soon, even Keir Starmer, who was once floating a second referendum, has become very quiet on the issue; we are much more likely to see a gradual ‘reintegration’ with Europe in strategic areas.)

Of all the developed economies, the UK has suffered more collateral damage than any other from the hostilities in Iran. Severing ties with the European Union, still dangerously dependent on Russian energy, and attempting to move closer to the American orbit haven’t helped. The problem shows up in the most important market for politicians. The yield on 10-year gilts briefly broke 5% on Monday, before Donald Trump’s announcement of a delay to bombing raids prompted a switchback. Rising yields have been universal, but UK yields are now the highest of the developed economies, and they alone have come all the way back to their highs from before the GFC in 2008.

That means that the bond market’s revolt has gone beyond even the extremes that ended the short premiership of Liz Truss back in 2022. The intensity of the pressure on gilt yields in the last month is distinctly reminiscent of that episode. The speed of the ascent has not been as great, but this is plainly a damaging shift.

This revolt, however, is less directly about the government’s fiscal plans and more about the central bank. Expectations have turned 180 degrees since the bombs started falling on Tehran. At that point, the market was pricing in at least two 25-basis-point cuts in the Bank Rate by the end of the year. Now it’s pricing at least two hikes. That’s because inflation expectations have surged, giving the Bank of England little choice but to hike, even with a sluggish economy that otherwise would require cuts.

Politics is also a problem. Betting on prediction markets is fast generating controversy, but needs to be taken seriously, particularly when assessing a situation as well-publicised as the British premiership. Polymarket (betting platform) currently puts the odds that Sir Keir Starmer will be out as prime minister before the end of this year at 68%. That number has been steadily rising. His most likely successors all appear to be to his left, and less to the gilt market’s liking. It’s hard to disagree with the assessment that Starmer is in deep trouble, even though his party has a big enough majority that there is no need for it to call a general election until 2029.

“You’re beginning to see the regime look for an exit ramp,” said White House Press Secretary Karoline Leavitt last Wednesday when asked about negotiations to end the war in Iran. She was talking about Iran, but it might just as easily have been the US.

The next stage of escalation, should it happen, would be a win for nobody; the US would take out Iran’s energy infrastructure, and Tehran would retaliate by doing similar damage to production and storage facilities across the Gulf, meaning energy and food crises for a swathe of the world’s population. It’s obvious that both sides could use an off-ramp. The question is whether they can find one before it’s too late.

Stocks have been supported by growing confidence that America is indeed looking for an off-ramp. There is no point in predicting what Trump will do next. His ‘Lie Social’ all-caps midnight posts show that he is changing his mind minute by minute. The No Kings 3 protests on Saturday were the biggest yet. Markets are likely to spend the rest of the week wavering as they weigh the evidence that Iran, despite its denials, could really make a deal.

Trump is prone to exaggeration and contradiction, but he is stoking up a deal so much that it’s clear he wants one. The US has a clear Plan A:

But when he conducts the same exercise for Iran, he gets questions rather than answers:

Prediction market bettors think there’s no better than a 50-50 chance of a ceasefire by the end of next month. Trump’s announcement Monday of a delay to escalation was seen to make a ceasefire significantly more likely, but still no better than a toss-up. Since then, there has been a trendless moving around the 50% level:

Without a deal, the best available outcome may be for the US somehow to reopen the Strait of Hormuz by military force, which would probably take weeks rather than days, while the energy crisis for much of emerging Asia would deepen. While it’s clear Trump doesn’t want to escalate, the fact that the US is sending troops to the region, ready for a ground operation, shows it’s a possibility.

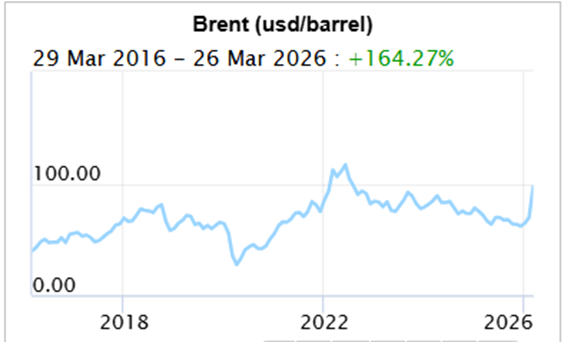

Oil and equity prices are roughly where they were a week ago, plainly driven by Gulf news, and unlikely to break out of their current (wide and jittery) ranges until the ultimatum expires and we have some clarity on a ceasefire. Brent crude has reached back above $100 a barrel several times now, a level that makes nobody in any petroleum-importing country comfortable:

The likelihood is that the worst will be avoided (because it usually is), and that this will be a buying opportunity. That’s why the main markets haven’t sold off far more. They will do so if Iran and the US can’t find an exit ramp between them.

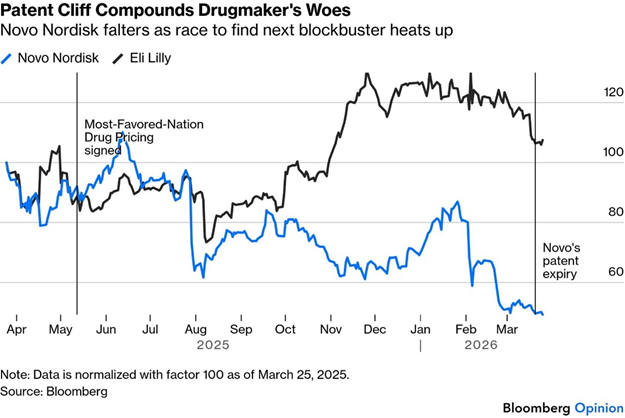

Over the last 21 months, Danish drugmaker Novo Nordisk A/S’s market valuation has fallen by nearly $500 billion. That’s more than the entire market cap of Costco Wholesale Corp. or Netflix Inc. Over that span, the maker of the blockbuster weight-loss drug Ozempic has gone from Europe’s most valuable company to an also-ran. All of this while obesity continues to be a pressing public health concern and demand for its products remains undimmed.

The expiration of the company’s patent for its obesity and diabetes drugs in notably India and China, which make up about 40% of the world’s population, means Novo won’t be catching a break any time soon. Lower-cost generics capable of delivering similar outcomes are likely to hit these two countries at prices as low as $14, a fraction of Novo Nordisk’s branded offering.

Historically, patent cliffs like this have devastated biopharma companies’ margins, and investors plainly expect that this time will be no different. The current wave of expirations will cover drugs worth roughly $150 billion in revenue. While companies have weathered previous cliffs, the stranglehold is not abating. Over the most recent 10- and five-year periods, the share of companies in the sectors with falling margins has jumped to more than 50%.

Over the last two decades, margins at more than 30% of the world’s top 20 biopharma companies have declined, 44% have kept them stable, and 25% have boosted profitability. In many cases, margin expansion has resulted from topline growth driven by individual products, not from controlling costs. That highlights the pressure generic GLP-1s are expected to put on weight-loss and diabetic drug manufacturers.

Novo’s rivals haven’t been spared. Intense competition and Washington’s drug-pricing policy are also chipping away at profits. This raises the stakes in the search for new blockbuster drugs. For example, the widely anticipated weight-loss pill cleared the US Food and Drug Administration’s last hurdle in December. That should expand access to millions of patients who were previously excluded, either by expense or because they disliked injections.

But there’s only so much these pills can do for profits, especially compared with their far pricier predecessors. That helps explain the muted response from investors, who may already have priced in the pill’s debut.

Whether investors are buying into these prospects is another thing.

The analysis of the obesity market suggests that prices, more than product features, are a greater driver of market share. Increasing competition from Novo as it fights to regain its foothold in the market is likely in the near term. Intense competition is good for consumers, but not helpful to investors seeking to capitalise on pharmaceutical breakthroughs. More importantly, perhaps, even the forecasts for the eventual revenue generated by the entire market are also slimming down. Analysts expect global obesity-drug revenue to reach about $120 billion by 2032, short of earlier projections by at least $30 billion.

South Africa’s central bank kept borrowing costs on hold to assess the inflationary impact of the US-Israeli war on Iran, which has sent oil prices surging and pummelled the rand.

There is now an increased expectation that rates will actually start to rise again this year. That marks a change from the last MPC meeting in January, when economists were forecasting multiple rate cuts this year.

It also mirrors a shift in investor expectations on monetary policy globally, with the Iran conflict slashing hopes for rate cuts by the Federal Reserve and the European Central Bank.

Kganyago in January cited geopolitical uncertainty among the reasons for holding rates steady, with subsequent events validating the caution of South African policymakers anxious to defend the 3% inflation target that they adopted last year.

Oil prices have risen almost 40% since the US and Israel attacked Iran on Feb. 28, while the rand has retreated about 6% against the dollar since the start of the conflict.

South Africa is heavily reliant on oil imports, and the war has also lifted fertiliser costs, which may spill over into food inflation. Financial markets, which initially expected a quite short war, are now starting to factor in the possibility that it could be longer. Significantly higher fuel prices will obviously give a push to inflation, while noting that a swift end to hostilities may put the central bank back on course to ease rates by 25 basis points in the second half of the year.

The South African Reserve Bank’s quarterly projection model at the January meeting showed rates ending the year around 6.3%, implying roughly two quarter-point rate cuts. Those forecasts are likely to be significantly altered when fresh projections are released …

The central bank lowered its inflation target to 3% in July – marking the first adjustment in the guide since 2000, and the move was ratified by Finance Minister Enoch Godongwana in November. While the Reserve Bank is unlikely to predict an overshoot of its 3% target with a 1% tolerance band, there remains a risk of a persistent breach should oil prices rise further, and the currency endure more pressure.

The SARB would view such a breach as threatening its 3% inflation objective’s credibility. If these risks materialise, the SARB would stand ready to raise rates at future MPC meetings. Similar risks are likely to play out across African economies, with most of the continent dependent on fuel imports. The Central Bank of Kenya, which delivered its 10th consecutive cut last month, is now seen deferring future reductions, while easing cycles in Nigeria and Egypt have also been put in doubt.

Author: Dawn Ridler

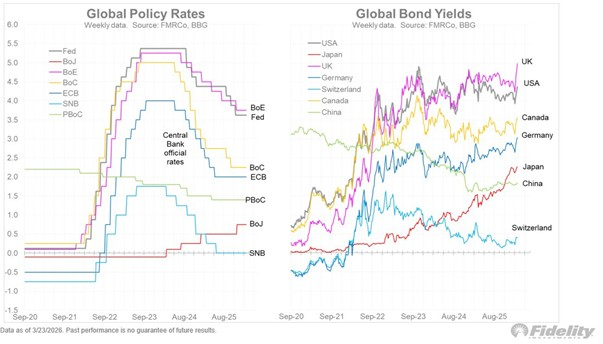

There is now a clear divergence between policy rates and global bond yields, with many developed countries showing a rise in yields. UK 2-year rates are approaching 4.5%, and US yields are almost at 4%. In the month, 2-year US bond yields have increased by 14%, starting the month at 3.38%. But the notion that only US yields are rising is wrong, as the graph below shows.

Much of the rise in yields is due to fears of rising inflation as the military action in Iran forces the oil price above $100. If these inflation fears spill over into actual inflation rising, this will force policy rates higher, putting a dampener on global growth.

Ironically, the FED in hindsight was probably right in keeping rates steady whilst the Trump administration was calling for a drop in interest rates. They capitulated in the second half of 2025 but will probably have to review that in the coming months. It is now up to the US government to end the war quickly so that inflation doesn’t settle at a value which forces interest rates up again. If the war isn’t unpopular with the US public already, higher interest rates definitely will be.

What will all of this look like at the midterm elections?

The other factor to consider is governmental debt. As rates rise, it becomes more expensive for governments to fund their deficits. For the US, this is a real issue and has been behind the US administration’s drive to lower rates throughout the last year. For Europe and Asian countries, this is a wound that is inflicted on them by a one-time ally. So, where to from here?

The one outcome is a peace accord between the fighting parties. Even though oil won’t start flowing immediately, the uncertainty about the future will evaporate, creating a market in equities. This will force bond yields lower again, and the world will go back to a debt refinancing cycle. The other outcome is that peace only comes through more conflict. This could involve US troops being deployed somewhere in the Strait of Hormuz (they are already on their way) and, with the aid of other Gulf nations, calling Iran to order with the objective of opening the Strait. This is the likely situation.

Consider that the US today controls Venezuelan oil, and if it can control Iranian resources as well, this will make it a dominant energy player if this capacity is added to the US’s own resources. There is a lot at stake. Achieve this, and Petro-Dollars continue to be the gold standard to beat. If they fail at this, the oil market becomes a lot more fragmented as certain oil contracts, depending on nationality and destination is settled in other currency units. The push for a new world order is playing out in the Strait of Hormuz.

But there will be an end to this crisis, and investors will look back at these events and talk about the buying opportunity it created in asset classes. No one knows when all of this will be resolved, but enough is at stake for role players to resolve the matter.

Author: Cobie Le Grange

EXCHANGE RATES and other Indices:

The Rand/Dollar closed at R17.07 (R17.06, R16.89, R16.55, R15.93, R16.01, R15.96, R16,03, R16.15, R16.10, R16.50, …R16.91, R17.13, R17.36, R17.13, R17.27, R17.31, R17.25, R17.38, R17.50, R17.22 , R17.35, R17.33, R17.37, R17.58, R17.65, R17.44, R17.61, R17.74, R18.15,R17.76, R17.72, R17.90, R17.58, R17.89, R17.99, R17.92, R17.77, R17.95, R17.88)

The Rand/Pound closed at R 22.77(R22.76, R22.35, R22.20, R21.48, R21.59, R21.78, R21,82, R22.11, R21.97, R22.13, …R22.57, R22.68, R22.74, R22.56, R22.69, R22.76, R22.96, R23.34, R23.37, R23.19, R23.22, R23.35, R23.55, R23.73, R23.84, R23.53, R23.84, R23.84, R24.09, R23.88, R23.76, R24.22, R24.08, R24.49, R24.22, R24.35, R24.05, R24.18)

The Rand/Euro closed the week at R19.70(R19.77, R19.33, R19.23, R18.80, R18.87, R18.94, R18.93, R19.14, R19.04, R19.20, …R19.68, R19.86, R19.99, R19.96, R19.98, R20.02, R20.06, R20.26, R20.33, R 20.22, R20.30, R20.35, R20.38, R20.61, R20.62, R20.44, R20.56, R20.64, R21.04, R20.86, R20.61, R20.93, R 20.70, R20.91, R20.74, R20.68, R20.24, R20,37)

Brent Crude: Closed the week $107.88 ($112.36, $103.14, $92.88, $73.19, $71.76, $67.75, $68,05, $69.32, $65.88, $63.34, …$63.71, $63.19, $62.42, $63.94, $63.61 $64.66, $65.04, $61.27, $62.14, $64.28, $69.67, $66.57, $66.80, $65.52, $67.38, $67.73, $66.08, $66.07, $69.46, $68.29, $69.21, $70.58, $68.27, $67.39, $77.27, $74.38, $66.56, $62.61, $65.41)

Bitcoin closed at $68,691 ($68,586, $70,869, $67,310, $63,534, $68,04, $69,649, $68,553, $81,301, $89,295, $90,585, … $90,809, $86,334, $94,990, $101,562, $109.936, $112,492, $106,849, $111,888, $124,858, $109,446, $115,838, $115,770, $110,752, $108,923, $114,916, $117,371, $118,043, $113,608, $118,139, $118,214, $117,871, $108,056, $107,461, $103,455)

Dos and Don’ts of Wills and Estate Planning NEW

Planning your legacy, starting with your will NEW

Holiday checklist

Next year – Action Plan

Next year – Vision, Mission etc

Medical Risk Mitigation

Next Year – Consolidation

Abdication or diversification?

Carbo-loading your retirement Spoiled for choice

Who needs a plan anyway

8 questions you need to ask about retirement

What to do when interest rates drop

How to survive volatility in your investments

What to do when interest rates drop

Difficult Financial Conversations

Financial Implications of Longevity

Kick Start Your Own Retirement Plan

You matter more than your kids in retirement

To catch a falling knife

Income at retirement

2025 Budget

Apportioning blame for your financial state

Tempering fear and greed

New Year’s resolutions over? Try a Wealth Bingo Card instead.

Wills and Estate Planning (comprehensive 3 in one post)

Pre-retirement – The make-or-break moments

Some unconventional thoughts on wealth and risk management

Wealth creation is a balancing act over time

Wealth traps waiting for unsuspecting entrepreneurs

Two Pot pension system demystified

Cobie Legrange and Dawn Ridler,

Rexsolom Invest, Licensed FSP 45521.

Email: cobie@rexsolom.co.za, dawn@rexsolom.co.za

Website: rexsolom.co.za, wealthecology.co.za