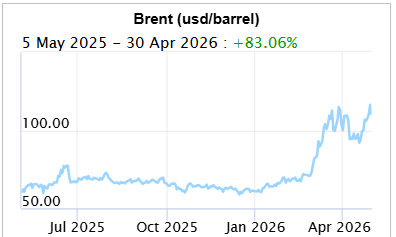

Broadening Oil Spill: Nine weeks in, the Strait of Hormuz remains closed with no serious negotiations underway. Brent crude topped $120/barrel mid-week before settling around $110 — its highest of the conflict — aided by the UAE’s withdrawal from OPEC+. UK 10-year gilts broke 5% for the first time since 2008, and 30-year US Treasury yields hit 5%, signalling a serious inflation alarm. Yet the S&P 500 has rallied 13% since its March low, driven by earnings optimism. Polymarket puts only 52% odds on the Strait reopening by the end of June, making a protracted stalemate the base case.

Turmoil at the Fed – JP’s Last FOMC: Powell’s final meeting produced the most divided FOMC since October 1992, with four dissenters favouring a more hawkish stance. Powell announced he will remain as a governor under incoming chair Kevin Warsh, framing it as upholding Fed independence rather than as dissent. Rate cuts in 2026 are now off the table entirely, with futures markets pricing none. The Fed’s longer-term inflation expectations remain anchored, but short-term measures are surging.

Trump, Fed, Bessent and Warsh: Trump’s desire for rate cuts has been thwarted entirely by the Iran conflict — an outcome described as a self-inflicted wound. The FOMC is increasingly resembling the Bank of England, with narrow majorities and open dissent. Treasury Secretary Bessent attacked Powell’s decision to stay on as governor, but the newsletter notes that attempting to weaponise the prosecution system against Fed governors is a far greater violation of institutional norms.

It’s All About Earnings: Mega-cap results were mixed. Alphabet surged ~7% on strong revenues and its custom TPU chips are challenging Nvidia. Meta fell ~7% despite beating revenue estimates, as investors baulked at projected capex topping $145 billion. Amazon rose on 28% growth in AWS cloud revenue. The key theme: margins matter, and investors are growing sceptical that AI capital spending will be matched by sufficient returns.

Crypto in RSA Under the Microscope: South Africa’s Draft Capital Flow Management Regulations 2026 propose bringing crypto assets into the exchange control framework for the first time. Key measures include mandatory declaration, border disclosure, forced private key disclosure, and penalties of up to R1 million or five years imprisonment. Critics raise constitutional concerns around privacy and self-incrimination. Public comment closes 10 June 2026. The newsletter expects prolonged constitutional court battles.

Still Partying Like It’s 1999: Despite elevated oil prices and ongoing geopolitical risk, markets are surging — reminiscent of late-cycle euphoria. Historical context is offered: bear markets are shorter than bull markets, corrections are common, and returns one year after a bear market trough have historically been strong. At least three “orange swan” events have occurred in the past 18 months.

Valuations and Markets: The MSCI ACWI hit an all-time high in April, driven by large US tech stocks gaining 15%+ for the month. The S&P 500 trades at a stretched P/E of 25x, but forward earnings estimates are rising sharply — 23% year on year for the MSCI USA. The Fed’s Reserve Management Purchases have supported liquidity, but incoming chair Warsh has signalled a return to a more traditional Fed role. With baby boomers heavily reliant on equity markets for retirement income, market stability has become a structural necessity. The overall outlook: markets may deliver a flat return in 2026, with long-term holders best placed to ride out the noise.

This Week’s Roundup

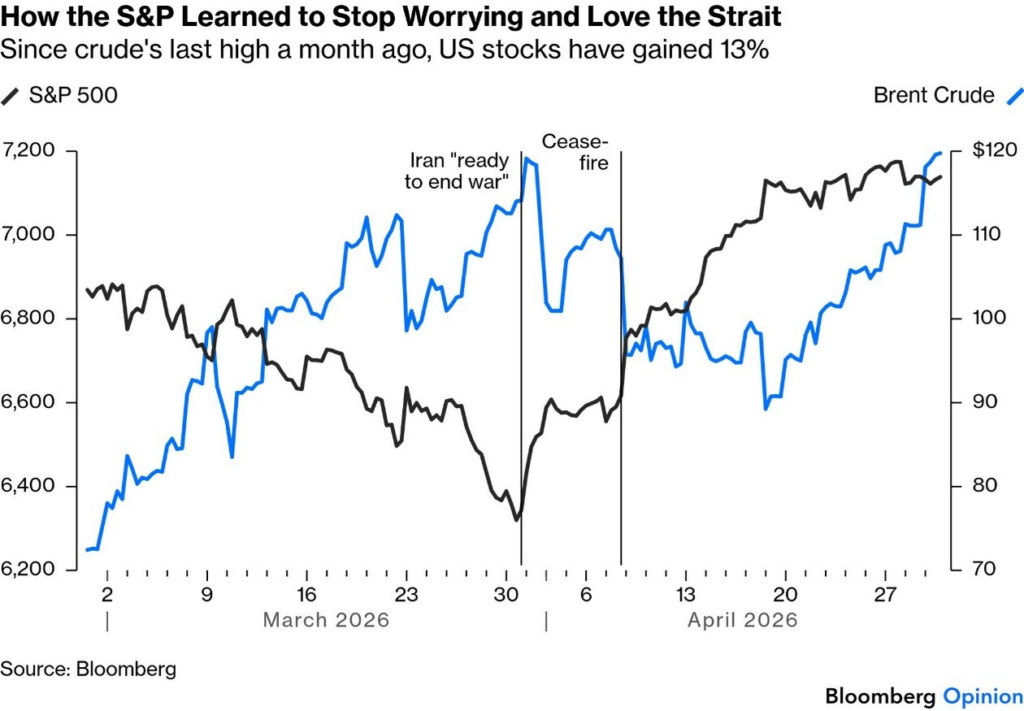

The Strait of Hormuz is still closed, 9 weeks later, there’s no longer any pretence of serious negotiations to open it, and oil prices have reacted by creeping upward. Helped along by the United Arab Emirates’ withdrawal from OPEC+, Brent crude, the world’s most followed benchmark, topped $120 per barrel on Wednesday and closed higher than at any time during the conflict. It is currently at $110.

That drove a series of classic alarm bells across global markets, taking out closely watched landmarks.

Bond yields surged, with UK 10-year gilts topping 5% for the first time since 2008;

30-year Treasury yields are hitting 5% for the first time this year, and the Japanese yen is over 160 to the dollar.

These all suggest alarm about inflation. The war is at a tipping point, with markets accepting that it will seriously damage the global economy.

They also had to absorb news of a more hawkish Federal Reserve than expected, which sent two-year Treasury yields up 11 basis points, their biggest rise in more than six months.

Kevin Warsh is on his way to being confirmed as Fed Chair, but Jerome Powell has also indicated that he will remain on board as one of the governors. Just a reminder, the FOMC is made up of a committee of 12, so the FED Chair alone does not set the rates. In addition to that, in December last year, 11 of the 12 chairs were reconfirmed, early, into 5-year terms – so for Trump to influence them, they would have to be fired (remember the failed attempt to fire Lisa Cooke?), resign or shuffle their mortal coil. Kevin Warsh is going to have a baptism by fire. (More about this below).

During the war’s first month, crude and the S&P 500 had a perfectly inverse relationship. During the second (just ended), they rose together. The S&P hit a low when Brent logged its previous high on March 30. Since then, oil has reclaimed its peak, while the S&P rallied by 13%:

The war isn’t over, and many of the world’s most important markets are behaving as though it’s getting more damaging. But for US stocks, they think it’s over.

Polymarket now puts odds of only 52% on the Strait reopening by the end of June — implying we’re not even halfway through the blockage. A protracted stalemate that creates shortages now looms as the likeliest outcome.

Two months ago, when the war was supposed to end in a matter of days, that would have been an unrealistically doom-laden scenario implying a bear market for stocks. Now it’s the base case. And stocks are up.

How to explain this?

Earnings expectations are behaving like a force of nature, and that is more important than anything else when pricing the stock market. Knowledge that all the biggest hyperscaler groups were announcing results after the close (which we’re also coming to below) would make people reluctant to exit from the market.

The way markets managed to keep on track as the Ukraine war bogged down into a stalemate, and dealt with last year’s tariff war, has also made traders confident. And if inflation is rising, stocks can be a good place to shelter. That said, it’s hard to believe they’re not a tad overconfident.

Turmoil at the FED – JP’s Last FOMC

As non-event meetings go, Jerome Powell’s final session chairing the Federal Open Market Committee was spectacular. Rates are unchanged, and so is guidance. But four of the committee’s 12 voters dissented from that decision. Such a lack of consensus hasn’t been seen since October 1992, the last FOMC before Bill “It’s the economy, stupid” Clinton won the presidency.

So unfazed was Powell by all this dissension that he announced that he’d stay on as a mere governor and member of the committee under successor Kevin Warsh until “it’s appropriate for me to leave. ”He isn’t looking to be a “high-profile dissident”:

My intention isn’t to interfere. I was a governor for almost six years. The tradition is that you work with the chair, and you try to collaborate. That’s the attitude I will take.

He has two years left in his term as governor, and won’t stand down until the Justice Department’s investigation into his handling of the Fed’s building renovations is “well and truly over, with transparency and finality.” He will judge when that’s appropriate.

The thread binding the dissents and Powell’s decision to stay is a determined effort to exert the independence not only of the Fed, but also of the committee’s individual voting members, most of whom now have terms that extend longer than Warsh’s four years as chairman. It will be his job to thrash out a consensus, and that is arguably easier now that his new colleagues have shown their positions. If he cannot deliver rate cuts as President Donald Trump wants, he can blame them.

Powell defended Fed independence by pointing out that markets trust it to control inflation. Longer-term expectations have indeed remained remarkably stable throughout the shocks of the last few years. However, while the five-year/five-year forecast, reflecting inflation from five to 10 years’ hence and the Fed’s favoured measure, remains at only 2.25%, shorter-term swaps forecasts are surging upward.

Any discussion of cutting rates this year is moot. Futures markets no longer expect it, while the rate-sensitive two-year yield has surged with rate expectations.

Trump wants rate cuts, but it’s hard to feel sorry for him; this is mess is 100% an own goal. The impasse in the Strait has thwarted any chance of that, while his administration’s brutish attempts to interfere with the central bank appear to have robbed it of the chance to replace Powell with someone more amenable.

The committee is now setting out its stall to behave like the Bank of England, where decisions come down to narrow majorities and the governor is sometimes in the minority. That’s not how the Fed has typically operated, but it’s a model that works elsewhere, and the bullying tactics are chiefly responsible.

Underscoring the point, Treasury Secretary Scott Bessent, who has effectively morphed into a Trump mouthpiece since his promising debut last year, attacked Powell for staying on:

It’s highly unusual for someone who says he’s an institutionalist and cares about norms at the Fed. This is a violation of all Federal Reserve norms.

It’s hard to take this seriously. Weaponising the prosecution system to get rid of Fed governors you don’t like is a much greater violation of such norms. And the Fed’s building, currently being renovated so controversially, bears the name of Marriner Eccles — a highly respected chairman who stayed on as a governor once he left the chair, just as Powell is planning.

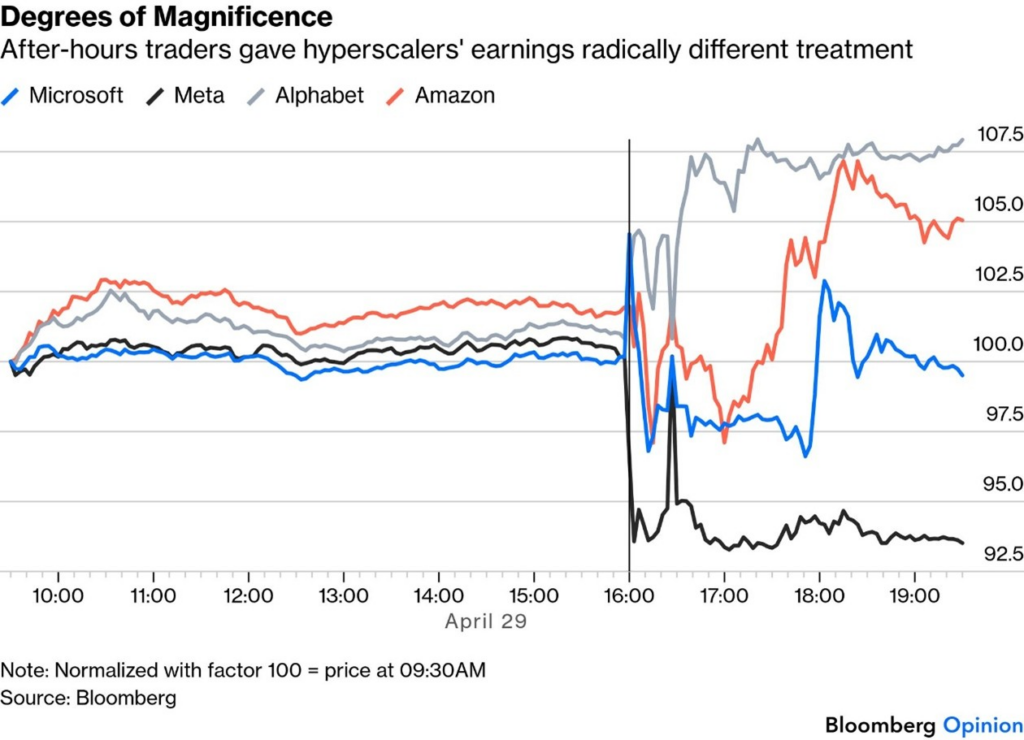

Wednesday’s mega-cap earnings delivered a familiar verdict: margins matter. Investors’ intolerance for unchecked AI-driven capital spending proved a consequential force as the after-hours reports from Meta Platforms Inc., Alphabet Inc., Microsoft Corp. and Amazon.com Inc., together worth nearly $12 trillion, offered a clearer read on the strength and the durability of the AI-driven rally.

Alphabet was the biggest winner, after delivering revenues and profits ahead of estimates. It soared by more than 7%, while others weren’t so lucky:

Behind this performance is the conviction that the company’s new generation of custom-designed chips, known as tensor processing units or TPUs, should provide additional tailwind to its artificial intelligence offering. Not only is Alphabet’s flagship AI model, Gemini, powered by these relatively lower-cost chips, but it’s also betting that broader adoption will put it in a position to challenge dominant chipmaker Nvidia Corp.

For context, Jensen Huang’s GPUs are designed for general-purpose model training, whereas Alphabet’s chips are optimised for more targeted AI inference tasks like chatbots and agents.

The significance of Alphabet’s pivot is underscored by the market reaction to Meta. It has raised spending on the back of “more expensive” components for building out its AI data centres, and now projects capex could top $145 billion this year. That’s up $10 billion from its estimates from three months ago.

This immense splurge didn’t go down well with investors, sending its shares tumbling by almost 7% in after-hours trading. That was despite sales of $56.3 billion, ahead of Wall Street’s estimate of $55.51 billion.

The key was that the solid results didn’t dispel concern that sustaining growth will come at a rising cost that eats into margins. Is it being treated unfairly?

The increase (in capex) is modest relative to Meta’s existing investment plans, comes alongside unchanged cost guidance, and sits against a backdrop of strong revenue growth and healthy margins.

Other companies received a more nuanced welcome. Take Amazon. It reported $151 billion in property and equipment expenses over the 12 months through March 31, $57.9 billion more than in the same period a year earlier. But investors viewed this favourably because Amazon’s cloud computing business needs to scale up if it’s to make more money. Sales at Amazon Web Services, which make up roughly a fifth of the company’s revenue and most of its operating profit, shot up 28% to $37.6 billion.

As the chart above suggests, traders weren’t sure what to make of Amazon. And their varying tolerance for huge spending plans suggests the demand for semiconductors may not be as limitless as the rally in chip stocks implies. We’ll find out soon enough whether these results are enough to keep the rally going in the face of so many headwinds.

Crypto in RSA under the microscope

The Draft Capital Flow Management Regulations 2026 were published on 17 April 2026. South Africa’s finance ministry has proposed a sweeping overhaul of its exchange control rules, much of which dates back to 1961, including bringing crypto assets formally into the exchange control framework for the first time, treating them as a distinct but regulated form of capital.

Key crypto-specific changes:

Why now?

National Treasury says the draft aims to move South Africa toward reporting, targeted oversight, and risk-based monitoring of high-impact cross-border flows. The JSE estimates the broader changes could attract at least R10 trillion in investment over time (sounds overly optimistic to me).

Critics say the changes raise serious constitutional concerns around privacy, property rights, and freedom of association, calling them among the most aggressive updates to South Africa’s decades-old exchange control system. Specifically, the forced-key-disclosure provision is seen as potentially conflicting with the constitutional right against self-incrimination.

Further criticism has focused on the grouping of all digital assets under a single definition of “crypto assets,” with analysts noting that decentralised cryptocurrencies like Bitcoin differ significantly from centrally issued stablecoins.

The National Treasury has invited public comment, with stakeholders having until 10 June 2026 to provide feedback before the regulations are finalised. I have often written about RSA’s antiquated forex controls, which put them in the minority globally and in the august company of China, Zimbabwe, Russia and India.

Interestingly, South Africa actually accepted Article VIII obligations (moving away from Article 14) years ago, meaning it formally committed to currency convertibility. However, it retained its 1961-era exchange control framework as a domestic policy tool, operating somewhat in tension with that commitment. That’s part of why the 2026 overhaul is framed as a modernisation, bringing the practical rules in line with SA’s international obligations, rather than just tightening control for its own sake.

These new regulations obviously have significant implications for our clients, and we will keep a close eye on developments. I suspect that this is going to be tied up in the constitutional court for a good many years.

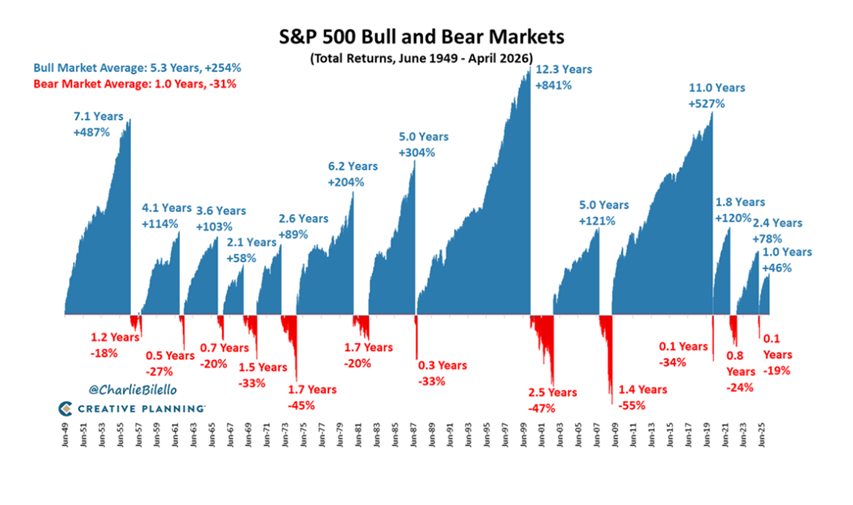

Whenever markets surge optimistically ahead, oblivious of what normies might consider ‘normal risk’ – like the impending oil crisis (we haven’t seen anything yet if that 20% supply isn’t restored soon) – I am reminded to look at history.

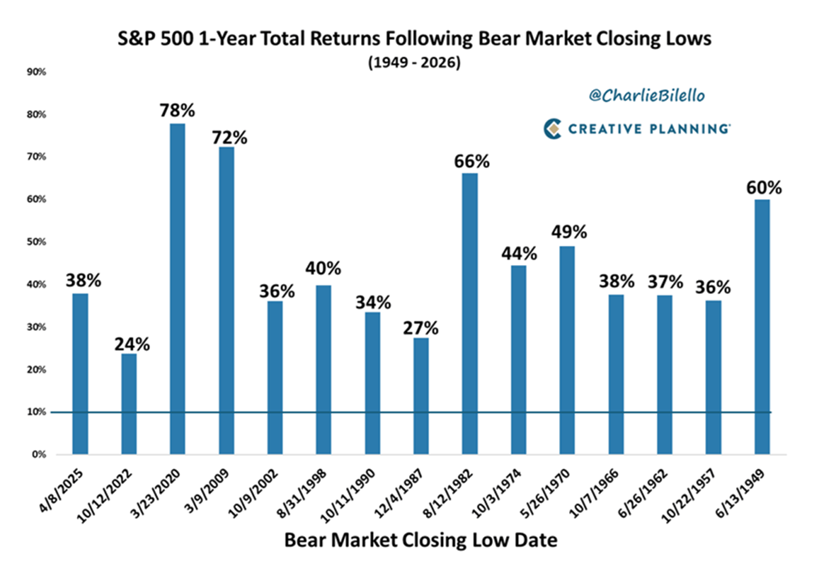

I came across the graph below last week, and it served as a reminder that while cycles always happen, the ‘Bear Markets’ are mercifully shorter than the ‘Bull Markets’. Of course, we have had at least 3 orange swan events in the last 18 months that have made investors’ lives ‘interesting’ to say the least.

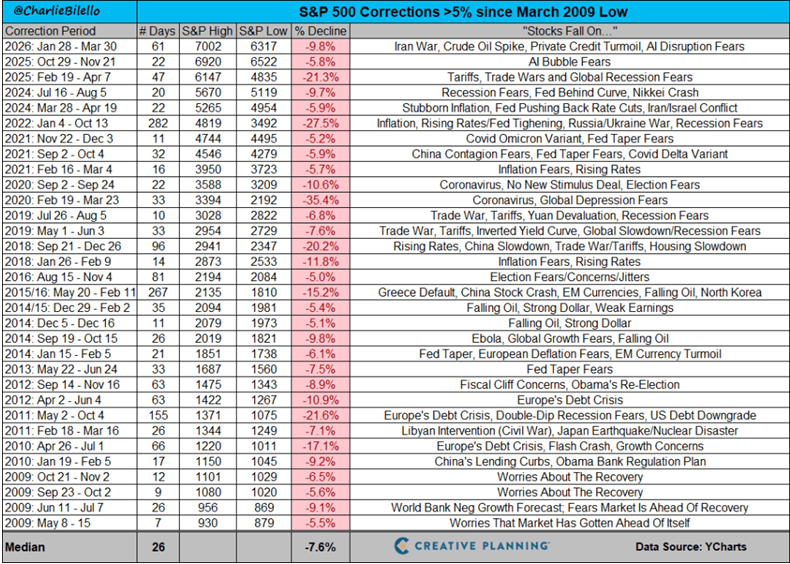

The table below provides a bot with more details on what triggered Corrections (>10% decline) rather than full Bear markets (>20% decline). Note that 2017 is the only year in which there was no correction of over 5%.

If you want more reassurance, check the table below that shows the return one year after the Bear market hit its final low.

Author: Dawn Ridler

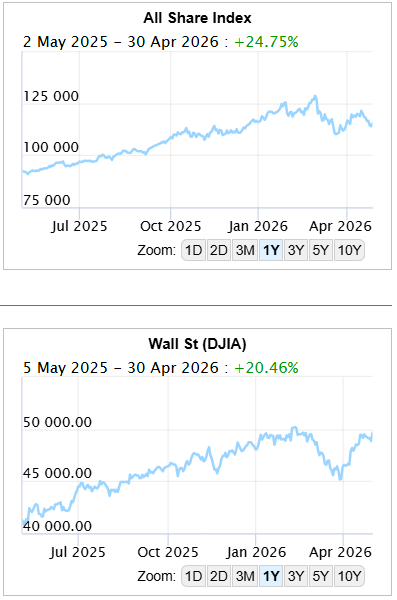

Global stock markets have rallied strongly in April with the MSCI ACWI hitting an all-time high, predominantly driven by its US component. This is as large tech companies have all gained north of 15% in the month.

What should puzzle investors is that this is all happening whilst the Strait of Hormuz continues to be a victim of the US/Iran conflict. Oil prices, despite weakening on the hopes of an imminent opening has stayed at about $100. The conflict has led to second-order effects as well. Consider that the UAE (United Arab Emirates) have opted to leave the oil cartel OPEC, which has been the body providing pricing stability to oil for the last 66 years.

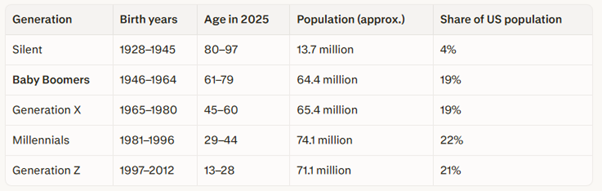

All of this should have seen markets at lower levels, but despite this, we are seeing markets at all-time highs. The one reason for this is that the Federal Reserve seems to have provided some liquidity as a response to the Iran conflict through their Reserve Management Purchases (RMP) mechanism. Combine this with lower bond market volatility and markets have had some reason to increase in value. But this won’t necessarily last. The FED has warned that they will fade their RMP efforts but even if they should continue these, consider the new FED Chair, Kevin Warsh and his promise to return the FED to a more traditional role away from the provision of market liquidity. This may be easier said than done given that the US economy is more reliant on a stable stock and bond market than ever before. If markets fall, tax revenues will falter and excess volatility will make the refinancing of bonds more difficult. This is a federal government issue. But leading on from this, consider that baby boomers make up a sizable portion of the US population:

At 19% of the population, this group has lived the American dream and relies heavily on the US stock market going up in value to fund their retirement income. If this becomes impeded, the US government will be called upon to provide extra funding.

All of this leaves us with a system which is heavily reliant on market stability. The one criticism investor have for markets at present is their cost. The S&P500 is trading at a P/E of 25x, showing an elevated valuation based on its history. But also consider that forward estimates for earnings are rising. For the MSCI USA, estimates have jumped by 23% y-o-y, whereas for the rest of the world, by 25%. If this continues, markets will continue to price in this growth.

The latest results from Meta showed a 33% y-o-y growth in Revenue, Amason’s AWS unit showed a Q1 Revenue growth of 28% and Alphabet grew cloud by 63%. These are not trivial growth numbers and markets are pricing for this growth at present.

It is one thing that ties all of this together: markets may generate a flat return in 2026. The current valuations suggest headwinds for markets, but this is heavily dependent on the pace at which earnings continue to materialise and on liquidity injections.

Time will tell, but this is why long-term equity holders ultimately benefit, as they have the enviable position to remove noise from the long-term growth story, which is unfolding.

Author: Cobie Le Grange

EXCHANGE RATES and other Indices:

The Rand/Dollar closed at R16.63 (R16.29, R16.41, R17.07, R17.06, R16.89, R16.55, R15.93, R16.01, R15.96, R16,03, R16.15, R16.10, R16.50, …R16.91, R17.13, R17.36, R17.13,16.52 R17.27, R17.31, R17.25, R17.38, R17.50, R17.22 , R17.35, R17.33, R17.37, R17.58, R17.65, R17.44, R17.61, R17.74, R18.15,R17.76, R17.72, R17.90, R17.58, R17.89, R17.99, R17.92, R17.77, R17.95, R17.88)

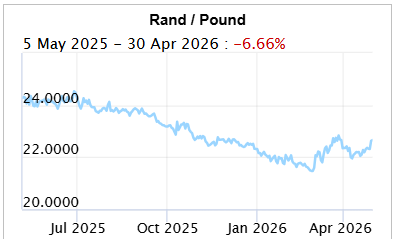

The Rand/Pound closed at R22.56 (R22.35, R22.02, R22.09, R22.77, R22.76, R22.35, R22.20, R21.48, R21.59, R21.78, R21,82, R22.11, R21.97, R22.13, …R22.57, R22.68, R22.74, R22.56, R22.69, R22.76, R22.96, R23.34, R23.37, R23.19, R23.22, R23.35, R23.55, R23.73, R23.84, R23.53, R23.84, R23.84, R24.09, R23.88, R23.76, R24.22, R24.08, R24.49, R24.22, R24.35, R24.05, R24.18)

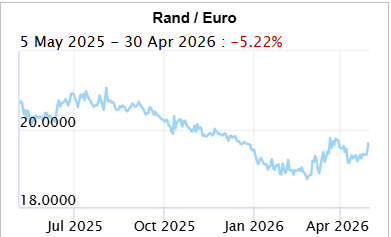

The Rand/Euro closed the week at R19.48 (R19.37, R19.17, R19.24, R19.70, R19.77, R19.33, R19.23, R18.80, R18.87, R18.94, R18.93, R19.14, R19.04, R19.20, …R19.68, R19.86, R19.99, R19.96, R19.98, R20.02, R20.06, R20.26, R20.33, R 20.22, R20.30, R20.35, R20.38, R20.61, R20.62, R20.44, R20.56, R20.64, R21.04, R20.86, R20.61, R20.93, R 20.70, R20.91, R20.74, R20.68, R20.24, R20,37)

Brent Crude: Closed the week $108.83 ($105.33, $90.38, $95.20, $107.88, $112.36, $103.14, $92.88, $73.19, $71.76, $67.75, $68,05, $69.32, $65.88, $63.34, …$63.71, $63.19, $62.42, $63.94, $63.61 $64.66, $65.04, $61.27, $62.14, $64.28, $69.67, $66.57, $66.80, $65.52, $67.38, $67.73, $66.08, $66.07, $69.46, $68.29, $69.21, $70.58, $68.27, $67.39, $77.27, $74.38, $66.56, $62.61, $65.41)

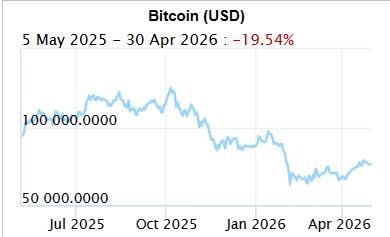

Bitcoin closed at $78,204 (78,049.98, $75,519, $70,904, $68,691 , $68,586, $70,869, $67,310, $63,534, $68,04, $69,649, $68,553, $81,301, $89,295, $90,585, … $90,809, $86,334, $94,990, $101,562, $109.936, $112,492, $106,849, $111,888, $124,858, $109,446, $115,838, $115,770, $110,752, $108,923, $114,916, $117,371, $118,043, $113,608, $118,139, $118,214, $117,871, $108,056, $107,461, $103,455)

Articles and Blogs:

Dos and Don’ts of Wills and Estate Planning NEW

Planning your legacy, starting with your will NEW

Holiday checklist

Next year – Action Plan

Next year – Vision, Mission etc

Medical Risk Mitigation

Next Year – Consolidation

Abdication or diversification?

Carbo-loading your retirement

Spoiled for choice

Who needs a plan anyway

8 questions you need to ask about retirement

What to do when interest rates drop

How to survive volatility in your investments

What to do when interest rates drop

Difficult Financial Conversations

Financial Implications of Longevity

Kick Start Your Own Retirement Plan

You matter more than your kids in retirement

To catch a falling knife

Income at retirement

2025 Budget

Apportioning blame for your financial state

Tempering fear and greed

New Year’s resolutions over? Try a Wealth Bingo Card instead.

Wills and Estate Planning (comprehensive 3 in one post)

Pre-retirement – The make-or-break moments

Some unconventional thoughts on wealth and risk management

Wealth creation is a balancing act over time

Wealth traps waiting for unsuspecting entrepreneurs

Two Pot pension system demystified

Cobie Legrange and Dawn Ridler,

Rexsolom Invest, Licensed FSP 45521.

Email: cobie@rexsolom.co.za, dawn@rexsolom.co.za

Website: rexsolom.co.za, wealthecology.co.za