The Legacy Series eBook is ready (free on request).

Too Busy? Got Better Things to Do? Read the Summary…

This Week’s Roundup: The SARB hiked the repo rate by 25bp to 7% on 28 May — its first hike since 2023 — with four of six MPC members in favour. SA inflation jumped to 4.0% in April (from 3.1% in March), inflation forecasts were raised to 4.4% for 2026, and growth forecasts cut to 1.2%. SA’s Q1 trade surplus trebled to R77 billion year-on-year. In the US, Q1 GDP was revised up sharply to 2.0% from 0.5%. April PCE rose to 3.8% year on year. Fresh US military strikes on Iran drove oil 2–3% higher. The IEA projected global oil inventories would fall 8.5 million barrels per day in Q2. Emerging market growth forecasts were cut to 3.9% while EM inflation was revised up to 5.5%.

Winning, Bigly: A tentative US-Iran deal (described wryly as “Version 10.543”) would extend the ceasefire by 60 days and open nuclear talks, but Trump had not yet agreed to the terms. Key sticking points remain: Iran’s nuclear programme, the return of $24 billion in frozen assets, and Trump’s own “three red lines” — reopening the Strait, surrendering enriched uranium, and ending the nuclear programme. Iran’s parliament speaker has continued to mock US claims of progress publicly. The newsletter is sceptical, concluding simply: “Yup, winning!”

Guard Rails Gone: US equity markets have effectively decoupled from the Iran war, with stocks rallying even as oil prices remain elevated. The driving force is AI earnings, which have overridden geopolitical risk as the primary market signal. Bonds, however, continue to track oil prices as a proxy for future inflation. Neither the stock market nor the bond market is currently imposing meaningful pressure on the Trump administration to end the conflict. With markets buoyant, hawkish Republican voices urging against a deal are gaining influence — ironically, market resilience is slowing the path to peace.

Not So Precious: Gold has lost nearly a fifth of its value since its late-January all-time high, trading only ~3% above its year-start level despite extreme geopolitical risk. Key headwinds include speculative position unwinding, tighter monetary policy expectations, a stronger dollar, and potential central bank gold sales to raise liquidity. The long-term bull case remains intact — rising money supply and credit creation provide structural support — but consolidations after major runs can last 12–24 months. Silver has also collapsed after a speculative surge. The newsletter concludes that precious metals are not the most compelling positioning at this time.

RSA Rate Hike: A detailed explainer on the SARB’s 25bp hike to 7%. The key insight is that this is not a response to demand-led inflation — which SA hasn’t experienced in decades — but a pre-emptive defence of the rand against imported inflation from elevated global oil prices. The SARB modelled three risk scenarios: a prolonged Strait closure pushing inflation to ~5% (requiring two extra hikes); the same with El Niño drought added (rates higher for longer); and a worst-case scenario combining all risks, pushing inflation above 6% and requiring three extra hikes. The SARB reiterated its commitment to returning inflation to its 3% target over time.

Ferrari at a Crossroads: Ferrari’s launch of the all-electric Luce — designed by Jony Ive and Marc Newson of LoveFrom — has been received extremely poorly. Priced at $640,000, its technical specifications are easily matched by far cheaper competitors, and critics argue the car fundamentally contradicts Ferrari’s core brand values of speed and passion. Former CEO Luca di Montezemolo warned it “risks destroying a legend.” The newsletter outlines three paths forward: write it off as a misstep (brave but probably right); push through with it as a deliberate brand disruption; or rebadge it under a different marque, as Ferrari did with the Fiat Dino in 1967. Ferrari’s share price is down 27% over the past year, trading at 33x earnings — not cheap. How management handles this misstep will be a critical test of their quality.

Unfortunately, economics, markets and economics are inextricably linked, so as much as we might be sick to death of the spin coming out of the White House construction site in the DC, it still moves markets and affects our portfolios

As of Friday, the US and Iran have reached a tentative deal (Version 10.543) to extend a ceasefire by 60 days and launch further talks on Tehran’s nuclear program, raising hopes the three-month conflict could be nearing a resolution. President Donald Trump has yet to agree to the terms. Both countries have previously hailed progress, with Trump repeatedly indicating the US was close to securing an agreement, only for the standoff to drag on.

Vice President JD Vance told reporters Thursday that the US and Iran are “going back and forth on a couple of language points,” including over issues relating to Tehran’s nuclear capabilities. He said Iran appears to be negotiating in good faith, adding that progress is being made.

Iran’s semi-official Tasnim news agency said in a post on X that the text of the possible memorandum of understanding between the US and Iran had not been finalised, citing a source it did not identify.

Scott Bessent, somehow managing to find the time to get involved in political shenanigans on his time off from his small day job as US Treasury Secretary, declined to say whether an interim deal had been reached, offering only that negotiations were continuing. He reiterated that Trump’s three “red lines”- reopening the Strait of Hormuz, Iran’s surrendering highly enriched uranium and ending its nuclear program- remain prerequisites for any agreement.

The US and Iran have had a fragile truce in place since early April, which has been interrupted by isolated military strikes. Axios reported that Trump asked for “a couple of days” to think about the agreement. Trump finds himself caught between Iranian demands for financial relief (not in place before the ‘excursion) and an end to attacks, pressure from Republican hawks not to compromise, and his own past criticism of similar agreements (especially those made by ‘Barack Hussein Obama’). Beyond Tehran’s nuclear program, negotiators still need to decide how much of Iran’s $24 billion in frozen assets will be released and how quickly. Yup, winning!

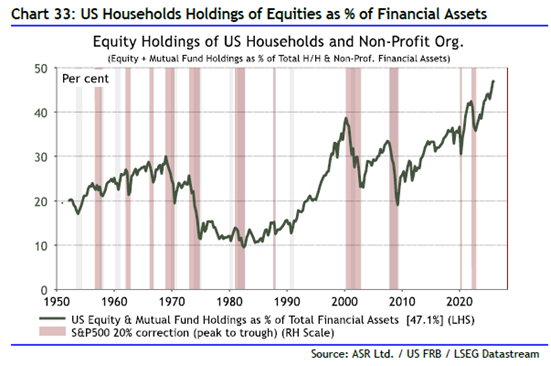

If anything might have imposed guardrails to limit Donald Trump’s actions, the conventional wisdom goes, it’s the global capital markets. No president likes overseeing a bear market in stocks, least of all this one. That’s particularly true as households’ holdings of equities reach fresh records.

Families now have a higher proportion of their financial assets in the stock market than even at the top of the dot-com bubble in 2000, as the following chart illustrates:

The standard argument runs that this gives the market even more power over politicians. With families this exposed to the stock market, any sell-off will have that much more impact on their finances, made transparent daily through 401(k) and exchange-traded fund prices.

Borrowing from the language of options, the idea is that no president will be prepared to continue with policies that prompt serious market damage. There will come a price at which politicians will bring the selloff to an end by U-turning on policy, much like writing a put option. However, Trump is about as far removed from an ordinary politician or president as you can get.

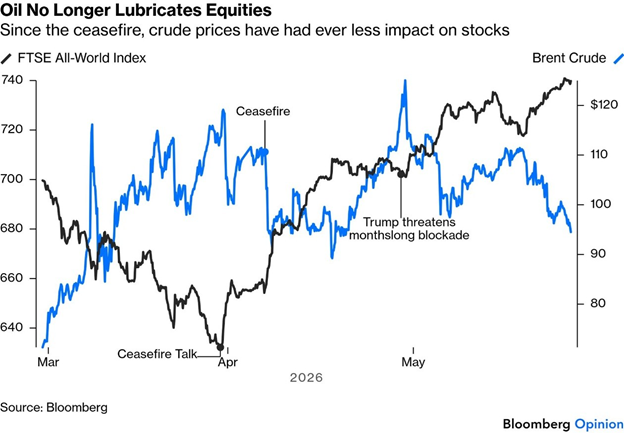

But the markets have ceased to be a factor in the administration’s decisions over the most pressing policy of the moment, the war in Iran.

After selling off sharply in the first month of the conflict, equities turned around at the end of March as the US and Iran signalled interest in pursuing peace. Stocks have since rallied consistently, seemingly impervious to events in the Gulf.

That grew clearer than ever after a renewed sharp fall in crude prices last Wednesday was greeted with near-total indifference on Wall Street. The stock market was almost perfectly flat for the day.

Why has oil ceased to matter? The most important factor, by far, is the countermanding shock from artificial intelligence, which has recently driven extraordinary gains for chip stocks. Stocks react to profits and earnings forecasts, both of which have improved markedly since the conflict started, so the Strait of Hormuz becomes a little less salient, in the US, anyway.

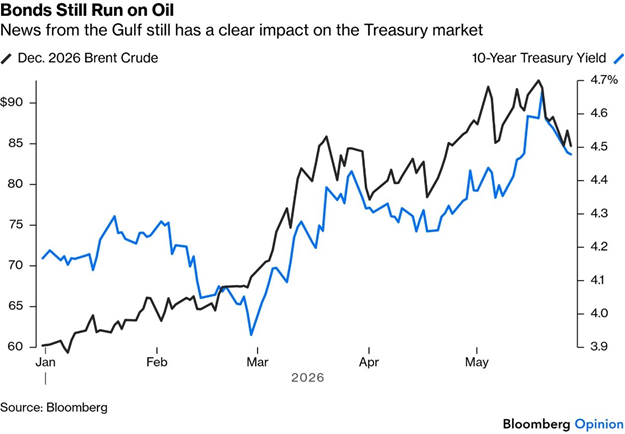

Bonds are different. Treasuries continue to take cues from oil prices for a few months hence, as a sustained increase would bring the greatest risk of raising embedded inflation expectations. The 10-year yield has clearly followed the path of December crude prices, although even here, there are signs that the effect is growing duller:

The bond market can be an even tighter leash on government behaviour than stocks, but it requires a fast and significant rise in yields to force changes in policy. That notoriously brought down British Prime Minister Liz Truss in 2022, while Trump admitted that he delayed imposing last year’s Liberation Day tariffs because the bond market was “yippy”, the start of the ‘TACO’ acronym. But they’re not imposing any limits on him at present.

Investors are more and more convinced that the American economy is recession-proof, and it’s powered by this weird ability to hold on to jobs despite everything.

Measures such as initial claims and the unemployment rate have stayed well under control throughout last year’s trade war and the current conflict.

The last shock, from the pandemic, may still be affecting behaviour. US employers discovered how difficult it was to rehire people once they’d been laid off, and may now be over-compensating. That helps keep the economy and the stock market buoyant. Much rides on the wealth currently being created for Americans in stocks, and many investors would dearly love to see Hormuz reopen before more significant economic damage is done. But the self-contradictory logic at present is that market confidence in the economy has relieved some of the pressure to reach a deal. In the absence of market pressure, the voices of hawkish Republicans counselling that the deals on the table look like defeat become more persuasive. That’s one of the many reasons why it’s taking a long time.

Since it surged to an all-time high in late January, gold has shed nearly a fifth of its value. The fallout from the war has taken centre stage in explaining the decline, but it doesn’t tell the full story. After the speculative boom, investors had begun unwinding bullish positions even before the first bombs fell on Tehran.

Gold even staged a small rally as the conflict got underway, in line with its traditional role as a safe haven amid geopolitical uncertainty. But it fell short of reclaiming its all-time highs before the reality of the ensuing energy shock drove a significant selloff. Still above its 200-day moving average, it remains unclear whether it’s settled into a downward trend.

Gold has largely traded sideways for several weeks, up only about 3% year-to-date — despite continuing extreme geopolitical risk. At least two factors explain this. First, after gold’s capitulation from its late-January high, speculators wanted to take opportunities to lighten their position. Second, and most important, was the prospect of tighter monetary policy stemming from a prolonged disruption in the Strait. Inflation, all else equal, should help real assets like gold, but many stayed on the sidelines because of the likely effect on central banks.

The dollar and gold tend to have an inverse relationship, so the currency’s strength since the conflict started also tends to weaken the gold price. Then, central banks in need of liquidity may raise cash by trimming their gold holdings. Together, these dynamics provide a compelling case for a short-term pullback.

In the long term, the rising money supply and credit creation provide support and balance. That is only going one way, so the long-term gold bull market remains underpinned. But the elephant in the room is that gold had its best year in 2025 since 1979. A soft patch is fair game. Consolidations can last for 12 months to two years.

Silver, which has also collapsed after an exceptional speculative surge, could be set for a rebound. Precious metals no longer appear the most compelling positioning at this time. For investors, a swift resolution of the Iran conflict would help clear the noise that has increasingly obscured underlying fundamentals.

The South African Reserve Bank’s (SARB) Monetary Policy Committee (MPC) raised the benchmark repo rate by 25 basis points on Thursday, taking it to 7% from 6.75%.

The decision lifts the prime lending rate to 10.5%.

The move comes amid growing inflation risks linked to persistently high oil prices and the ongoing conflict in the Middle East, which have pushed up fuel costs and heightened concerns about broader price pressures feeding through the economy.

The MPC’s decision aligns with expectations from several economists and market participants, who argued that the central bank would act pre-emptively to contain inflation expectations and limit the risk of second-round effects.

Sarb governor Lesetja Kganyago said in his statement that four committee members favoured a rate hike, while two preferred no change. Asked whether a 50 basis point hike had been on the table, Kganyago said it had featured in a robust discussion.

“The committee agreed that inflation risks had intensified, and that the challenge of large and overlapping shocks would likely trigger second-round effects, requiring a monetary policy response.”

“Our decision was aimed at managing risks and ensuring that inflation returns to target,” he added.

For this meeting, the MPC explored three risks.

The first was a prolonged Middle East crisis, which would result in higher food and oil prices and a weaker rand. Remember that the SARB has a dual mandate, inflation control and rand protection. The price of oil is an imported inflationary effect over which RSA has little control, but any surge in inflation will impact the exchange rate. So, the rise in interest rate is not to cool an overheated economy with demand-led inflation (which we haven’t seen in decades anyway) but to protect the Rand. Protecting the Rand has a direct impact on that imported inflation.

The SARB has several reasons to want to protect the rand’s value.

In short, for a small open emerging market economy like South Africa, the exchange rate is one of the most powerful transmission mechanisms for inflation, making it central to monetary policy decisions.

The second consideration is that El Niño, a weather pattern that appears to be forming and typically brings drought to parts of South Africa.

The third added so-called “non-linear effects” – the risk that large shocks could have disproportionately bigger effects on inflation, with more costs passed on to consumers.

Policy would therefore need to strike a balance between supporting economic activity and guiding inflation back to target over time.

Under the scenario of a prolonged closure of the Strait of Hormuz, inflation would rise to about 5%, requiring two more rate hikes than the baseline. With El Niño added, rates would remain higher for longer.

The most adverse scenario combined all these risks, causing inflation to peak above 6% and requiring three extra hikes, he said.

The scenarios underscored the role of food, alongside fuel, in transmitting the ongoing geopolitical shock, while also highlighting the added risks posed by a severe El Niño.

The MPC noted that the world had already experienced one global inflation surge this decade and could be at the start of another.

In such conditions, it said, it is crucial that central banks maintain their credibility and prevent higher inflation from becoming entrenched. “Although we do not have the tools to prevent the initial effects of supply shocks, monetary policy is responsible for longer-run inflation. We take this duty seriously, and reiterate our commitment to bringing inflation back to 3%, over time,” Kganyago added.

Author: Dawn Ridler

A company I have long admired is Ferrari, listed under the appropriate ticker code: RACE. And this is what the brand is all about…. Racing. And then Ferrari is also about passion and the love of beautiful machines, which can operate at the highest level. This is at the heart of the company and is borne out of their love for Formula 1 motor racing. It’s a brand which relies heavily on performance and the attitude of the Ferrari “tifosi”, the hardened race supporters arriving in red to support their team.

The love of the brand starts at a young age. Ferrari is associated with speed and passion. Children start their love affair with these red machines by putting a poster of an insanely expensive Ferrari on their wall. At that moment, that kid dreams of becoming a Ferrari owner. And for some of us, that dream never ends, and at its ultimate conclusion, may end up with ownership of multiple Ferraris. Let’s put all of this into numbers:

Ferrari is a cash machine. The brand sustains the sales momentum and the scarcity factor associated with the ownership of some of their high-end models by keeping Ferrari aficionados engaged and interested in owning their next car. They only sell about 13,500 cars per year, and the average selling price is about $500k. But to entice the next loyal fan to fulfil his dream requires a lineup of cars that will make him part with hard-earned cash. It has to fulfil the passion which the brand is so synonymous with.

So the launch last week of the Ferrari Luce, their all-electric vehicle, has many scratching their heads. Jony Ive, who designed the iPhone designed the car alongside Marc Newson. Together they formed a design colab called LoveFrom which is the main design thrust behind the Luce. Many commentators can see the resemblance between the iPhone and the Luce but this should be seen as something tragic for Ferrari. If Ferrari were a car brand synonymous with efficiency, maybe this would fly. Alas, it doesn’t, and the core brand values of Ferrari aren’t represented by the Luce in any shape or form.

Then there is the price. The car is selling for $640,000 and has technical specifications which are easily beaten by competing electric cars at a fraction of the cost. The most prolific comparison I have seen is with the Nissan Leaf ($39,000 for the high-end model). The irony in the image below will tell you all about the reception this car has had:

This now leaves the owner of the prancing horse with a few choices.

They could write this all off as a misstep. The problem is that their production plant has been retooled and the cost of development has now become a sunk cost. It takes a brave company to do this, but it is probably the right thing in the long run, given the fierce brand loyalty of Ferrari owners. I would probably rethink who I hire for brand research in the future, too.

The second choice would be to push through. Flavio Manzoni, part of Ferrari’s own design, has framed the Luce as a deliberate disruptive break from tradition. The car is about efficiency rather than nostalgia aimed at a new possible customer. And perhaps the future of Ferrari is an all-electric, efficient lineup of cars. I can’t see it, and their loyal brand owners, I don’t think, will be able to see it either.

And the third option is to make this a joint project. This is where the Ferrari brand is dropped from the car and replaced by a possible Renault badge (Nissan would be an immediate design fit… just a thought). One can still keep the fact that it was designed by Ferrari, as was the case with the Fiat Dino, which was produced in 1967. The engine in this case was Ferrari but the badge said Fiat.

The famed previous CEO of Ferrari, Luca di Montezemolo after seeing the Luce said that if he truly spoke his mind, he would “harm Ferrari,” that the Luce “risks destroying a legend,” and that he hopes they remove the Prancing Horse from that car, adding that it is at least a car “the Chinese won’t copy.” I think this would be echoed by the Tifosi. How a company deals with a misstep tells one a lot about the quality of management. The share price is down by -27% over the last year. This isn’t necessarily about the Luce alone, as the company has historically traded at expensive multiples, attracting valuations of 50x earnings. Currently, it’s trading at 33x earnings, a similar valuation metric to some AI-powered companies. So I wouldn’t frame Ferrari’s price today as cheap, but management action is going to be critical to holding onto this valuation.

Author: Cobie Le Grange

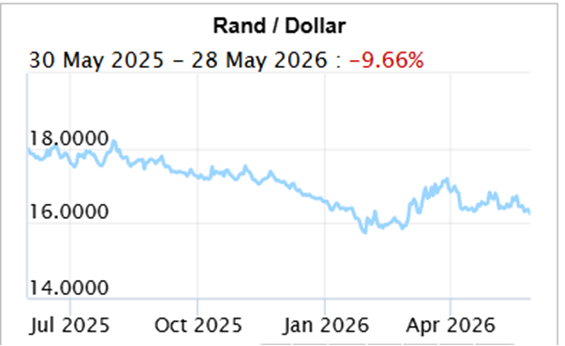

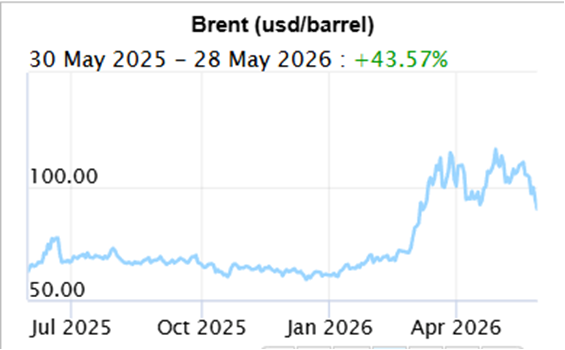

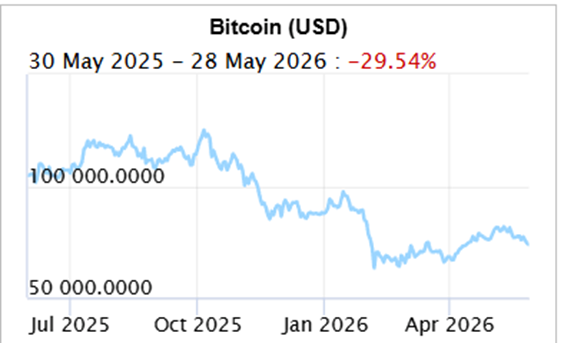

EXCHANGE RATES and other Indices:

The Rand/Dollar closed at R16.23 (R16.46, R16.68, R16.39, R16.63, R16.29, R16.41, R17.07, R17.06, R16.89, R16.55, R15.93, R16.01, R15.96, R16,03, R16.15, R16.10, R16.50, …R16.91, R17.13, R17.36, R17.13,16.52 R17.27, R17.31, R17.25, R17.38, R17.50, R17.22 , R17.35, R17.33, R17.37, R17.58, R17.65, R17.44, R17.61, R17.74, R18.15,R17.76, R17.72, R17.90, R17.58, R17.89, R17.99, R17.92, R17.77, R17.95, R17.88)

The Rand/Pound closed at R21.80 (R22.09, R22.21, R22.30, R22.56, R22.35, R22.02, R22.09, R22.77, R22.76, R22.35, R22.20, R21.48, R21.59, R21.78, R21,82, R22.11, R21.97, R22.13, …R22.57, R22.68, R22.74, R22.56, R22.69, R22.76, R22.96, R23.34, R23.37, R23.19, R23.22, R23.35, R23.55, R23.73, R23.84, R23.53, R23.84, R23.84, R24.09, R23.88, R23.76, R24.22, R24.08, R24.49, R24.22, R24.35, R24.05, R24.18)

The Rand/Euro closed the week at R18.91 (R19.11, R19.38, R19.29, R19.48, R19.37, R19.17, R19.24, R19.70, R19.77, R19.33, R19.23, R18.80, R18.87, R18.94, R18.93, R19.14, R19.04, R19.20, …R19.68, R19.86, R19.99, R19.96, R19.98, R20.02, R20.06, R20.26, R20.33, R 20.22, R20.30, R20.35, R20.38, R20.61, R20.62, R20.44, R20.56, R20.64, R21.04, R20.86, R20.61, R20.93, R 20.70, R20.91, R20.74, R20.68, R20.24, R20,37)

Brent Crude: Closed the week $91.12 ($104,24, $109.26, $101.29, $108.83, $105.33, $90.38, $95.20, $107.88, $112.36, $103.14, $92.88, $73.19, $71.76, $67.75, $68,05, $69.32, $65.88, $63.34, …$63.71, $63.19, $62.42, $63.94, $63.61 $64.66, $65.04, $61.27, $62.14, $64.28, $69.67, $66.57, $66.80, $65.52, $67.38, $67.73, $66.08, $66.07, $69.46, $68.29, $69.21, $70.58, $68.27, $67.39, $77.27, $74.38, $66.56, $62.61, $65.41)

Bitcoin closed at $73,788 ($74,559, $77,879, $80,733, $78,204, $78,049.98, $75,519, $70,904, $68,691 , $68,586, $70,869, $67,310, $63,534, $68,04, $69,649, $68,553, $81,301, $89,295, $90,585, … $90,809, $86,334, $94,990, $101,562, $109.936, $112,492, $106,849, $111,888, $124,858, $109,446, $115,838, $115,770, $110,752, $108,923, $114,916, $117,371, $118,043, $113,608, $118,139, $118,214, $117,871, $108,056, $107,461, $103,455)

Articles and Blogs:

Legacy Series Part 4 NEW

Legacy Series part 3

Legacy Series Part 2

Legacy Series Part 1

Holiday checklist

Next year – Action Plan

Next year – Vision, Mission etc

Medical Risk Mitigation

Next Year – Consolidation

Abdication or diversification?

Carbo-loading your retirement Spoiled for choice

Who needs a plan anyway

8 questions you need to ask about retirement

What to do when interest rates drop

How to survive volatility in your investments

What to do when interest rates drop

Difficult Financial Conversations

Financial Implications of Longevity

Kick Start Your Own Retirement Plan

You matter more than your kids in retirement

To catch a falling knife

Income at retirement

2025 Budget

Apportioning blame for your financial state

Tempering fear and greed

New Year’s resolutions over? Try a Wealth Bingo Card instead.

Wills and Estate Planning (comprehensive 3 in one post)

Pre-retirement – The make-or-break moments

Some unconventional thoughts on wealth and risk management

Wealth creation is a balancing act over time

Wealth traps waiting for unsuspecting entrepreneurs

Two Pot pension system demystified

Cobie Legrange and Dawn Ridler,

Rexsolom Invest, Licensed FSP 45521.

Email: cobie@rexsolom.co.za, dawn@rexsolom.co.za

Website: rexsolom.co.za, wealthecology.co.za