The Legacy Series eBook is ready (free on request).

Too Busy? Got Better Things to Do? Read the Summary…

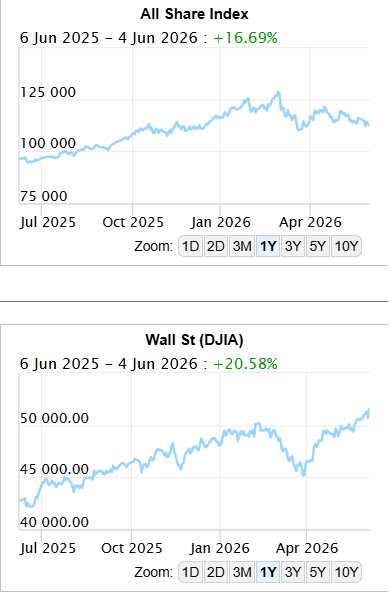

This Week’s Roundup: SA inflation hit 4.0% in April, household debt stress is deepening with 41% of credit-active South Africans in default, and the JSE is lagging Wall Street. In the US, Q1 GDP was revised down to 1.6%, PCE rose to 3.8%, and Kevin Warsh was sworn in as Fed Chair 54–45. Brent crude fell ~19% in May on ceasefire progress. Markets price a 97% ECB rate hike probability on 11 June.

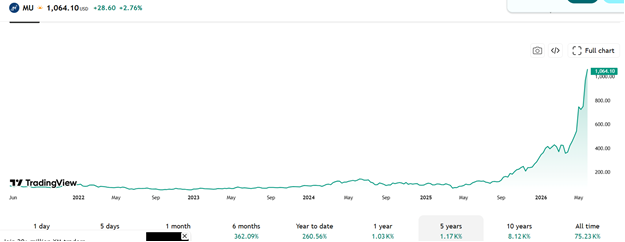

Micron and Broadcom – AI Jitters: Micron crossed $1.2 trillion in market cap in a week. US market outperformance is entirely attributable to tech — strip it out and the S&P is below three-month-ago levels. Broadcom disappointed with AI revenue guidance below expectations despite a $270 billion pre-earnings rally.

The Price of Using AI and the Rate of Return Debate: AI ROI remains unproven. Uber, Walmart and others have capped AI tool usage after costs spiralled. Bain’s report summarises it bluntly: Your AI Budget Is Growing. Your Returns Aren’t. AI has become a metered utility bill, and companies are being forced to justify the expense.

Still Worried About AI Job Losses?: Four years after ChatGPT, there is no measurable employment displacement in official data. AI-driven layoffs were just 5% of total 2025 job cuts. Schumpeter’s creative destruction framework suggests human ingenuity will prevail — the jobpocalypse hasn’t started yet.

SpaceX: SpaceX’s ~12 June IPO at a $1.8 trillion valuation faces scrutiny after its merger with loss-making xAI. Capex doubled revenues in Q1 2026, debts stand at $29 billion, and ambitions include space-based data centres and a $100 billion chipmaking plant. Buying in at 90x revenues is a pure faith-based bet.

Spending those dollars: Google’s $80 Billion Capital Raise Google is raising $80 billion via equity — $30 billion in a public offering, $40 billion at-the-market from Q3 2026, and $10 billion direct to Berkshire Hathaway — all earmarked for AI capex. Despite strong cash generation and access to bond markets, management chose to dilute shareholders, likely because rising yields made equity cheaper. Issuing stock at 28x earnings is a meaningful ask. With SpaceX, Anthropic and OpenAI also eyeing public markets, the AI capital frenzy is building — and history warns that massive build-outs typically create excess capacity before demand catches up.

Micron and Broadcom – AI jitters Last week, Micron Technology Inc. had just topped a trillion dollars in market cap. Micron Technology is one of the world’s largest semiconductor companies, specialising in memory and storage chips — primarily DRAM (Dynamic Random Access Memory) and NAND flash storage.

Graph : Micron Techologies

Founded in 1978 and headquartered in Boise, Idaho, Micron makes the chips that power everything from data centers and AI servers to smartphones, laptops, and cars. Their products are essentially the “memory” that computers use to process and store data at speed. In this fast moving world, Seven days is a long time. It’s now topped $1.2 trillion. The last week’s growth is equivalent to the entire market valuation of companies like McDonald’s Corp. or Verizon Communications Inc.

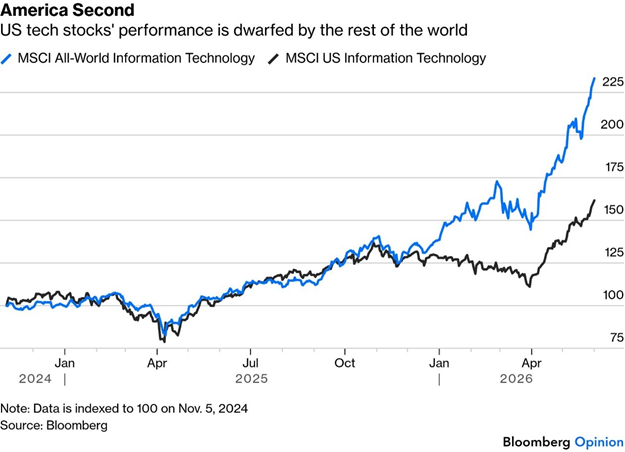

What’s interesting is that this “AI” effect doesn’t respect geography. Since the 2024 presidential election, the IT sector for the world as a whole has done far better than the US IT index alone, according to MSCI:

This is because the US is particularly dominant in software groups, which are perceived to be likely victims of AI and have endured a major selloff.

Tech sectors elsewhere can luxuriate in the demand for chips.

Focusing on the semiconductor sector itself, there are other big players, particularly in South Korea and Taiwan. The US industry has done no better than global semiconductors as a whole.

Annoyingly, the US stock market has emerged from the war’s first three months in far better shape than the rest of the developed world. There appears to be a clear geographical reason for this: The US isn’t dependent on imported oil via the Strait while Europe and the Far East are deeply exposed. That lack of supply is really going to start to hit the rest of the world unless the straits are opened soon. US outperformance during that time proves to be entirely attributable to its tech sector. Exclude it, and the S&P is below its level from three months ago and has barely made up any ground on the EAFE (Europe, Australia and the Far East) index.

Enjoy it while it lasts; no amount of technical advances can keep any market advancing as quickly as this forever. But for now, the strength is overwhelming and helping to tide the capital markets through some dire straits.

Broadcom Inc. shares fell in extended trading after the company delivered a disappointing forecast for artificial intelligence chip revenue, signalling its efforts to gain ground in the burgeoning industry are going more slowly than anticipated.

Chief Executive Officer Hock Tan said Broadcom will sell $56 billion in AI chips in the fiscal year that ends in October. That forecast fell short of the average estimate of $57.6 billion.

Though the company is making headway in pivoting to artificial intelligence customers, it’s up against outsized investor expectations. Broadcom added roughly $270 billion in market value over the last five trading sessions before the earnings report, fueled by AI optimism.

Broadcom has signed and expanded long-term deals with companies like Alphabet Inc.’s Google, Anthropic PBC and Meta Platforms Inc., but questions remain about how much revenue will be recognised in each quarter, as opposed to being accounted for in a multiyear backlog.

The price of using AI and the ‘rate of return’ debate

In the coming months, some of the world’s biggest AI labs — including OpenAI and Anthropic PBC — will debut on the public markets at valuations close to $1 trillion each. Alphabet Inc. is tapping equity and debt markets to fund its AI spending, while older companies like Hewlett Packard Enterprise Co., Dell Technologies Inc. and Nokia Oyj are benefiting from the gold rush too.

Everyone is piling in on the bet that artificial intelligence will make companies more profitable and productive. But the truth is messier.

The debate about AI’s return on investment stubbornly persists, in part because companies still lack broad, measurable improvements they can cite, with spending justified company-by-company. NVIDIA Corp. Chief Executive Officer Jensen Huang this week promised “insane” returns for investors in AI (calling those who questioned the technology’s potential returns “crazy”), but the next few months of initial public offerings could prove a peak rather than the start of another boom.

One set of cautionary signals comes from companies that find AI useful but far too costly. Uber Technologies Inc. recently set usage caps on AI coding tools for its staff after the company blew through its entire annual AI budget in just a few months. Walmart Inc. capped staff use of a tool for generating spreadsheets and presentations, shifting away from giving employees an unlimited number of tokens, a data measurement for usage. One unnamed company is said to have accidentally spent $500 million on tokens in a single month, after introducing Anthropic’s Claude to its workforce but failing to provide usage limits. Plenty of grumbling about cost is coming from the financial sector too.

Last year, the hot new trend among corporate users was tokenmaxxing, or using AI as much as possible to boost productivity and climb internal leaderboards. But more firms are now learning the hard way that the more tokens they spend, the more AI costs.

The consultancy Bain & Company summed the problem up in a recent report titled Your AI Budget Is Growing. Your Returns Aren’t. It found that while some companies reported cost reductions of 10% to 20% after using AI, many were ploughing more money into the technology before those savings had fully materialised, essentially making a leap of faith.

The bull case is that we’re still in an experimentation phase in which many companies aren’t measuring all the right things. AI’s biggest value could come not just from cutting costs but from producing more useful work.

Many companies currently lack the skills to integrate AI properly. OpenAI and Anthropic have recognised that gap and are hiring more forward-deployed engineers, or software designers who also work with customers to help use AI in the most effective way.

But many other firms are finding that AI is increasingly like a never-ending utility bill. Every query, hallucinated draft or bloated coding session has a cost because it is essentially metered software.

That’s partly the result of the sheer scale at which companies are consuming AI. Providers have always charged corporate customers by usage, but until recently, most employees accessed AI through flat-rate subscriptions or price-capped pilots, so token costs stayed under the radar. Now that firms are deploying agents and coding tools and rolling out AI company-wide, those per-query expenses are finally becoming large enough to bite. Now that those costs are out in the open, metered pricing is forcing companies to confront a question that AI labs conveniently postponed as they built up more hype: whether their technology is useful enough to justify the bill. If many more AI users start to go the way of Uber and Walmart, that will be a problem for a market that until now has been riding astonishingly high.

Still worried about AI job losses?

Fear of a “jobpocalypse” driven by artificial intelligence is pervasive; just ask any graduating student. Virtually every report on the labour market is now scrutinised for signs of job displacement. But even though we’re now halfway through the fourth year since the launch of ChatGPT marked the unofficial beginning of the generative AI era, a meltdown in employment isn’t showing up in the official data.

It could just be a matter of time.

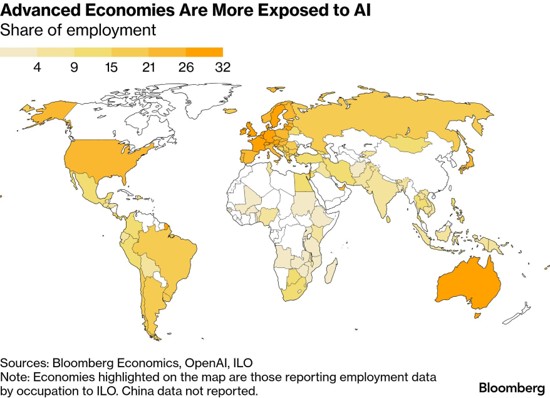

There is the suggestion that that 27% of workers in advanced economies, or more than 120 million in over 30 countries, are likely to be meaningfully affected by AI (just an observation below – what about Canada, Trump’s “51st State?”):

Reports of layoffs, particularly in the tech space, appear to reinforce the job-displacement hypothesis. AI-driven disruption drove an estimated about 55,000 planned layoffs in 2025, representing approximately 5% of total job cuts last year. It ranked fifth among all cited reasons.

But this is inconclusive. Anecdotal evidence cited as proof of disruption is, after scrutiny, often dismissed as possible AI-washing. And for all the anxiety surrounding artificial intelligence, broad labour measures show no meaningful signs of displacement. If anything continues to paint a picture of a remarkably healthy jobs market. Tuesday’s print shows vacancies surging back to their highest pre-pandemic level. That doesn’t support any notion of an AI takeover.

Even accounting for population growth since the turn of the century, the latest data show the US once again has more than one vacancy for each unemployed worker. Whatever the threats from AI and the discontent of graduating students, the labour market remains firmly tilted in favour of job seekers.

For all this resilience, however, it’s far too early to rule out meaningful displacement. Previous industrial revolutions took decades before their full employment impact was felt. That lag between technological innovation and an eventual hit to jobs has shortened, with each successive upheaval accelerating the pace at which certain occupations are transformed or rendered obsolete, but there’s still a lag.

Roles like software engineering have been transformed by agentic AI systems that can perform many entry-level roles with little to no supervision. But such changes are likely concentrated in specific sectors and unlikely to shift the overall aggregate.

Humanoids and robotics remain far from their full potential, and it is unclear whether they will ultimately complement or compete with human workers.

Throughout history, human ingenuity tends to prevail; the technological forces that render some jobs obsolete often give rise to new occupations that were previously inconceivable.

Creative Destruction:

Schumpeter’s notion of creative destruction argues that while every generation believes it is living through exceptional change, humans repeatedly adapt.

Joseph Schumpeter, the Austrian-American economist, introduced this concept in his 1942 book Capitalism, Socialism and Democracy. The core idea is that capitalism advances not through stability, but through constant cycles of destruction and renewal — old industries, technologies, and business models are continuously torn down and replaced by new, more efficient ones.

Innovation is the engine. Entrepreneurs introduce new products, processes, or technologies that render existing ones obsolete. The old is not merely outcompeted — it is destroyed. Think of how:

• The car killed the horse-and-buggy industry

• Digital streaming dismantled physical video rental

• The smartphone wiped out dedicated camera and GPS device markets

Why “Creative”?

The destruction is productive. Resources, capital, labour and talent are freed from dying industries and redeployed into newer, more productive ones. The economy as a whole grows richer and more dynamic, even as specific industries or workers suffer painful disruption.

He argued this process is the defining feature of capitalism, not a bug or side effect. Attempts to protect incumbents from disruption — through regulation, monopoly, or government intervention — ultimately slow economic progress by keeping resources trapped in less productive uses.

The concept powerfully describes today’s tech economy. AI, for instance, is currently “destroying” roles in legal research, coding, and content creation while simultaneously creating entirely new industries and job categories. Micron’s rise, as discussed above, is itself a product of creative destruction.

AI rendered older computing architectures obsolete and created enormous new demand for high-bandwidth memory.

The tension Schumpeter identified — between the short-term pain of disruption and the long-term gains of innovation — remains one of the central challenges of modern economic policy.

obs like lamplighters, ostlers, livery-stable keepers, newspaper criers and boiler firemen once dominated.

In 1910, one-third of workers were employed on farms, and by the end of the century, that proportion was minuscule. In 1950, one-fifth comprised machine or vehicle operatives; by the end of the century, the proportion was less than a 10th. In 1970, over 5% of the workforce were stenographers, typists or secretaries; yet these jobs are almost nonexistent today.

Green shoots of the job market’s next evolution are emerging. Revelio Labs, a work intelligence platform, shows that the need for core data-centre jobs has grown sharply since the launch of ChatGPT, with demand for the construction workers who build them (a segment that will presumably decline again once the infrastructure has been completed) rising by over 430%.

Wall Street’s greatest powers are lined up behind the notion that AI will displace a huge number of jobs — but also, conveniently, create new posts to replace all of them. Goldman Sachs researchers estimate that AI could automate 25% of current work hours over the next decade, with white-collar occupations facing the greatest exposure. This will be offset by new jobs that the technology will enable. Just a thought – maybe everyone will just get a shorter work week?

Do any of us feel like we have less to do these days, despite the convenience of Excel, email or Zoom? Probably not. It’s possible that AI will have to wait for a recession before employers feel determined to use it to eliminate jobs, human ingenuity will probably use the new technology to create new roles. The jobpocalypse certainly hasn’t started yet.

Elon Musk’s SpaceX needed comparatively little money to build a world-beating space launch and satellite-broadband firm. But as it reframes itself partly as an artificial-intelligence infrastructure company, offering both terrestrial and potentially space-based computing capacity, its financial needs are massively increasing. This doesn’t bode well for a mooted $1.8 trillion valuation in its initial public offering.

Before its AI pivot, SpaceX raised more than $9 billion of venture capital to fund its Falcon rockets and Starlink satellite constellation. That’s a lot for a private startup, even one founded almost a quarter century ago. But it’s a sliver of the sums that AI specialists OpenAI and Anthropic PBC have tapped investors for recently.

Space Rockets Are Capital Intensive. AI Is Even More So

The old SpaceX was able to use its capital so efficiently because of its reusable rocket innovations, cheaper in-house components, lucrative government contracts and profitable broadband internet services. But the company’s hunger for funds has deepened since its February merger with another Musk outfit, the loss-making startup xAI. The development costs for Starship, SpaceX’s heavy-lift launch vehicle, are only adding to the pressure. In effect this loss-making division is being bundled up with the way sexier SpaceX, but nobody buying into the hype seems to mind.

While SpaceX held almost $24 billion of cash and short-term marketable securities at the end of March, on current form, even tens of billions of dollars of IPO proceeds wouldn’t last long.

As a standalone company, SpaceX was in many respects a magnificent business But after incorporating xAI, it’s not the same company anymore. The pace of spending is concerning. Founded in 2023, xAI has already raised more than $40 billion to try to compete with OpenAI and Anthropic.

xAI’s Grok chatbot is struggling to keep up with Sam Altman and Dario Amodei’s creations. SpaceX has had more luck renting out spare data-centre capacity. Anthropic has agreed to pay it $1.25 billion a month for computing power.

This means SpaceX has become both an AI laboratory and a cloud provider like CoreWeave Inc., with the added twist that it may one day operate data centres in space. While Musk’s engineers have often proved doubters wrong, it’s unclear how orbital data centres would be repaired or upgraded.

These ambitions will be astonishingly expensive, and Musk isn’t stopping there: SpaceX also wants to build its own chipmaking plant, reducing its reliance on industry leaders Taiwan Semiconductor Manufacturing Co. and Samsung Electronics Co. While another of his companies, Tesla Inc., will help fund that extraordinarily complex endeavour, it may end up costing more than $100 billion. And SpaceX is already burning through prodigious amounts of cash, while its debts have swelled to about $29 billion.

On a consolidated basis, the company’s capital spending totalled more than $20 billion in 2025, with most of that coming from the AI division. That’s more than the entire business’s $18.7 billion of revenue that year. During the first quarter of 2026, capex increased to more than $10 billion, double the group’s revenue in the same period.

Capital expenditures were twice as high as revenues in Q1 2026

The IPO prospectus warns that capex will increase “substantially” in future, which SpaceX will fund using a “range of debt and equity financing solutions” available to it as a public company. It aims to maintain an investment-grade credit rating. Anyone buying SpaceX shares at a $1.8 trillion valuation, more than 90 times last year’s revenue, is betting that traditional metrics like cash flow and profit don’t apply here. That’s often been the case for Tesla, where a golden dawn is always just over the horizon. SpaceX’s massive capital needs will put such sunlit assumptions to the test.

Author: Dawn Ridler

Last week, Google announced an $ 80 billion capital raise in the form of an equity offering. There will be a $ 30 billion public offering split into preference shares and Common class shares. Then there will be a $ 40 billion at the market offer which will begin in Q3 2026. So all of this will raise $ 70 billion, and then in addition to this, there is an extra $ 10 billion which will be raised by selling stock to Berkshire Hathaway. The proceeds of this capital raise will go towards what they call general corporate purposes and capital expenditure as it relates to AI. They also note that some of the proceeds will help them meet administrative obligations as they relate to a restatement of their share incentive scheme.

Debt has always been modest in this company when compared to its cash resources. There was an uptick in debt as they issued bonds in 2025 (circa $ 20 billion) and 2026 ($30 billion), but again, much of this is modest in comparison to the cash resources available to them from their traditional search and advertising business. What makes this interesting is that they preferred to issue stock, and by default, are asking shareholders to fund their expansion rather than continuing to tap global bond markets for the funding.

Diluting current shareholders should be the last place one goes to raise new capital, but perhaps given that bond yields have been rising, management figured it would be cheaper to fund expansion through the issuance of shares than the debt markets. And then there is a frothy market into which to do this. A modest growing company with a share price to match is not going to have a shareholder base which will be in favour of dilution in any shape or form. But then this is the AI boom. New stock being issued at 28x earnings should make any new shareholder pay attention to the value they are getting. I am sure some may be forfeiting their thought process, given that Berkshire Hathaway is also participating. Could they know something no one else does? Or perhaps they are just so cash-heavy at present that they don’t need to make the investment case work in the short term. They will settle for the mid to long term.

In my mind, the equity capital raise is the next step in a market that is slowly becoming more frothy.

Google is a great business, but management tapping shareholders should never be done lightly. All of this cash, raised across large tech companies, is going to have to generate superior returns. Add to this the IPO market, which is only just getting started. SpaceX will launch soon, and both Anthropic and OpenAI will possibly look for a deal as well. The frenzy is starting, and the risk appetite is there to fund it. As with all new technologies, history teaches that a major build-out occurs, sucking in large amounts of capital, and that no one can afford to miss out on the next wave of excitement. At some point, it peters out, leaving vast amounts of capacity without the requisite demand. History shows that demand does arrive at some point, but by then the initial players have either exited or been bought by incumbents with cash piles intact. These become the real winners over time. How this frenzy plays out only time will tell but for now capital markets are pointing to the next step in this journey.

Author: Cobie Le Grange

EXCHANGE RATES and other Indices:

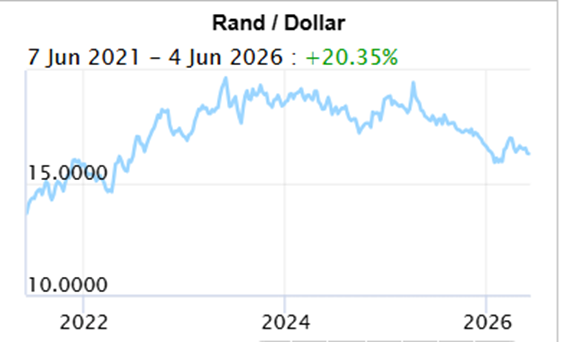

The Rand/Dollar closed at R16.55 (R16.23, R16.46, R16.68, R16.39, R16.63, R16.29, R16.41, R17.07, R17.06, R16.89, R16.55, R15.93, R16.01, R15.96, R16,03, R16.15, R16.10, R16.50, …R16.91, R17.13, R17.36, R17.13,16.52 )

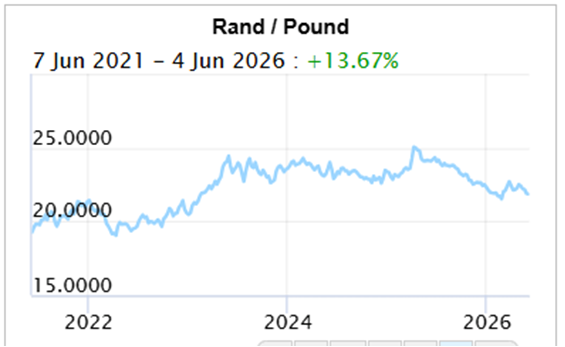

The Rand/Pound closed at R22.06 (R21.80, R22.09, R22.21, R22.30, R22.56, R22.35, R22.02, R22.09, R22.77, R22.76, R22.35, R22.20, R21.48, R21.59, R21.78, R21,82, R22.11, R21.97, R22.13, …R22.57, R22.68, R22.74, R22.56,

The Rand/Euro closed the week at R19.08 (R18.91, R19.11, R19.38, R19.29, R19.48, R19.37, R19.17, R19.24, R19.70, R19.77, R19.33, R19.23, R18.80, R18.87, R18.94, R18.93, R19.14, R19.04, R19.20)

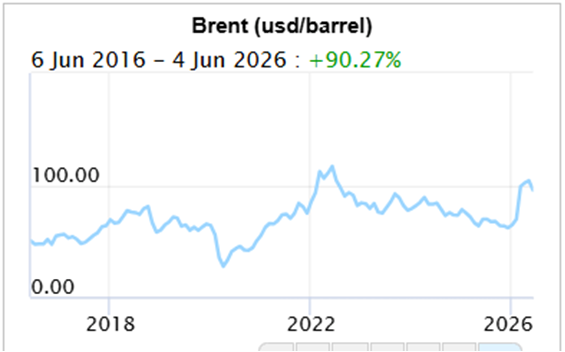

Brent Crude: Closed the week $93.09 ($91.12, $104,24, $109.26, $101.29, $108.83, $105.33, $90.38, $95.20, $107.88, $112.36, $103.14, $92.88, $73.19, $71.76, $67.75, $68,05, $69.32, $65.88, $63.34, …$63.71, $63.19, )

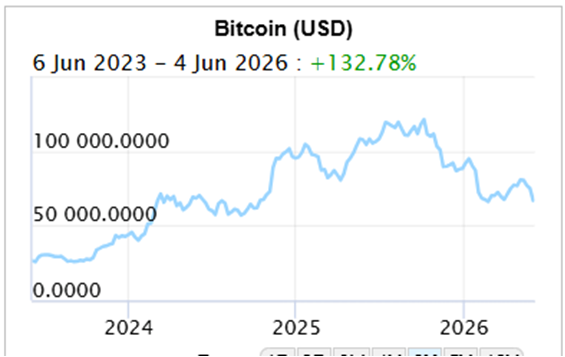

Bitcoin closed at $60,762 ($73,788, $74,559, $77,879, $80,733, $78,204, $78,049.98, $75,519, $70,904, $68,691 , $68,586, $70,869, $67,310, $63,534, $68,04, $69,649, $68,553, $81,301, $89,295, $90,585,)

Articles and Blogs:

Legacy Series Part 4 NEW

Legacy Series part 3

Legacy Series Part 2

Legacy Series Part 1

Holiday checklist

Next year – Action Plan

Next year – Vision, Mission etc

Medical Risk Mitigation

Next Year – Consolidation

Abdication or diversification?

Carbo-loading your retirement Spoiled for choice

Who needs a plan anyway

8 questions you need to ask about retirement

What to do when interest rates drop

How to survive volatility in your investments

What to do when interest rates drop

Difficult Financial Conversations

Financial Implications of Longevity

Kick Start Your Own Retirement Plan

You matter more than your kids in retirement

To catch a falling knife

Income at retirement

2025 Budget

Apportioning blame for your financial state

Tempering fear and greed

New Year’s resolutions over? Try a Wealth Bingo Card instead.

Wills and Estate Planning (comprehensive 3 in one post)

Pre-retirement – The make-or-break moments

Some unconventional thoughts on wealth and risk management

Wealth creation is a balancing act over time

Wealth traps waiting for unsuspecting entrepreneurs

Two Pot pension system demystified

Cobie Legrange and Dawn Ridler,

Rexsolom Invest, Licensed FSP 45521.

Email: cobie@rexsolom.co.za, dawn@rexsolom.co.za

Website: rexsolom.co.za, wealthecology.co.za