UK inflation – a pleasant surprise: The Bank of England held Bank Rate at 3.75% on 18 June in an 8-1 vote, as UK inflation eased to 2.8% in May. Hike expectations have fallen from four this year to roughly one, following the US-Iran deal. Politically, over 70 Labour MPs are calling for Starmer to resign, and Andy Burnham’s Makerfield byelection win positions him as a likely successor, though markets expect policy continuity either way.

RSA Inflation: South African inflation jumped to 4.5% in May, driven by fuel costs (up 28.7% year on year). The SARB had already hiked the repo rate 25bps to 7% on 28 May on a narrow 4-2 vote, its first hike since 2023. A further hike is now pencilled in for 2026, with inflation forecast raised to 4.4% and growth cut to 1.2%. Rate cuts are off the table

The latest Iran deal: Trump signed the US-Iran memorandum at Versailles, with Pezeshkian countersigning in Tehran, opening a 60-day negotiating window. Trump conceded ground on his own past red lines: uranium enrichment, ballistic missiles, and frozen funds. The reaction was split, with Iran hawks critical and some typical critics welcoming it. The deal is explicitly preliminary, and given Trump’s history of reversals, it’s too soon to call it durable.

Warsh in the hotseat: Warsh held rates steady at his first FOMC meeting, a split decision between hold and hike camps, and notably submitted no dot of his own. He wants to reduce market reliance on Fed signalling and move away from the “Fed put,” though the piece is sceptical that this holds once a real bear market tests it. He’s also floated AI-driven job creation offsetting inflation, a view treated as premature.

UK inflation – a pleasant surprise

With the 10th anniversary of the Brexit vote coming next week, it was a ‘super Thursday for UK policy…

The Bank of England Monetary Policy Committee held Bank Rate at 3.75% on June 18, according to a decision announced Thursday at noon UK time. The hold was widely expected and came on an 8-1 vote, continuing the committee’s cautious stance in the face of conflicting inflation and growth signals. UK inflation stood at 2.8% in May, above the 2% target but easing from earlier peaks driven by the Middle East energy shock.

Senior officials, including Governor Andrew Bailey and Deputy Governor Sarah Breeden, had signalled the need to tread carefully before tightening further, citing uncertainty over whether recent energy price declines will persist and whether second-round wage and price effects have already taken hold. Markets had earlier priced as many as four hikes this year at the height of geopolitical uncertainty in March, but by mid-June that expectation had retreated to roughly one hike over the next 12 months, reflecting the easing from the US-Iran peace deal.

Meanwhile, about 200 miles to the north, the voters in the Makerfield byelection decided that Greater Manchester’s mayor, Andy Burnham, should be given the parliamentary seat so he can serve if he is to challenge Keir Starmer for the prime ministership. The Reform protest vote took a back seat, but never count Trump-Lite-Farage down and out; he has more lives than a mangy alley cat. The ultra-right-wing winds are still blowing in the ‘West’ (technically North West).

The latest UK inflation numbers came in below expectations. The core consumer price index is now actually below its US equivalent, even though the UK is more dependent on energy imports.

At the last meeting of the MPC, the chief economist Huw Pill voted to raise rates. Until a few days ago, the general expectation was that at least one more would join him. But the mild inflation added to the news from Strait of Hormuz to bring the projected Bank Rate crushing down. At the last MPC, the market was braced for three hikes this year. That’s now down to one.

That is in large part because UK rates are viewed as wholly dependent on the price of oil (not really much different to us here in RSA). This is an odd judgment given the widespread arguments that the BoE and other central banks shouldn’t be too hasty to react to a potentially transitory oil shock. But as Mizuho Group’s Jordan Rochester points out, the projected interest rate for the end of next year has been trading almost perfectly in line with oil price fluctuations.

If the MPC is unlikely to produce a shock now, the unlikely figure of Elon Musk is also made the Makerfield byelection more predictable. The sitting MP, Josh Simon, precipitated the contest by resigning last month, saying that he was doing so to allow Burnham a path to parliament and the prime ministership. As Nigel Farage’s populist-right Reform Party had just bested Labour in local elections in the constituency, all seemed set fair for an epic contest. It didn’t pan out that way at all; the Reform Party was thoroughly trounced.

But Musk obviously tried to split the anti-Burnham vote by vocally supporting Restore Britain, a splinter group from Reform UK. Burnham won with some ease, and prediction markets now give him a 70% chance of swiftly winning the premiership:

How much damage would this do to UK assets? Starmer has said he will contest any challenge, meaning that the next few months could be taken up with a leadership contest, creating uncertainty. And Burnham at this point appears to be outflanking Starmer from the left. An early Burnham campaign gaffe that the UK should not be “in hock to the bond markets,” along with his interest in nationalising some utilities, pays directly into such a narrative. (Starmer also infamously misspoke at a Labour party conference address in his first months as prime minister, saying there could be no peace in Gaza without “the return of the sausages” when he meant to say “hostages.” He caught and corrected himself, but the moment perhaps lingered in public memory as emblematic of his leadership struggles, but compared to the full-cream constant Trump gaffes, blunders, mistakes, errors, faux pas, flubs, bloopers, clangers and howlers out of the White House, that is very small potatoes.

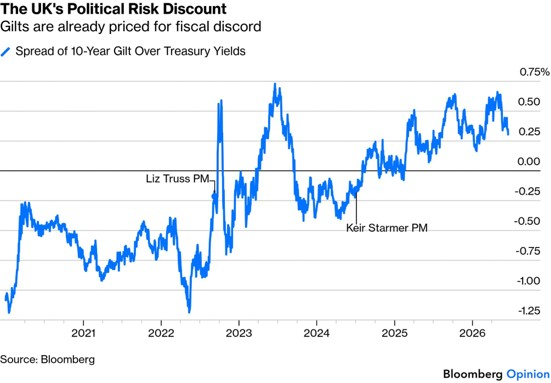

But it’s questionable how much of an impact a Prime Minister Burnham would have. As prediction markets show, he is already thought likely to have the job by the end of this year, and it hasn’t provoked great alarm. Britain’s fiscal position would make it difficult to make significant changes, and the terrible disciplining example of former Prime Minister Liz Truss, brought down by the gilt market within 49 days, will make any UK politician reluctant to tread too far.

The bond market already prices in fiscal risks, as gilts trade at a higher yield than Treasuries, and has signalled elevated risk ever since Starmer’s victory two years ago — but it’s fair to assume that it has the most alarming political outcomes covered:

The likelihood is that the UK limps on with much the same policies it currently has, whether under Starmer or under a slightly more talented politician, while the Bank of England keeps rates where they are. It’s not an inspiring prospect, but markets appear to be priced for it.

South Africa’s inflation accelerated sharply to 4.5% in May, and the SARB has already responded. The inflation surge was largely driven by increases in fuel prices, with the fuel index leaping by 14.3% on a monthly basis to reach an annual rise of 28.7%. Over the past 12 months, prices for petrol increased by 24.8% and diesel by 53.8%.

The South African Reserve Bank raised its key repo rate by 25 basis points to 7% on May 28, 2026, marking its first rate hike since 2023. Four of the six members of the MPC backed the decision, while two voted to hold. The narrow vote reflects genuine tension within the committee between containing inflation and protecting fragile growth.

The policy shift is dramatic. The committee said inflation risks had increased due to the Middle East crisis and warned that overlapping shocks could trigger second-round effects, justifying a monetary policy response to contain risks and bring inflation back to target.

Looking ahead, the SARB’s Quarterly Projection Model now suggests another rate increase in 2026 following the 25-basis point increase on May 28. Inflation forecasts were raised to 4.4% for 2026 (from 3.7%) and the central bank lowered its growth forecasts for 2026 to 1.2% (vs 1.4%).

For borrowers, the prime rate is now 10.50%. For investors, the calculus has shifted entirely: rate cuts are off the table, and the growth outlook has deteriorated. The structural stickiness of energy and utility costs means this isn’t a temporary blip that monetary tightening will quickly cure. The SARB is fighting a supply-side shock with a demand-side tool, which explains the committee’s internal disagreement. It is way too early to tell if this new Versailles ‘MOU’ will actually stick and bring down the price of fuel.

Hopefully, this article isn’t going to age like spilt milk and be totally irrelevant by Monday, but here goes… President Donald Trump and his team had several red lines that they used to justify the US war against Iran. At a press conference on Wednesday, Trump largely brushed them aside.

Explaining his decision to agree to an interim peace deal, Trump repeated his insistence that the country would never get a nuclear weapon. Yet he went on to suggest that Iran should have the right to enrich uranium, be allowed to develop ballistic missiles and get access to billions of dollars in frozen funds.

Those three things have been at the centre of the debate around how to approach Iran for years, dating to the 2015 agreement that the US, under President Barack Obama, and other great powers signed with Iran to limit its nuclear program.

Not only that: Trump had repeatedly cited those issues as reasons why Obama and past presidents had failed so badly in containing the threat posed by the regime in Tehran.

In a head-spinning turn of events, Iran hawks including former Vice President Mike Pence and former US Ambassador to the United Nations Nikki Haley lamented Trump’s new vision, while some of the president’s most vehement critics cheered.

“It’s doing a lot of the things that Trump criticised Obama for doing,” Christian Whiton, a State Department adviser in the George W. Bush and first Trump administrations, said of the president’s comments. “And whether or not he means it, he has expressed to them he will not resume military operations because doing so will cause the worst recession since the great depression.”

The National Iranian American Council, meanwhile, cheered what it saw from Trump.“The measures in this agreement should not be read as concessions but rather corrections to a decades-old policy of coercion that was an abject failure and made war inevitable,” the group said in a statement.

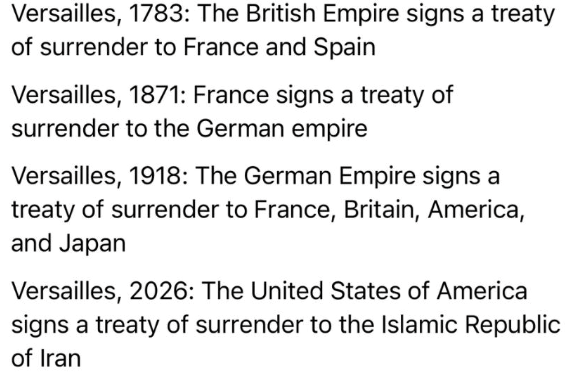

Hours later, at the palace of Versailles near Paris, the president signed the so-called memorandum of understanding to end the war and reopen the Strait of Hormuz. The location chosen to sign the accord is “interesting”:

Trump has a history of taking a hard stance only to reverse it days, sometimes even hours later. And Iran hawks may not need to worry too much: The interim deal opens the door for 60 days of negotiations and Trump hasn’t given anything away yet.

The Trump administration has also said Iran has been so weakened economically and militarily that the US has achieved its goal of threat reduction and even opened the door to the country rejoining the global economy, if its leaders choose that path.

But there was plenty in the press conference that surprised even the president’s supporters.

Take Iran’s ballistic missile program. Days after the US and Israel launched the war with Iran in late February, Defense Secretary Pete Hegseth said the US objective was to “destroy the missile threat” posed by Iran. Trump shrugged off that idea at the press conference marking the end of a Group of Seven summit in Evian, France. He even derided those offering him advice — he referred to them as “guys I like” — as focusing on the wrong thing with the fixation on ballistic missiles. “I mean, they have to have some because other people have some,” Trump said.

“Missiles aren’t the problem,” Trump told reporters. “They hurt a little location, but they don’t blow up the planet.”

The president took the same approach with nuclear enrichment. For years, he and many Republican critics of Iran have questioned why it should be allowed to enrich uranium if, as it insists, it doesn’t want a nuclear weapon. Secretary of State Marco Rubio told Fox News in May that Iran needs to “walk away from enrichment.”

With Rubio standing right behind him on Wednesday, Trump made clear he no longer agreed.

“It’s a little hard when other people have it, other adjoining states have it, and you’re not letting them have it for purposes of electricity and things like that,” Trump said. “You have to use a little common sense.”

The third red line Trump crossed centred on Iran’s frozen assets.

The country has billions of dollars in overseas accounts that the US has blocked banks from releasing. Part of the justification for years has been that Iran is a leading state sponsor of terrorism, funding proxy groups such as Hezbollah in Lebanon and Hamas in Gaza, and can’t be trusted not to do so again.

“It’s not our money, it’s their money — and we froze it at a certain point in time,” Trump said. “I guess we’re going to have to give it back, you know. If we didn’t give it back, nobody would ever invest in the dollar again.” That idea met with strong opposition from some of the president’s most ardent supporters, including Senator Ted Cruz, a Texas Republican.

“History teaches us giving billions of dollars to theocratic lunatics who want to murder us is not a good idea,” Cruz said in an interview. There have been some pundits citing Obama’s payment to Iran as a precedent for this. There is one big difference. The funds released to Iran by the Obama administration were in settlement of a dispute from the 70’s, where Iran, run by the Shah, had bought arms, but before they could be delivered, his regime was overthrown, and the US kept the money and the arms. A classic double dip. This is not quite the same, and Trump is already walking that part back.

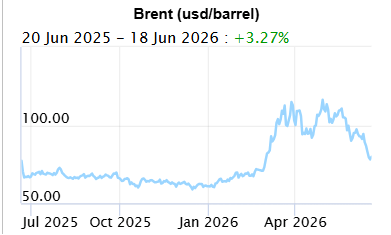

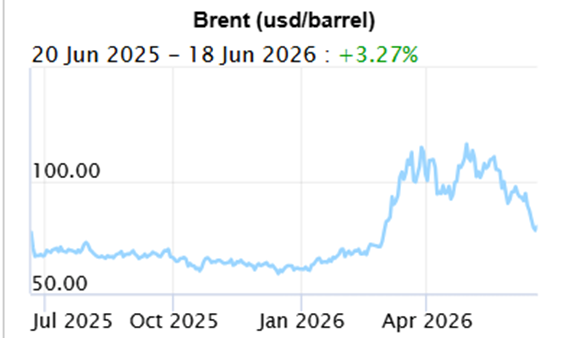

In short, it is far too soon to celebrate; let the market day-traders speculate, but watch from the sidelines with a jaundiced eye. As of Friday afternoon, this is what Brent Crude looked like:

Author: Dawn Ridler

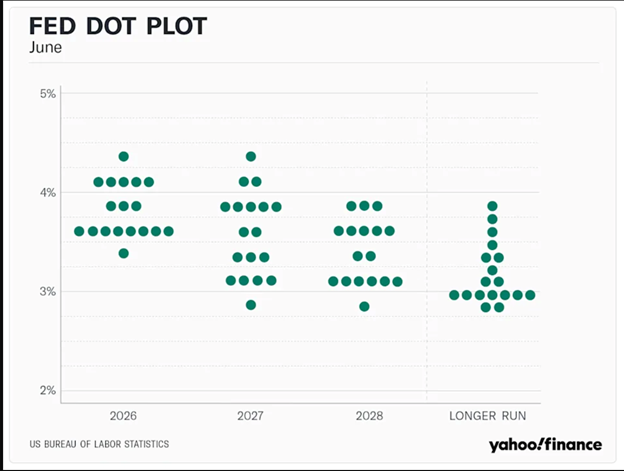

Last week, Kevin Warsh got his first opportunity to lead the Federal Open Market Committee (FOMC) and announced that US rates will not move this time around. This wasn’t a surprise. The committee was actually split between those that wanted to hike rates (dots above the 3.75% line below) and those that wanted to keep them steady (as denoted by the dots on the horizontal line). There was one member who believed that rates should be cut. Not sure how they would come to that conclusion! There is clearly now an impetus on raising rates as inflation is rising but much to Governor Warsh’s relief, the Iranian deal will at least not place inflation on an upward trajectory which can become harmful to the US economy. Interestingly, the Governor doesn’t believe in forecasts and thus refrained from participating in the dotplot which is a mainstay feature of US rate decisions.

But what was evident from the meeting is that he wants to see a step change at the Federal Reserve. Rather than watching data with market participants in order to gauge the economy, the Governor believes that market participants have become overtly reliant on what the FED says and does to judge market movements. This is something he wants to change, but can he?

The biggest reason for this reliance stems from the liquidity injections which has become the norm since the 2008 financial crisis. Investors have realised that this drives stock prices higher and if a fresh dose of liquidity is required to calm markets, the FED will readily administer this. This is called the “FED Put” in markets and perhaps wont be so prevalent in the future. The problem is that markets without a “FED Put” becomes part of the old-world bull/bear cycles. Can the baby boomer generation, with their overt reliance on stock markets for retirement, stomach a 1-year bear market? What does a bear market in stocks do to the credit cycle and by default the ability for the US government to refinance their ballooning debt. The Governor may be forced into providing liquidity before his term is out. So, whilst he awaits this, he wants to focus on price stability. I think most central banks would want to see this but the tools to achieve this may be changing. The Governor believes there is a brave new AI world out there which can deliver on fuller employment even if inflation is persistent. Economists will tell you that inflation ultimately kills jobs but this Governor believes that AI could influence all of this. There is this notion that AI will create new industries and by default jobs. If the byproduct is more inflation then this shouldn’t stand in the way of job creation. But perhaps the Governor is getting a little ahead of himself. History teaches that where new capacity is brought online in an industry, it often isn’t matched with the same level of demand. The use of the capacity takes time and whilst this occurs, the most leveraged players go out of business. This may very well happen before AI creates new industries and jobs.

What one can rely on is that there are events beyond the control of the Governor which will require immediate action. He may find that he has to deal with the same issues as his predecessors because the structure of the economy requires it. For now, perhaps idealistically, he wants to run the FED to his own beat. How long this lasts, the next crisis will dictate.

Author: Cobie Le Grange

EXCHANGE RATES and other Indices:

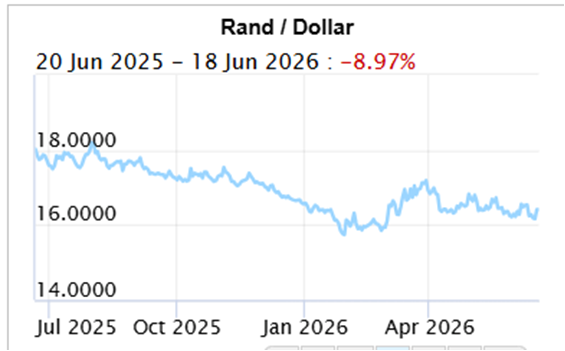

The Rand/Dollar closed at R16.39 ( R16.27, R16.55, R16.23, R16.46, R16.68, R16.39, R16.63, R16.29, R16.41, R17.07, R17.06, R16.89, R16.55, R15.93, R16.01, R15.96, R16,03, R16.15, R16.10, R16.50, …R16.91, R17.13, R17.36, R17.13,16.52

The Rand/Pound closed at R21.67 (R21.80, R22.06, R21.80, R22.09, R22.21, R22.30, R22.56, R22.35, R22.02, R22.09, R22.77, R22.76, R22.35, R22.20, R21.48, R21.59, R21.78, R21,82, R22.11, R21.97, R22.13, …R22.57, R22.68, R22.74, R22.56,

The Rand/Euro closed the week at R18.89 (R19.16, R19.08, R18.91, R19.11, R19.38, R19.29, R19.48, R19.37, R19.17, R19.24, R19.70, R19.77, R19.33, R19.23, R18.80, R18.87, R18.94, R18.93, R19.14, R19.04, R19.20)

Brent Crude: Closed the week $80.59 ($87.33, $93.09, $91.12, $104,24, $109.26, $101.29, $108.83, $105.33, $90.38, $95.20, $107.88, $112.36, $103.14, $92.88, $73.19, $71.76, $67.75, $68,05, $69.32, $65.88, $63.34, …$63.71, $63.19, )

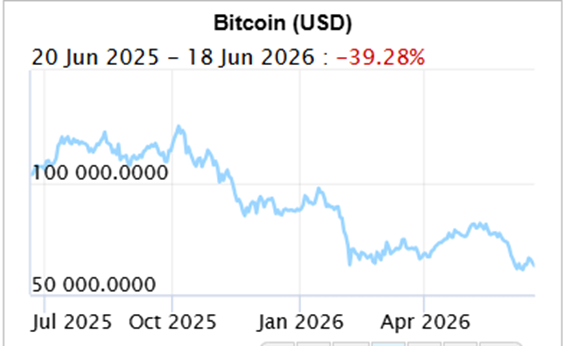

Bitcoin closed at $64,029 ($64,131,$60,762, $73,788, $74,559, $77,879, $80,733, $78,204, $78,049.98, $75,519, $70,904, $68,691 , $68,586, $70,869, $67,310, $63,534, $68,04, $69,649, $68,553, $81,301, $89,295, $90,585,)

Articles and Blogs:

Legacy Series Part 4 NEW

Legacy Series part 3

Legacy Series Part 2

Legacy Series Part 1

Holiday checklist

Next year – Action Plan

Next year – Vision, Mission etc

Medical Risk Mitigation

Next Year – Consolidation

Abdication or diversification?

Carbo-loading your retirement Spoiled for choice

Who needs a plan anyway

8 questions you need to ask about retirement

What to do when interest rates drop

How to survive volatility in your investments

What to do when interest rates drop

Difficult Financial Conversations

Financial Implications of Longevity

Kick Start Your Own Retirement Plan

You matter more than your kids in retirement

To catch a falling knife

Income at retirement

2025 Budget

Apportioning blame for your financial state

Tempering fear and greed

New Year’s resolutions over? Try a Wealth Bingo Card instead.

Wills and Estate Planning (comprehensive 3 in one post)

Pre-retirement – The make-or-break moments

Some unconventional thoughts on wealth and risk management

Wealth creation is a balancing act over time

Wealth traps waiting for unsuspecting entrepreneurs

Two Pot pension system demystified

Cobie Legrange and Dawn Ridler,

Rexsolom Invest, Licensed FSP 45521.

Email: cobie@rexsolom.co.za, dawn@rexsolom.co.za

Website: rexsolom.co.za, wealthecology.co.za