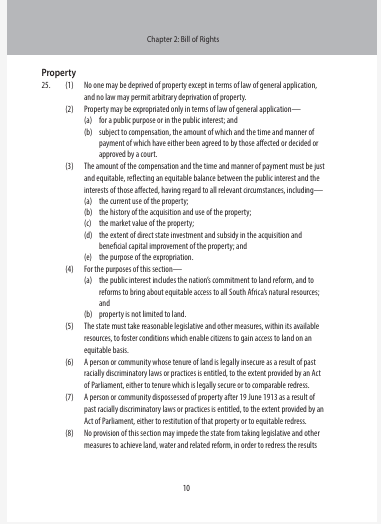

| Welcome back to our Newsletter and podcast – We hope you had a great break and looking forward to a happy, healthy and above all, prosperous 2025. Cobie and I like to keep this newsletter and our podcast evolving. We’d love to hear from you about what you like or dislike, what you’d like more or less of – both in the newsletter and podcasts. Do you have topics you’d like to hear a blog on? Do other people’s wealth journeys interest you? Market Watch The JSE is back to the familiar pattern of catching a breath and moving sideways – next week might just be choppy!. This week, for a change, I am looking at 10-year graphs – note how the JSE moves in fits and starts but Wall Street (apart from the pandemic blip) has been in an almost constant bull market for over a decade. At what stage do we declare that cycles are over?   Appropriation Without Compensation – some perspective South Africa has a new law to govern the expropriation (or compulsory acquisition) of private property by the government for public purposes or in the public interest. The passing of the Expropriation Act 13 of 2024 followed a parliamentary process that began in 2020. The act repeals the apartheid-era Expropriation Act 63 of 1975 and aims to align expropriation law with the Constitution. It sets out the procedures, rules, and regulations for expropriation. Besides setting out in quite a detailed fashion how expropriations are to take place, the act also provides an outline regarding how compensation is to be determined. Some South Africans have expressed impatience with the slow pace of land reform ( a popular soapbox for Julius). Note, however, that this is not due to unwilling sellers, far from it, it is thanks in the main to the land claims process which, frankly, borders on gross incompetence. Twenty-two years later, less than half of the claims have been resolved. There is much debate in the country about the provisions of the new act. The debate is mostly about the extent to which it affects existing private property rights. Some argue the act is unconstitutional, while others welcome it as a necessary step in the right direction. There is absolutely no doubt that this is now going to enter into robust legal challenges – especially if it is ‘imprudently implemented’. The biggest controversy with this act is the ‘without compensation’ part. That is a euphemism but sounds better than confiscation – which is what it actually is. That smacks of communism. If there was a refusal to negotiate a financial settlement with land claims parties it would be one thing, but it isn’t. Land redistribution is not a new concept – but you can go the Zim route of wholesale confiscation or what happened in Kenya – compulsory purchase orders – which were done at market value but you had no option but to move. According to most experts, the ‘without compensation’ part would only be used in exceptional circumstances. I think most of us agree that if a piece of property has been effectively abandoned or has built up huge arrears, there might be a case for ‘confiscation’. Apparently, the property will only be ‘expropriated’ for public use. That is not particularly controversial and is found in the laws all over the world, but it is bought not confiscated (just to clarify the smoke and mirrors talk) I know there is the fear that this act will be used to implement land claims etc in a wholesale fashion aka Zimbabwe, but the international outcry would be huge and relegate us firmly to persona non-grata status for a very long time. The biggest concern is that the appropriation would be ‘arbitrary’ and not just used for government good. One aspect you might see being proposed in the constitutional challenges is that the govt has to enter into a negotiation with the property owner first. The Act is freely available online it’s 52 pages (but in multiple languages so not that bad), I’ve read though it so you don’t have to and here are some of the low lights:  One interesting thing to note is the inclusion of the mortgage here – this has long been one of the big bones of contention. In terms of current laws around mortgages – the mortgage would still have to be paid even if the property has been confiscated. The bank has a lien, as it were, on that asset – and you don’t get the deeds back from the Master until the mortgage has been cancelled. Here is one of the other controversial sections:  One of the important sections to consider here is 3(a) – property held for investment aka speculation. The wording of the controversial AWC aka ‘confiscation’ clause. Section 12 of the act deals with compensation for expropriation. It is arguably the most controversial part of the new legislation. Section 12(1) does not appear problematic and is largely the same wording as Section 25(3) of the Constitution. This part of the property clause sets out what must be taken into account when compensation for expropriation is determined. Section 12(3) of the act refers to “nil compensation” – when nil rand (monetary) compensation may be paid. There is no explicit reference to nil compensation in the current wording of Section 25 of the Constitution. It’s a new thing in the Expropriation Act. This is what all the fuss is about. (Also freely available online)  The circumstances in which nil compensation could be granted in terms of the new act are, in fact, very limited. Section 12(3) leaves the discretion to the expropriating authority to determine when it may be just and equitable to pay nil compensation. However, the act lacks guidelines on how such a discretion must be exercised. This is going to have to be fixed. The scope of Section 12(3) is also limited in some respects. For one, it is restricted to land. Only where land is expropriated would nil compensation be an option. Some of the fear-mongering in the media assumes that it applies to all assets, and they could come and ‘acquire’ your GWagon. Not all forms of property can be expropriated without compensation. The notion of property under Section 25(1) of the Constitution is generally wide and includes various rights and interests, which are broader than just land. For instance, personal rights, mineral rights, and licences are included under the Section 25(1) notion of property. This wide understanding of property is not applicable to Section 12(3), which refers to “land” being expropriated. Section 12(3) is also limited to the expropriation of land “in the public interest”. Nil compensation is therefore envisaged only in the context of expropriation of land undertaken in the public interest, and not also for a public purpose. Three of the four categories listed in Section 12(3), where nil compensation is envisaged, are linked to the way in which the property was being used prior to the expropriation. Land used in a productive manner is therefore not evidently envisaged under Section 12(3). This is not an objective measure and is likely to be contested in court. In short, the act forces South Africans to engage with the idea of nil compensation in a much more direct manner. The presence of a clause dedicated to nil compensation provides new clarity on when this could apply. Frankly, why the ANC decided to publish it now is a mystery – didn’t they know it was going to cause a problem with their GNU partners? It is hard to determine whether this act will pass constitutional muster without seeing how expropriation under it will work in practice. It remains to be seen whether it will have the far-reaching consequences many fear or call for. Lawyers are waiting to pounce on the first real instance of this law being used in a controversial case.  The Copper Colonialist is at it again. Not happy with the mayhem around his Fanta Fascism, DJT has been a busy boy. This mass-chaos tactic should come as no surprise – Bannon gave us the inside skinny on the tactic years ago. Basically – bombard them with 3 (crazy) ideas every day, and maybe one will stick.  Trump’s “Flood the Zone” In 2018, the former Trump administration strategist Stephen K. Bannon boasted of the ability to overwhelm Democrats and any media opposition through a determined effort to “flood the zone” with initiatives. That’s what we’re seeing here. I don’t know about you, but the 3 weeks since Trump’s election feels more like a year. This time around, the flood is bigger, wider and more brutally efficient. As President Trump begins his second term, he has enacted his agenda at breakneck speed as part of an intentional plan to knock his opponents off balance and dilute their response. Firing inspectors general. Sweeping clemency for Jan. 6 defendants. Investigations of perceived enemies. A federal hiring freeze. Moving to end birthright citizenship. An immigration crackdown. Terminating diversity, equity and inclusion programs. Revoking security clearances. On Tuesday, just when Democrats thought they might come up for air, news broke that Mr. Trump had ordered a freeze on trillions of dollars in federal grants and loans, prompting a new round of outrage. In a speech on Thursday, the fellow felon, Bannon, expanded on this infamous tactic: The president “understands how close he came to political oblivion, and I think he also understands that this’ll be remembered as the age of Trump,” Bannon added later. “He’ll be at the level of General Washington and Lincoln and then Trump, of turning around … the country, I think he’s stepping into the moment,” Bannon said. There is no doubt the democrats have been left reeling – but they had better come up with a plan if they have any chance of winning back the house and the senate in two years time.  Trump and Inflation – the tightrope All the back and forth on Tariffs, which Trump is using as a sledgehammer negotiating tactic with the US’s trading partners — if imposed and maintained — would act like a bucketful of sand in the wheels of the global economic machinery. Companies have had time to prepare by frontloading inventory builds and diversifying supply chains, but tariffs would still be disruptive and impose significant extra costs. The US should fare better in a full trade dispute because of its relatively closed economy, but this overlooks the interplay between the US stock market and the US dollar. A steep fall in US equities in response to tariffs might well dampen foreign investors’ enthusiasm for holding US stocks. More to the point, a steep fall in US equities would blow a hole in US households’ net worth. The entire increase in US net wealth since 2022 is attributable to higher equity prices. So, if US households respond to a fall in equities by curtailing their consumption in order to save more of their earnings, growth in the highly consumer-dependent US economy would suffer. Remember 70% of US GDP comes from consumer consumption A steep fall in US equities is also what the new administration badly wants to avoid, while an exit of foreign investors would make it much harder to keep the lid on bond yields. After the climbdown on Mexico and Canada, the assumption appears to be that Trump 2.0 doesn’t mean tariffs any more drastic than in his first term. That’s allowing bond yields to come down and helping the growth agenda (while disappointing the many who had bet on more US exceptionalism and higher yields). Moving ahead with tariffs could make Bessent’s life much more difficult.  Medicare and Medicaid – Universal Health Care (UHC) provision-“lite” The provision of health care and the associated costs around the world is often a hot topic – especially here at home in RSA with the signing into law of the NHI bill last year. The bottom line is that in most countries around the world that have some sort of UHC ( unless they are truly social and have large budget surpluses – countries like Norway) are largely inefficient. In the UK, the operational standard in Accident and Emergency is 4 hours, but in many cases the wait is over 12 hours (which correlates to a 40% increase expectancy of death of a patient). This is not much different to what you’d expect in an RSA govt hospital, frankly. Hospital care etc in the US is notoriously expensive, and the cost of drugs, specifically, often orders of magnitude higher than you find even in Europe. Medicare and Medicaid are now in the DOGE (aka Musk) firing line. Medicare is largely age-based and available to most seniors, whereas Medicaid is income-based and offers assistance to people with limited income and resources. As of last week, Elon Musk’s Department of Government Efficiency has gained access to the inner workings of Health and Human Services, including data systems of the agency that manages a nearly $2 trillion budget, handles Medicare and Medicaid benefits and runs the National Institutes of Health, the world’s biggest biomedical research institution. Why? According to Musk – this is where the big money fraud is happening. However, The federal government has long-established channels for rooting out overspending and wrongdoing in health programs. They recoup billions of taxpayer dollars each year. • HHS (Health and Human Services) inspectors recovered $7.13 billion for the federal government in misspent taxpayer funds during fiscal year 2024. The Justice Department brought in another $1.7 billion in settlements and judgements from health care-related litigation on false claims. • Trump fired HHS inspector general Christi Grimm last week. Ironically, the larger percentage of those who are impacted by this intrusion and potential cutting off of benefits are MAGA supporters. Middle America is in Season 2 of the FAFO biopic of Trumpism and Trumponomics – which will probably not be as fondly remembered as Reganomics.  Steinhof update For anyone who is still interested in the Shenanigans that brought down Steinhoff, Rob Rose (who wrote a brilliant book on the topic, and was involved in the documentary)has written a series of articles – now that the 7000-page forensic report has been released. You can read the series of articles on Currency News  RSA – The run-up to the budget and the Social Security tax. Forget the NHI, we have anew tax to worry about – Social Security. Although the NHI was promulgated into law, there are years of groundwork that has to take place before we’re likely to see even the start of those proposals are implemented. In a document leaked to the press last week following an ANC imbizo – they are now floating a “Social Security Tax” to fund yet another grant – the basic income grant aka BIG. This is the ‘spin” around the proposal • South Africa does not have a comprehensive social security system, so there are no significant social security taxes. (Sure, it just falls under a different section – last year RSA spent R370bn on the various Grants)  • The ANC has said that it will use progressive tax measures (i.e the more you earn, the more you pay), including a social security tax, to fund the BIG. • The ANC has also said that the BIG should complement existing social security programs, such as the Child Support Grant. (i.e more, not consolidation or replacement) • The ANC has said that it will finalize a policy on the BIG within two years of a new ANC administration. (Is the GNU a ‘new administration – I doubt it). • The ANC has said that the BIG should be universal, basic, and income-based Last week was the State of the Nation – then it’s the budget time again on the 19th of Feb The fiscal slippage has become a general trend in South Africa, as in most cases the fiscal metrics deteriorate, with only very occasional cases of improved outlooks, as occurred when savings in the GFECRA – Gold and Foreign Contingency Reserve Account (the new govt piggy bank) account were earmarked last year. The latest gross debt to GDP ratio (October’s MTBPS – Medium Term Budget Statement, aka mini-budget) was projected to peak at 75.5% of GDP in 2025/26, well above the debt ratio of 60% of GDP instead seen as the maximum sustainable debt ratio for an emerging market economy. Isn’t it funny how projections, as seen in the graph below, always show the situation ‘turning around’ – who are they fooling?  State expenditure for the fiscal year to date is lower as a % of the estimated budget outcome this fiscal year compared to last, at 72.7% vs. 74.2%, for the first three quarters of the fiscal year. This is one of the key numbers we will be looking at in the Budget. While the National Treasury sets the inflation target, and the Reserve Bank is tasked with achieving the target, the Reserve Bank has stated it believes there is a need to lower the inflation target. National Treasury has worried about negative effects that could ensue on the economy and households, while the SARB has already published research on the positive implications from lowering the target. Overall, for the Budget, state finances are not strong, and this weakness, combined with better-than-expected inflation but lower-than-expected GDP outcomes, means further fiscal slippage remains a risk. Expenditure continues to outpace revenue and this is unsustainable – the ANC’s solution seems to be more taxes – but thinly disguised as something else – like Social Security “Levy” and NHI “contributions”. The one nasty shock I have been expecting from a budget is the removal of the medical aid tax credit, maybe not for over 65s, but for everyone else. In the graph below the one thing that will jump out at you is the increased cost of our borrowing – the cost of the government not living within their means. It’s like the rest of maxing out our credit cards, and just opening a new card to pay the interest on those other cards – one day the music stops and that debt has to be paid (unless you’re in the US apparently)   Trump, the FED and Bessent Amid all the excitement surrounding Trump 2.0, his Treasury secretary, the highly respected hedge-fund manager Scott Bessent, has voiced a clear economic target that he shares with the president. “He and I are focused on the 10-year Treasury,” he said in an interview with Fox Business. “He is not calling for the Fed to lower rates.” Long may it last – and he may at least have a good shot at maintaining the independence. If DJT’s base doesn’t understand tariffs, they sure won’t understand Treasury bonds. Arguably, 10-year Treasury benchmark is the most important rate in the entire global economy, and elected politicians should keep their hands off an independent central bank (taking notes, Cyril?) The problem is that nobody controls the Treasury yield — it’s set by one of the world’s biggest and most liquid markets. In the years before the Global Financial Crisis, Alan Greenspan’s Federal Reserve famously tried to push up the 10-year yield and couldn’t. It became known as the conundrum. To keep yields down, central banks and governments can buy industrial quantities of bonds — the dreaded quantitative easing, a policy that amplified inequality to excruciating levels and that hopefully, no one wants to repeat. Bessent also has to contend with the almost universal belief in markets that Trump 2.0 means higher 10-year yields. The argument is that tax cuts will mean higher deficits and higher yields to finance them, while tariffs will raise inflation. That brings higher yields in its wake. It is no surprise then that yields rose sharply during the last quarter of last year, from a low in the brief period around the president’s debate with Kamala Harris when his chances looked to be weakening. It’s natural that the administration wants lower rates, the argument goes. Who wouldn’t? But their agenda will make it mighty difficult to achieve. And yet… Bond yields are falling. The 10-year has shed 40 basis points in barely a month. And despite every other headline as the new president behaves like a bull in a china shop, the big bond market event of the year, so far, was the December inflation data. Nothing else comes close. The graph below shows the 10-year treasury rate over a long period of time  Disinflation is happening painfully slowly. However, the numbers were quiescent enough to dispel the notion that price rises were already resurging and that the Trump Trade had been overdone (hold my beer). Since then, traders reacting to his actions rather than his words have continued — with occasional interruptions — to step back from bets on rising rates and inflation. In the process, they’ve also stepped back from bets on American Exceptionalism. US unemployment was out Friday (to complete) The key audience will be in the Federal Reserve, rather than the White House. The assumption is that the job numbers will do nothing to persuade it to move interest rates either up or down, and the week’s data download has so far supported that. The estimate of private sector jobs from the payroll group ADP, which tends to be less volatile than the official number, suggests that the economy continues to produce an average of a bit less than 200,000 jobs each month, as it has for two years now: Author: Dawn Ridler  2 steps forward and 3 steps …… You’ve probably seen the fiasco around the expropriation without compensation bill last week (Dawn went into it in more detail above) and the ensuing fallout with the US government. In short, the US has noticed the slow failure of South Africa and has called the ANC out for it. Actually, they ask pretty good questions of the ANC and because accountability has now become real it’s going to be difficult to answer appropriately without relying on the old playbook of African nationalism. A difficult task ahead for Cyril Ramaphosa given that he is dealing with this, the DRC matter, NHI and attempting to attract capital to South Africa. USAID is finished not only for us but also for the rest of the world. I am pretty sure aid will be delivered but this will come as part of newly negotiated bilateral trade agreements with the US. I don’t believe South Africa can negotiate any deal with the US! In short, the US is cutting back on endless spending to focus on their own debt levels. In short, they are hoping to bring down the cost of energy to lower inflation and if they can get a handle on the debt levels this should drive longer dated bond yields lower. These are critically important steps for the US economy, and they will be doing this whilst at the same time cutting taxes. Not an easy task but I admire the American tenacity to deal with the real issues at hand. This certainly was lacking in previous dispensations. Making America great again requires friends, and it is this process that America is sifting through at present. When America signed the AGOA (African Growth and Opportunity act) in 2000, the President in South Africa was Thabo Mbeki. He actually took over in 1999 from Nelson Mandela under which South Africa had attained it’s wunderkind status as the world’s newest democracy attained without a civil war. Amazing stuff at the time and the benefits have been real. Then came the dark days under Jacob Zuma (2009-2018) and Cyril Ramaphosa (2018 to present). This is where ideology trumped over logic and the spoils of the economy is shared by a few at the expense of the rest. There is a saying in markets that risk happens slowly and then all at once. The same thing applies to politics. The wayward backward-looking policies of the ANC have been highlighted for many years within the borders of the country but the risk in the world order has slowly been building until the International Court of Justice (ICJ) watershed moment in 2023. When South Africa decided to lay genocidal charges at the ICJ (probably funded by Iran) against Israel for a war that we are not involved in nor have any geographic responsibility for, the invisible line had been crossed. Israel has many friends in the West including the USA and the spotlight had firmly been placed on South Africa and by default the policies of the ruling party. This brings me back to the expropriation bill. I don’t actually think the government wants to expropriate land. But what the bill does do is make the sector un-investable. Citizens stop buying property and renovations halt as market values stagnate or decline. Do this for long enough and there certainly will be property abandonment. Property loses its value as buyers depart and one of the largest wealth effects for the country stops. Think of a first-time home buyer being able to sell their home for a profit. It releases a large capital amount that the owner had invariably built through years of paying a mortgage. But for this to happen, property prices need to go up. All South Africans will suffer under this legislation but the middle class and emergent middle class in particular are being robbed of the wealth effect. Such a pity. At what point does ideology stop driving decision-making in South Africa? The Americans have been clear that a line has been crossed. But this doesn’t stop the ruling party from continuing in the name of an economic revolution. The time the ANC stops is when they either cease to exist or their backs are so against the wall that no other option but to concede exists. This can take a long time which is the real danger for South Africa at present. Author:- Cobie Legrange EXCHANGE RATES: The Dollar is still showing relative strength, and this will impact our exchange rate.  The Rand/Dollar closed at R18.41 (R18,67, R18.38, R18.73, R18.03, R18.05, R18.11, R18.21, R17.58, R17.60, R17.66, R 17.41, R17.48, R17.12, R17.42, R17.85, R17.82, R17.71, R17.85, R18.32, R18.26, R17.95, R18.23, R18.20)  The Rand/Pound closed at R22.85 (R23,16, R22.93, R22.80, R22.99, R22.98, R22.72, R22.99, R22.73, R22.72, R22.89, R22.75, R22.93, R22.90, R23.20, R23.44, R23.41, R23.13, R23.39, R23.28, R23.32, R23.34, R23.00, R22.63, )  The Rand/Euro closed the week at R19.02 (R19,35, R19.31, R19.23, R19.09, R18.87, R19.19, R18.85, R19.09, R19.07, R19.05, R19.19, R19.12, R19.47, R19.79, R19.72, R19.80, R19.70, R20.01, R19.94, R19.58, R19.74,)  Brent Crude: Closed the week at $74.65 ($76,40, $77.60, $79.98, $71.00, $72.38, $75.05, $70.87, $73.86, $73.99, $75.57, $78.67, $77.95, $71.96, $74.68, $71.47, $76.99, $79.05, $79.09, $79.43, $77.56, $85.03, $83.83, $84.86, $85.22).  Bitcoin closed at $96,286 ($99,049, $104,559, $104,971, $99,341, $97,113, $97,950, $90,679.47, $79,318, $68,277, $66,989, $62,876 , $62,267, $65,596, $62,603, $54,548, $57,947, $63,936, $59,152, $60,847, $61,903, $59,760,). Articles and Blogs: New Year’s resolutions over? Try a Wealth Bibgo Card instead.NEW Wills and Estate Planning (comprehensive 3 in one post) NEW Pre-retirement – The make-or-break moments Some unconventional thoughts on wealth and risk management Wealth creation is a balancing act over time Wealth traps waiting for unsuspecting entrepreneurs Two Pot pension system demystified Keeping your legacy shining bright Financial well-being when dealing with Dementia and Alzheimers Weathering the storm Pruning your wealth farm Should you change your investments with changing politics? Taking a holistic view of your wealth Why do I need a financial advisor? Costs Fees and Commissions The NHI and what to do about it New-Normal for Retirement? Locking-In Interest rates – The inflation story Situs – The Myths and Reality Tax Residency – New Rules new headaches Are retirement annuities dead A new look at retirement Offshore investing – an unpopular opinion Cobie Legrange and Dawn Ridler, Rexsolom Invest, Licensed FSP 45521. Email: cobie@rexsolom.co.za, dawn@rexsolom.co.za Website: rexsolom.co.za, wealthecology.co.za |

͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏