I spent another interesting week interviewing on Fine Music radio last week, and had some interesting conversations. This one, on construction changes underway around RSA was particularly informative: Another Brick in the Wall

Too Busy? Got Better Things to Do? Read the Summary…

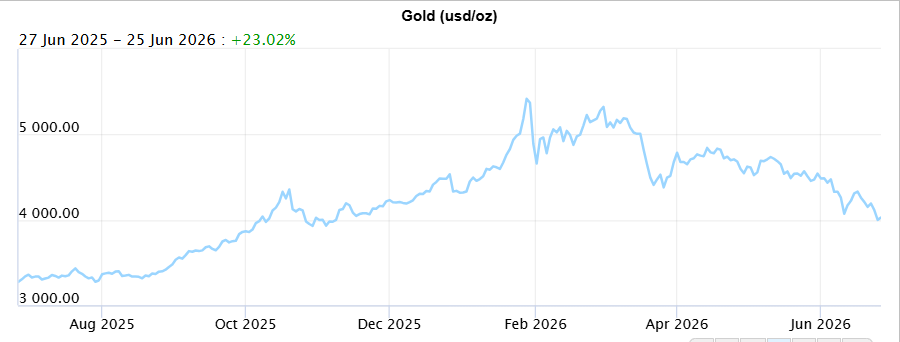

About change!: Gold has shed all its 2026 gains and is now down roughly 8%, falling below $4,000 for the first time in eight months. The reversal reflects the unwinding of the debasement trade, the long-running bet that government deficits and money-printing would erode fiat currencies, as Kevin Warsh’s hawkish Fed stance and the US-Iran ceasefire have strengthened the dollar to 14-month highs and dampened inflation fears, even as PCE inflation hit a three-year high of 4.1% in May.

AI, all honeymoons have to end, now it’s the hard graft: AI has moved from sci-fi to mainstream, but real workplace adoption remains narrow, essentially productivity admin at scale. Hyperscalers face mounting pressure to justify enormous valuations with corporate revenue that isn’t yet materialising at the pace required, and the elusive “killer app” remains exactly that.

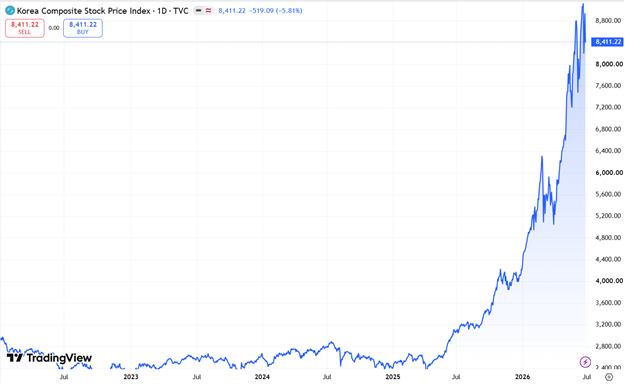

The Kospi’s meltdown, a snapshot for posterity: South Korea’s KOSPI plunged 9.99% on June 23, “Black Tuesday” , triggering circuit breakers and $2.5 billion in foreign outflows, driven by MSCI’s fourth consecutive rejection of South Korea for Developed Market status, a hawkish Fed, and leveraged ETF concerns around Samsung and SK Hynix. The market bounced sharply the next day on Samsung buyback speculation, but the structural MSCI exclusion locks out billions in passive inflows until at least 2028.

Japan, growing at last: Japan is undergoing its biggest fiscal overhaul since World War II, with Prime Minister Takaichi introducing a multi-year budgeting framework to fund a proposed ¥370 trillion investment plan targeting AI, semiconductors, and economic security. The shift reflects a sober reassessment of Japan’s strategic position, particularly its defence posture relative to China.

Stay safe: The anti-immigration movement “March March,” founded by Jacinta Ngobese-Zuma and linked to the MK Party, has set a June 30 deadline for undocumented migrants to self-deport. Violence has already claimed lives and displaced thousands, and the ANC has accused Zuma of engineering the unrest ahead of November’s local elections. President Ramaphosa has deployed a R600-million security operation, but the government’s credibility is under pressure. Markets have so far not priced in significant escalation risk.Semis: Semiconductor stocks carry stretched valuations driven by AI excitement, but investors would do well to remember that semis are a cyclical business with long, barren stretches — Nvidia and TSMC both went sideways for over a decade before their recent runs. Today’s buyers face none of the “toil and trouble” of long-term holders, and the central question is whether current earnings reflect durable demand or short-term euphoria.

This Week’s Roundup

The remarkable rally in precious metals to start this year seems very distant. Gold has given up all its gains and is now down by about 8%. Wednesday saw it drop below $4,000 per ounce for the first time in eight months.

That reversal has played out thanks to gold’s loss of haven appeal, even as three months of fighting in the Middle East gave investors powerful need of somewhere to shelter. It’s also driven by a broader unwinding of the debasement trade that had probably started to fray before the war.

What is the debasement trade?

The debasement trade is the idea that governments and central banks, by running large deficits and expanding money supply, are gradually eroding the purchasing power of fiat currencies. Investors who believe this will happen position themselves in assets they expect to hold value as the currency weakens.

The core logic: when a government spends more than it collects in taxes and funds the gap by issuing debt (which central banks may then monetise by buying bonds and creating money), each unit of currency represents a smaller claim on real goods and services over time. The currency is “debased.”

The typical debasement trade portfolio buys gold, silver, Bitcoin, commodities, real assets like property and infrastructure, energy stocks, and sometimes foreign currencies or short positions on government bonds. The bet is that these assets will appreciate in nominal terms as the currency loses value, even if their real value stays roughly flat.

It has been a recurring theme since the 2008 financial crisis, when quantitative easing by the Fed and other central banks prompted the first big wave of gold buying and later Bitcoin adoption under this thesis. It came back strongly post-COVID when deficit spending exploded globally.

The trade is not without controversy. Critics point out that currency debasement predictions have been made continuously since 2009 without hyperinflation materialising in most developed economies, and that gold and Bitcoin can go through long fallow periods even when deficits are high. Proponents counter that the effects are cumulative and that the inflation of the 2020s proved their case.

In the current environment, with the US running deficits above 6% of GDP, debt-to-GDP around 100%, and global de-dollarisation discussions gaining traction, the debasement trade has found renewed interest, which partly explains gold’s run to above $4,000 per ounce and Bitcoin’s resurgence.

Kevin Warsh’s nomination as Federal Reserve chair in January (over candidates seen as beholden to President Donald Trump’s more dovish agenda) likely marked the shift in expectations that ultimately undermined the trade.

The debasement trade is primarily about the fear that policymakers (in the US and elsewhere) will inflate away unsustainable debt burdens.

When you inflate away debt, you turn on the printing presses. So monetary policy is an accessory. But the root cause is bad fiscal policy. That’s why you have to turn on the printing presses.

This explains why the markets paid close attention to the announcement of Jay Powell’s successor in unusual detail. Warsh was nominated amid persistent calls from Trump for lower interest rates (which should help the gold price), but his nomination immediately rattled investors. Gold tumbled as much as 13% from an all-time high that day, its steepest decline in more than four decades, while its putative modern replacement, Bitcoin, subsequently collapsed.

The dollar, meanwhile, found a bottom after a prolonged slide. Its surge has been given extra force by the end of the war, and the DXY broad dollar index closed the week at a 14-month high:

Warsh’s reputation as an inflation hawk sowed doubt about whether rates would continue to fall under his leadership. Any lingering fear that the Fed might ignore renewed inflation pressures was quickly dispelled by the new chairman’s maiden press conference, where he emphasised price stability above all else. But the narrative of a new hawkishness may be overblown. The energy shock is dissipating quickly in the wake of the peace deal, and that has brought down inflation expectations even more sharply. If Warsh wants more room to cut rates, this should give it to him.

The issue here is that prevailing inflation wasn’t driven solely by the closure of the Strait of Hormuz. Even as the waterway reopens, price pressures increasingly appear to extend beyond energy. That helps to explain the Fed’s hawkish tilt. investors who celebrate the slaying of the inflation dragon before it’s dead will be disappointed.

The Iran peace deal should ease one source of stress. Oil prices should not spike to $200, and US inflation should not revisit its 2022 peak if the Straits of Hormuz remain open. However, inflation will not return to the 2% target and will remain stuck at a 3.5%-4% plateau until the next inflationary shock.

Driven by the strong April CPI, hot May non-farm payrolls, and a hawkish Fed, Slok argues that there is a new market narrative, in which reopening the Strait overheats the economy and forces the Fed to raise interest rates soon. And indeed, Bloomberg’s World Interest Rate Probabilities function shows rate expectations increasing when the crude price rose, but then climbing further as it fell:

Such projections support the dollar’s renewed strength. Standard

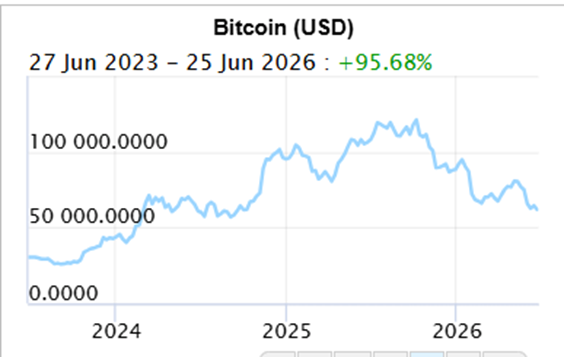

A stronger dollar won’t be popular in the White House, and could exacerbate Bitcoin’s woes. The dollar index has climbed to its highest in more than a year, while the cryptocurrency is hovering near its lowest price since 2024. Given Bitcoin’s longstanding inverse relationship with the dollar, this isn’t a modest tailwind.

AI – all honeymoons have to end – now it’s the hard graft

In three short years, AI has gone from being a topic reserved for sci-fi to dominating mainstream media.

Even the shiniest balloon has its limits, and when it comes to the top, there is almost always shudders before the fall. Last week’s Kospi crash might just be one of those’before shocks’.

Even as we plebs learnt the term ‘token maxxing’ (the corporate practice of encouraging employees to use as much AI as possible ), it is already out of fashion. The real adoption of AI in the workplace is still pretty narrow and is really just admin on steroids at this point. Not much different, frankly, to the role PCs played decades ago. It is probably having a greater impact on individuals who have embraced the technology and are harnessing it and customising it to quietly improve their individual productivity. Unfortunately, those hyperscalers need to keep rapidly expanding sales to justify their huge valuations. That can only come from corporates – in the short term. Hyperscalers are hoping that they can become the industry standard in subscriptions, like Microsoft is today, but we are a long way off that. Everyone is looking for the next ‘Killer app’, but that is elusive and evolving so fast that it has the shelf life of a ‘ready-to-eat’ avocado.

The Kospi’s meltdown – a snapshot for posterity

South Korea’s KOSPI index suffered one of its worst single-day collapses in history on Tuesday, June 23, plunging 9.99% in what traders quickly dubbed “Black Tuesday.” The crash was so severe it triggered a 20-minute circuit-breaker halt on the Korea Exchange, with more than $2.5 billion in foreign capital flooding out of the market in a single session.

Three catalysts converged at once: MSCI announced it would again exclude South Korea from its Developed Markets watchlist, the country’s fourth consecutive failed attempt, citing persistent shortcomings in market accessibility for foreign investors, particularly around won-denominated transactions; a hawkish Federal Reserve meeting on June 17 had already unnerved global AI and semiconductor bulls; and regulators raised fresh concerns about leveraged single-stock ETFs tied to Samsung and SK Hynix.

Those two chipmakers, which together account for roughly half the KOSPI’s market cap, both fell over 10-12%, dragging the entire index down with them. The collapse also came after a record rally had pushed the KOSPI to all-time highs, leaving stretched valuations vulnerable to forced liquidations among highly leveraged retail investors.

| Stock | Change | Note |

| Samsung Electronics | -10%+ | Circuit breaker triggered; +10% Wed on buyback speculation |

| SK Hynix | -12%+ | +5% Wed as AI/memory demand sentiment improved |

| SanDisk (US) | -11% | Memory chip contagion hit US-listed peers |

| Micron Technology (US) | -10% | Broad semiconductor de-risking |

| SoftBank (Japan) | -15% | Largest Nikkei casualty; AI portfolio exposure |

The market staged a sharp recovery on Wednesday, June 24, climbing more than 4.1% as aggressive short-covering swept through Seoul trading desks. The primary fuel for the bounce was speculation that Samsung Electronics was preparing a massive share buyback program worth approximately 90 trillion won — news that sent the stock surging as much as 10% intraday.

SK Hynix also gained more than 5% as sentiment around AI and data-centre memory demand stabilised. The recovery was notable in its speed and scale, though analysts cautioned it reflected relief rather than a fundamental shift, with the MSCI exclusion still locking out billions in potential passive fund inflows from global index-tracking ETFs and pension funds. South Korea’s next realistic window for MSCI Developed Market inclusion now pushes to June 2028 at the earliest.

If you thought the US AI story was impressive, look at this graph of the Kospi:

FOMO yet?

The contagion was swift and broad. Japan’s Nikkei 225 fell 3.6% in early Tuesday trading before partially recovering to close down 0.74% at 69,274. The Philadelphia Semiconductor Index — the closest American proxy for global AI-chip sentiment — shed approximately 8%, while SanDisk plunged 11% and Micron dropped 10% as the Korean market rout hit memory chip stocks stateside.

The Nasdaq Composite closed down 2.21% and the S&P 500 lost 1.44%, with European tech stocks shedding 2.7% in early trading. By Wednesday, global markets were stabilising: the Dow rose 0.35%, the KOSPI held its gains above 8,400, and the Nikkei declined a more modest 0.88% — suggesting the worst of the contagion had passed, even as the structural question of South Korea’s market accessibility remains unresolved. Was this a warning, a clarion bell, a canary in the mineshaft?

In the space of a few months, Japan has gone from a stagnant, mature economy to one that is fighting to reclaim some of that lost glory, and, in a pearl-clutching moment from the last remnants of the silent generation, rebuilding its military. This is probably not because they want to go back to the neo-colonial period of WW2, but a stark realisation that the US is not going to protect them from China if push comes to shove. In fact, they are far more likely to push them under the bus, especially in the current Fanta-tinted world of the current administration.

Prime Minister Sanae Takaichi is overhauling Japan’s budgeting process with a new multi-year framework and finance policies. This follows the rollout of a proposed ¥370 trillion ($2.3 trillion), 14-year investment plan for sectors like AI and semiconductors, aimed at bolstering the economy.

Most of the country is concerned about escalating violence on the anti-immigration platform that is being pushed by radio personality Jacina Ngobese-Zuma (she is not related to Jacob Zuma, but the inferred association hasn’t hurt). This too will pass, but people are already being hurt, and it will have a ripple effect on our reputation unless it is properly handled by the authorities.

If you haven’t been following the local news, the anti-immigration movement “March March” was founded by former radio show host Jacinta Ngobese-Zuma. The name March-March has always been English, but the Zulu phrase is associated with the movement is “Mabahambe” (meaning “they must go”) is a slogan protesters chant, but that is separate from the movement’s name.

The movement has set June 30 as a deadline for undocumented migrants to self-deport. Violence has already preceded it: unrest near Mossel Bay in late May left five Mozambican nationals and two South Africans dead, 55 shacks burned, and some 800 Mozambicans displaced. Thousands of Malawians and Nigerians have since fled the country, with repatriation centres established in Durban.

Despite Ngobese-Zuma’s insistence that March and March is non-partisan, the movement’s links to former president Jacob Zuma’s MK Party are well-documented. The movement’s National Treasurer was a candidate on MK’s 2024 election list, and MK’s secretary-general led a protest in Durban alongside Ngobese-Zuma. MK has confirmed it will join the 30 June march.

ANC secretary-general Fikile Mbalula accused Zuma directly at a June 25 press conference of “manufacturing chaos” to collapse state institutions ahead of November’s local government elections, drawing parallels to the July 2021 unrest that killed more than 300 people and cost the economy R50 billion. This probably goes to the heart of the protests’ motivation.

The government has deployed a R600-million SAPS operation and President Ramaphosa has urged restraint, but critics argue that by conducting immigration raids in response to March and March’s demands rather than prosecuting those inciting violence, the state has ceded the narrative. With 160 civil society organisations calling for urgent presidential intervention and multiple political parties having courted Ngobese-Zuma ahead of the polls, what began as a fringe grievance has become the defining issue of South Africa’s pre-election moment. The rest of the world is looking on carefully.

South African President Cyril Ramaphosa said the government won’t allow anyone to destabilise the country, following a series of xenophobic attacks and anti-immigrant demonstrations.

The nation’s security forces are ready to prevent any disruption, Ramaphosa told lawmakers in Cape Town on Thursday, ahead of a month-end deadline imposed by xenophobic protest groups for undocumented migrants to leave the country.

“Those who transgress will meet the full might of the law,” he said. “We want this whole process of immigration to be handled in the parameters of our law and as smoothly as possible.”

The protests have had little impact on South Africa’s financial assets, though investors are monitoring the steps the government is taking to head off any widespread violence.

So far, the market does not appear to be pricing in a material escalation scenario, and implied volatility has not signalled widespread concern about a repeat of the July 2021 unrest. Ramaphosa’s comments follow similar remarks by Geordin Hill-Lewis, the leader of the nation’s second-biggest party, who on Wednesday called on the government to take a strong stand against xenophobic violence. Remember that the MK party is not part of the GNU despite coming 3rd in the elections.

Author: Dawn Ridler

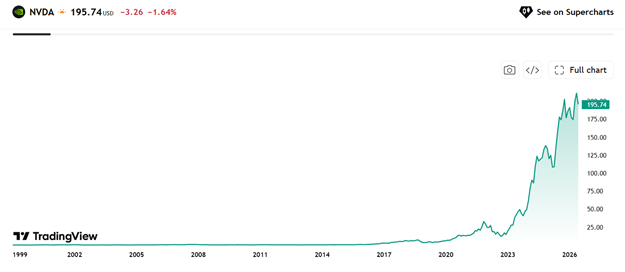

It was back in 2022 when Nvidia was trading at $15 when they introduced their GPU line of datacenter chips. This occurred alongside the AI boom and before you knew it, Nvidia’s share price was trading like it was a gift to markets. But one shouldn’t forget that before this, Nvidia was a chip manufacturer competing against other companies in this space, often competing on the never-ending spiral of price and performance. In the semiconductor industry (also called semis), being the first mover comes with risk and clearly a vast opportunity if you get your timing right.

But what many investors forget is that there are periods when very little happens in the semiconductor space. Take Nvidia again. From the beginning of 2002 to 2015 almost nothing happened with the share price. This is the time when only industry insiders are exited by technical developments at the semis and investors are sceptical about a company’s ability to generate profits in the future. These are the long, lonely yards. Take Taiwan Semiconductor Manufacturing (TSMC). In a similar fashion this share price did nothing from early 2002 to 2012. A similar story to Nvidia.

This is a graveyard for capital as cash allocated creates no return. Fast forward to today. The promise of an AI led world is forcing the valuations for these stocks higher whilst their underlying businesses, that of design and manufacturing of semis, hasn’t changed at all. AI will certainly change the way we work and yes, it will make us far more reliant on data going forward. But does all of this translate into an insatiable desire for semis in the future which makes almost any price an investor pays reasonable today? The market will want you to think this, but in reality it would be proved wrong in the long run.

And this is the problem with investors. At some point investors lose the battle against their good sense. At its core the emotions of fear and greed are very strong. It’s what makes us human and our ability to ignore these emotions is a fight against nature itself. We all want to believe that we can conquer these but alas markets can stay irrational for long periods of time.

At some point investors capitulate and start believing that “This time is different”. We forget the toil and trouble managers and owners of semis needed to go through in the quest to outdo their competitors, whilst their share prices went nowhere. On paper they all had the shares or options but none of that produced life changing money for a long time. Think what it took for Jensen Huang from Nvidia to keep believing through the thin years to harvest today. Think of the countless engineers who work in this sector and have merely paid the bills until today. For an investor to become involved in semis today doesn’t need any toil or trouble… it merely requires a belief that we have never seen the likes of AI before. Who sells the new investor the shares? It must be someone who has been a long-term owner and knows that semiconductors are a cyclical business.

There is a saying in markets that you don’t need to be a genius to make money from markets, but you do need patience. Unfortunately, this is the one thing many investors lack. We live in a world where instant gratification has become the norm rather than the exception. It is expected and spills over into our investment lives. We seek expertise and we measure this in returns.

We are experiencing an IPO season where companies are being sold on promises. Many of these companies do produce earnings which makes the comparison with the dotcom boom flawed. The question the market will answer in time is how robust these earnings are. So if an investor measures returns today, a good question would be if they are measuring expertise or euphoria?I would argue that today’s expertise doesn’t come with the best returns. Alas now one needs patience which as always is in short supply.

Author: Cobie Le Grange

EXCHANGE RATES and other Indices:

The Rand/Dollar closed at R16.40(R16.39, R16.27, R16.55, R16.23, R16.46, R16.68, R16.39, R16.63, R16.29, R16.41, R17.07, R17.06, R16.89, R16.55, R15.93, R16.01, R15.96, R16,03, R16.15, R16.10, R16.50, …R16.91, R17.13, R17.36, R17.13,16.52 )

The Rand/Pound closed at R21.64(R21.67, R21.80, R22.06, R21.80, R22.09, R22.21, R22.30, R22.56, R22.35, R22.02, R22.09, R22.77, R22.76, R22.35, R22.20, R21.48, R21.59, R21.78, R21,82, R22.11, R21.97, R22.13, …R22.57, R22.68, R22.74, R22.56

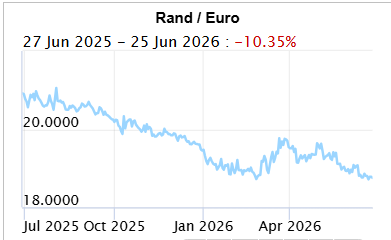

The Rand/Euro closed the week at R18.66(R18.89, R19.16, R19.08, R18.91, R19.11, R19.38, R19.29, R19.48, R19.37, R19.17, R19.24, R19.70, R19.77, R19.33, R19.23, R18.80, R18.87, R18.94, R18.93, R19.14, R19.04, R19.20)

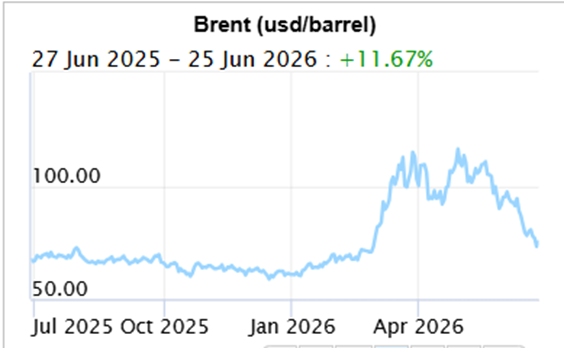

Brent Crude: Closed the week $71.99($80.59, $87.33, $93.09, $91.12, $104,24, $109.26, $101.29, $108.83, $105.33, $90.38, $95.20, $107.88, $112.36, $103.14, $92.88, $73.19, $71.76, $67.75, $68,05, $69.32, $65.88, $63.34, …$63.71, $63.19, )

Bitcoin closed at $60,063($64,029, $64,131,$60,762, $73,788, $74,559, $77,879, $80,733, $78,204, $78,049.98, $75,519, $70,904, $68,691 , $68,586, $70,869, $67,310, $63,534, $68,04, $69,649, $68,553, $81,301, $89,295, $90,585,)

Articles and Blogs:

Legacy Series Part 4 NEW

Legacy Series part 3

Legacy Series Part 2

Legacy Series Part 1

Holiday checklist

Next year – Action Plan

Next year – Vision, Mission etc

Medical Risk Mitigation

Next Year – Consolidation

Abdication or diversification?

Carbo-loading your retirement Spoiled for choice

Who needs a plan anyway

8 questions you need to ask about retirement

What to do when interest rates drop

How to survive volatility in your investments

What to do when interest rates drop

Difficult Financial Conversations

Financial Implications of Longevity

Kick Start Your Own Retirement Plan

You matter more than your kids in retirement

To catch a falling knife

Income at retirement

2025 Budget

Apportioning blame for your financial state

Tempering fear and greed

New Year’s resolutions over? Try a Wealth Bingo Card instead.

Wills and Estate Planning (comprehensive 3 in one post)

Pre-retirement – The make-or-break moments

Some unconventional thoughts on wealth and risk management

Wealth creation is a balancing act over time

Wealth traps waiting for unsuspecting entrepreneurs

Two Pot pension system demystified

Cobie Legrange and Dawn Ridler,

Rexsolom Invest, Licensed FSP 45521.

Email: cobie@rexsolom.co.za, dawn@rexsolom.co.za

Website: rexsolom.co.za, wealthecology.co.za