Your summary with links, if you’d like to curate your content:

Oil Reserves: The IEA coordinated its largest-ever emergency reserve release of 400 million barrels, dwarfing the 2022 Ukraine response. However, with Hormuz disruptions removing up to 16 million barrels per day, the release buys roughly 25 days of cover at best, a bridge and not a solution.

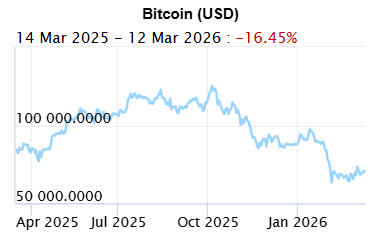

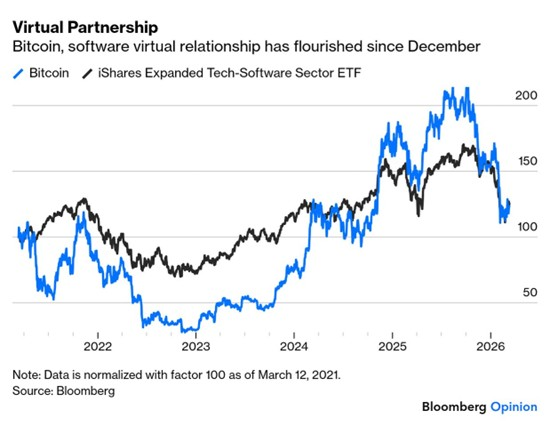

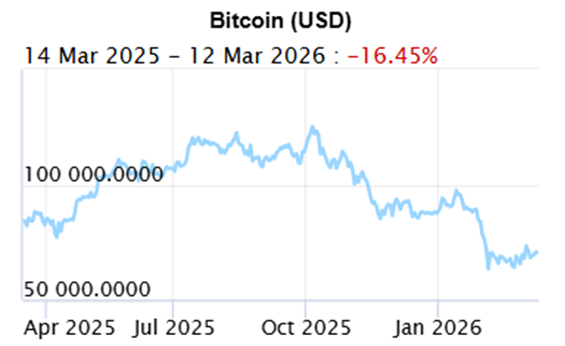

Bitcoin’s Golden Moment: Despite being down over 20% year-to-date, Bitcoin has quietly gained more than 5% since the outbreak of the Iran conflict, while gold dipped 2% over the same period. Its increasingly tight correlation with the software sector may hold clues to where it heads next.

Semantics: Force Majeure: The conflict has breathed new life into the legal concept of force majeure, with QatarEnergy and Aluminium Bahrain among those invoking the clause to excuse missed deliveries due to Hormuz-related disruptions.

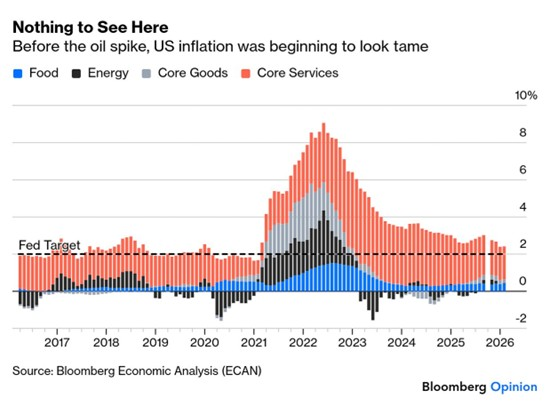

An Inflation Postscript: Tariffs have been slow to show up in official inflation data, and underlying trends were normalising, but the Gulf conflict changes that calculus entirely. Inflation swaps suggest a significant, if not catastrophic, upward price impact ahead.

Cost of the War: The first six days of the US-Iran conflict cost at least $11.3 billion, with munitions alone accounting for $5.6 billion in the opening two days. A supplemental funding request to Congress of around $50 billion is expected shortly.

And the Winner is… Russia? Reports emerged that Russia supplied Iran with targeting data used to strike US assets, killing seven American service members, yet Trump’s response was to call Putin for a “good chat” and float lifting oil sanctions. Ukraine, meanwhile, offered counter-drone technology that the White House initially dismissed, only to scramble for it once the Shahed drones were already falling.

Oil: Cobie’s take: Despite superior US and Israeli firepower, Iran holds a powerful card in its ability to disrupt oil flows through the Strait of Hormuz, where 20% of the world’s oil and LNG passes. With tankers being destroyed and drone attacks spreading across the region, this has become a race against time. A quick resolution favours the US and global markets; a prolonged conflict drives inflation higher, hurts growth, and hands greater influence to Russia and China. The broader takeaway is that commodities are increasingly strategic assets, and those who control them hold real power in an increasingly unstable world.

This Week’s Roundup

RSA

USA Markets & Economy

Global ex RSA/USA

Strategic petroleum reserves (SPRs) are government-held emergency stockpiles of crude oil, maintained to cushion economies against sudden supply disruptions. The US Strategic Petroleum Reserve is the world’s largest, with a capacity of around 714 million barrels stored in underground salt caverns along the Gulf Coast; current holdings sit at roughly 415 million barrels following a series of releases since 2022. The IEA coordinates collective action among member countries, which are obligated to hold reserves equivalent to 90 days of net oil imports. In a crisis like the current Hormuz closure, governments can release SPR barrels into the market to suppress price spikes and buy time for diplomatic or military resolution. The G7 is reportedly weighing the largest coordinated SPR release in history, but critics note that even a full release of all IEA member reserves would only cover around 60 days of the disrupted Hormuz flow, making reserves a bridge tool rather than a solution. Saudi Arabia and the UAE, whose exports are also constrained by the closure, have indicated they could reroute some supply via pipelines bypassing the Strait, though total bypass capacity covers only a fraction of normal throughput.

South Africa does not maintain a formal strategic petroleum reserve in the traditional sense. The country relies on a combination of commercial stockholding obligations, managed by the Central Energy Fund (CEF) and its subsidiary, the Strategic Fuel Fund (SFF), and mandatory industry stock requirements.

In 2015, South Africa controversially sold off a significant portion of its state-held reserves – around 10 million barrels – at what proved to be the bottom of the oil price cycle, a decision that drew heavy criticism from Parliament and the public. The SFF has since been tasked with rebuilding those holdings, but progress has been slow and opaque, with repeated auditor-general findings of poor governance at the entity. Current estimates put South Africa’s total commercial and strategic stocks at somewhere between 20 and 30 days of consumption cover, well below the IEA’s recommended 90-day benchmark (South Africa is not an IEA member, but uses it as a reference standard). With no domestic oil production on any scale and a refining sector severely constrained since the closure of the Sapref refinery in Durban, South Africa is acutely exposed to the current Hormuz disruption. Any sustained period of elevated global oil prices feeds directly into fuel price increases at the pump, transport costs, and ultimately food inflation – a particularly painful combination for a country where a large proportion of households spend the majority of their income on food and transport.

The International Energy Agency agreed to discharge 400 million barrels from emergency oil reserves, its largest-ever release, as governments seek to contain a price spike driven by the Middle East war. The volume far exceeds the 183 million barrels that member states released in 2022 after Russia invaded Ukraine. But potential supply losses from the current crisis may also be much larger, with the near-halt of flows through the critical Strait of Hormuz keeping vast amounts of crude and fuel out of the global market.

Heavy importer Japan, one of the countries most exposed to oil-price shocks, said it would release about 80 million barrels. The UK will contribute 13.5 million barrels, Germany about 19.5 million, and France as much as 14.5 million. South Korea plans to release 22.5 million barrels.

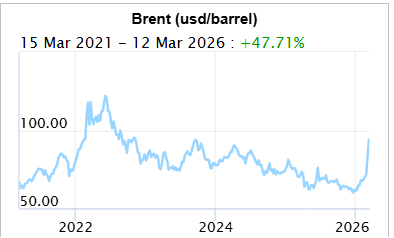

Oil soared to almost $120 a barrel in London earlier this week as flows through Hormuz remained essentially halted, though futures have since eased, in part on expectations that governments would tap their oil reserves. Prices dipped following Wednesday’s announcement, before ticking back up.

The IEA, which coordinates stockpile releases for OECD countries, has yet to give a breakdown of the types of oil included in Wednesday’s agreement — a detail important for energy traders looking to better understand the implications for different fuel and crude markets.

The last time the IEA coordinated a stock release, shortly after Russia’s invasion of Ukraine, the overall split was 73% crude and 27% products, with diesel-type fuels making up the largest share of the latter. The US was the top contributor, with 90.6 million barrels, all of which was crude oil.

Speaking privately, traders and analysts at large commodity trading houses and hedge funds have given a range of estimates for the rate at which barrels may hit the market this time around, largely between 2 million and 4 million barrels a day, though some put the figure lower at 1.2 million a day.

The effective closure of the Strait of Hormuz has caused storage tanks in Persian Gulf countries to fill up. As a result, major producers including Saudi Arabia, the United Arab Emirates and Iraq are deepening supply cuts, shaving about 6% off global output.

Asian importers take a much bigger share of the crude and oil products that normally flow through Hormuz than Europe or the US, suggesting the immediate impact of the Iran war should, overall, be much sharper in that region.

But that geographical split isn’t uniform across the barrel. Europe’s jet fuel market, for instance, is in dire need of supply. The fuel’s premium to crude has shot up since the conflict began, standing at almost $90 a barrel on Tuesday, according to figures from General Index. A similar measure for Asia is now significantly lower.

The IEA has said its 32 members hold more than 1.2 billion barrels in public emergency stockpiles, including the largest buffer, the US Strategic Petroleum Reserve, or SPR. There are a further 600 million barrels of industry stocks under government obligation.

These countries are obligated to hold at least 90 days of net oil imports, which may consist of stockpiles maintained exclusively for emergency use, inventories held for commercial purposes, or stocks stored under bilateral agreements.

The US SPR currently contains about 415 million barrels of oil, or a little more than half its capacity. Established in the 1970s following the Arab oil embargo, the inventory is held in massive and deep underground caverns at four heavily guarded sites along the Gulf of Mexico.

Some traders and analysts doubt that consumer governments will be able to tap inventories quickly enough to fill the yawning supply gap. It might cover just a portion of the 11 million to 16 million barrels of supply from the Persian Gulf that are being lost each day.

The maximum drawdown capability of the US SPR is 4.4 million barrels a day, according to the Energy Department’s website, and it takes 13 days for SPR oil to reach the open market after a presidential decision. Trump had criticised Biden’s 2022 drawdown of 180 million barrels as reckless and politically motivated, and pledged in his inaugural address to refill the SPR right to the top (he managed to add 3,8% last year). The SPR currently sits at around 58% capacity, holding 415 million barrels, against a maximum of 714 million barrels.

There are a couple of ways these oil reserves can be released: Thye can be sold to energy companies at market rate, or, you can do what Trump is going to do: let the energy companies ‘borrow’ the oil, sell it at prevailing rates with a promise to return it – clearly, when the price drops to much more ‘palatable’ levels. This is a multi-billion dollar windfall for the oil companies. (Mr Global on TikTok breaks this down very eloquently. The grift keeps on grifting.

The IEA has previously helped implement five such interventions:

While writing this newsletter, I am acutely aware that anything said here could be out of date by Monday morning, but let’s just take stock of what has happened so far – and how quickly it could be ‘unwound’ if the war were to cease today.

Let’s look at oil. (Cobie gives another perspective on this below.) Can the conflict be wound down in a way that allows oil and other exports to start flowing through the Strait of Hormuz quite quickly? This is what matters financially, but it also provides a clear view of the motivations on either side.

President Donald Trump’s war aims have been confused and shifting, but he plainly doesn’t want a protracted interruption to oil supply (or a long war). The dopamine high of mission Epstein Epic Fury is gone, the Ayatollah replaced by one who is arguably even worse and now motivated to avenge the killing of his father, and one has to wonder if anyone in the Oval Fishbowl actually thought through the consequences.

Persistently high oil prices, one of Trump’s campaign rally cries that hit the sweet spot in mid-America, would be politically toxic and might well lose both chambers of Congress for the Republicans at the midterm elections in November. But last year’s much-discussed National Security Strategy made it a core aim that the Straits of Hormuz remain open. Easier said than done.

Shutting the Strait is bad for Iran as well, of course. But it is their critical source of leverage (rather like China’s control of rare earths in negotiations over US tariffs). They have an abundant desire not to surrender, or their regime might not survive. That means closing the Strait.

Iran’s new supreme leader, Ayatollah Mojtaba Khamenei (above), said the Strait of Hormuz should remain closed and signalled he won’t back down in the Middle East war, in his first public comments since succeeding his assassinated father. He has yet to be seen in public.

The 56-year-old hardline cleric, appointed last weekend, also said that other fronts in Iran’s conflict with the US and Israel will be opened if the fighting persists.

The stringent and defiant tone suggested once again that Iran believes it can keep firing missiles and drones across the energy-rich region, roiling markets. Its attacks so far have caused havoc in countries from Israel to Saudi Arabia and the United Arab Emirates, and led to oil and natural gas prices soaring.

We’ve also established that the Strait is even easier to close than had been thought. Insurance underwriters have determined that. Post-pandemic, we all know more about supply chains, so everyone understands the significance of Gulf nations already reaching capacity in their storage.

Markets are evidently caught in dire straits — the spike to $120 crude happened after a weekend of reports that the vulnerable passage between Iran and Oman had closed, while the brief drop as low as $80 followed a quickly withdrawn report that a US Navy ship had already escorted a ship through. This is at least strong circumstantial evidence that the issue matters above all others.

This is a problem. What is now universally known as the TACO option, Trump always “chickens out,” claims he won, and then moves on (which worked in the “contretemps” over Greenland) — isn’t available. He can declare victory, but it will only be a real win for financial markets if the Strait reopens. Iran’s increasingly assertive demands make it very unlikely they’ll do him this favour. He started this. Low-cost, decentralised drones, missiles, and intelligence networks make it far cheaper for a country to avoid defeat, even against a force as powerful as the US Navy:

Using Sun Tzu’s “The Art of War” as a guide, a clever way to defeat a stronger opponent is to make waging war far more costly for your opponent than it is for yourself. It appears that this is exactly the current situation.

The West can play for time, because it has strategic reserves put aside for just such a situation as this, but Wednesday’s news that the International Energy Authority would release 400 million barrels of oil didn’t avert a fresh rise in prices. The Hormuz obstruction is reducing supply by between 11 million and 16 million barrels a day.

If the higher estimate is correct, a back-of-the-envelope calculation shows that the released reserves can cover the gap for 25 days. For what it’s worth, the Polymarket prediction market now offers a 52% probability that war will still be going on by April 30, which is 50 days from now.

A further problem is that reopening the Strait requires an Iranian regime that wants to do so and has the strength to clamp down on rogue actors within. There is no sign of such a regime, even after the spectacular decapitation strikes that launched the offensive.

Niccolo Machiavelli’s five rules for successful regime change have yet to be completed (while the US badly wants not even to try to implement some of them):

1. Eliminate the Former Ruling Family

2. Maintain Existing Laws and Taxes (When Possible)

3. Establish Colonies Instead of Large Occupation Armies

4. Live There Personally or Maintain Close Control

5. Crush Rebellions Quickly and Decisively

A lesson from COVID and the Ukraine war is that supply chains will eventually adjust after a shock. Plans to keep trade flowing without going through the Persian bottleneck are already taking shape. But that takes time. For the next matter of months, it looks as though Hormuz will be closed, and that will hurt.

Bitcoin’s Golden Moment

Well, maybe not golden, maybe a shiny brass colour. Recent headlines have been grim for crypto enthusiasts. Bitcoin is down more than 20% year-to-date, extending a selloff that began in October. More troubling is its uncharacteristically drawn-out struggle, with investors selling into every perceived rally and pushing prices into yet another tailspin.

With the digital asset’s safe-haven credentials already under scrutiny, the Iran conflict piled further pressure on the narrative. But Bitcoin has weathered the storm, up more than 5% since the first US-Israeli missiles landed in Tehran. For context, the asset was largely unchanged during last year’s 12-day war.

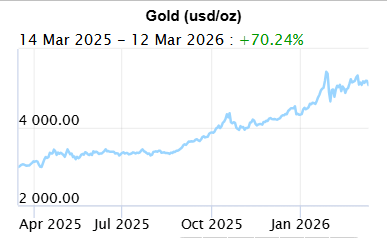

Surprisingly, Bitcoin’s distant cousin, gold — the quintessential haven asset — is down by about 2% since the war broke out. It would be far too early to conclude that there’s been safe-haven regime change, as gold is still up by nearly 20% for the year.

But Bitcoin’s curious show of strength needs to be explained. It owes its resurgence in part to support from global markets after traders rushed to buy the dip following Trump’s comments on the imminent end of the Iranian conflict. This scramble doesn’t suggest a flight to safety so much as a (probably premature) bet on an imminent easing of geopolitical tensions.

The market is a tad twitchy, which is obvious.

The close correlation of software and Bitcoin of late is interesting…

Bitcoin has traded in line with the software sector over the past five years, with the same performance, meaning $100 invested in Bitcoin or software stocks has had the same result. I find it hard to believe that Bitcoin drives the software industry; it is presumably more likely that it is the other way around. Is it causality or coincidence? As this chart above shows, their relationship has strengthened in recent months. If it holds, the ripples running through the software industry amid AI disruption fears may signal where Bitcoin goes from here. One thing is clear: Cryptocurrency is a whole new asset class, and lumping it in with others just isn’t working.

The new war in the Middle East has given fresh relevance to the legal term “force majeure.” It’s a clause buried in many contracts that lets a party off the hook in the event of an unforeseen “act of God.”

A number of oil and commodities companies have invoked the principle since the US and Israel began striking Iran, which responded with its own attacks on multiple countries. QatarEnergy, which operates the world’s largest liquefied natural gas export facility, declared force majeure so that it wouldn’t face penalties for missing contracted deliveries due to events beyond its control. Similarly, Aluminium Bahrain BSC in early March suspended deliveries of metal to some customers under force majeure clauses, citing the risks of shipping through the Strait of Hormuz, a vital waterway south of Iran that connects the Persian Gulf to the Indian Ocean.

What is force majeure? French for “superior force,” the phrase typically describes an unexpected, external event that makes it impossible for a party to fulfil its obligations under a contract. Force majeure clauses are a common feature of supply agreements and other business deals, and consumers will also find them in the fine print they agree to when they buy such things as plane tickets. Natural disasters such as earthquakes, hurricanes and floods are frequently specified as force majeure events, as was the COVID pandemic. So are human activities such as war, political unrest, terrorist attacks and labour strikes.

One of the underlying concerns, in RSA and abroad, is the impact of higher oil prices on inflation.

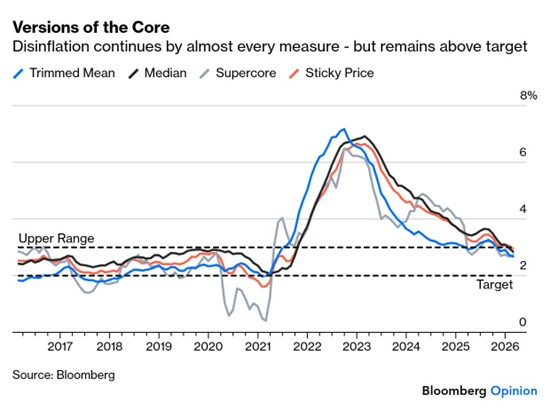

Cross-checking this with more sophisticated versions of core inflation produced by different research groups across the Fed confirms the picture.

On the face of it, the numbers continue to show that tariffs are taking a long time to turn up in prices and that inflation is returning to normal. That would make it easier for the Fed to cut rates, although it still needs to be careful not to signal that it would now settle for an effective 3% target rather than 2%.

Deeper analysis is a little beside the point, though, given what is happening in the Gulf. Inflation swaps suggest that the conflict will have a significant but not catastrophic upward effect on prices.

Officials from President Donald Trump’s administration estimated during a congressional briefing this week that the first six days of the war on Iran had cost the United States at least $11.3 billion.

That figure, from a closed-door briefing for senators on Tuesday, did not include the entire cost of the war, but was provided to lawmakers as they have clamoured for more information about the conflict.

Several congressional aides have said they expect the White House to soon submit a request to Congress for additional funding for the war. Some officials have said the request could be for $50 billion, while others have said that estimate seems low.

The administration has not provided a public assessment of the cost of the conflict or a clear idea of its expected duration. Trump said during a trip to Kentucky on Wednesday that “we won” the war but that the United States will stay in the fight to finish the job.

Administration officials have also told lawmakers that $5.6 billion of munitions were used during the first two days of strikes.

Members of Congress, who may soon have to approve additional funding for the war, have expressed concern that the conflict will deplete U.S. military stocks at a time when the defence industry is already struggling to keep up with demand.

Trump met executives from seven defence contractors last week as the Pentagon worked to replenish supplies.

Democratic lawmakers have demanded public testimony under oath from administration officials about the Republican president’s plans for the war, including how long it might last and what his plans are for Iran once the fighting has stopped.

At the end of last week, US officials leaked to the Washington Post that Russia had been giving Iran target data to strike US military assets in the Persian Gulf. These attacks have killed seven American service members and wounded more than 150 to date. They also damaged a $1.1 billion radar that’s among just six of its kind worldwide. A subsequent CNN report said Russia was also helping Iran with drone tactics learned from fighting Ukraine. Response from the White House? Crickets…

The Iranian barrage consisted mainly of roughly $40,000 Shahed attack drones, some of which US Gulf allies had to shoot down with PAC3 Patriot air defence missiles that cost $3 million to $4 million apiece. They have burned through about 800 of these high-end interceptors.

As all this was going on, Ukraine offered and then provided some of its unique, low-cost counter-drone technologies to defend the very same Gulf targets that the Kremlin was helping Tehran to hit.

And now comes the surprise: It wasn’t that Russian President Vladimir Putin helped an ally against the US, a country both see as their primary enemy; it was the response of the US president.

Donald Trump didn’t thank Ukraine or reprimand Russia, as one might expect. He dismissed any Russian sharing of target data as inconsequential. He got on the phone with Putin for a “good” chat about the war in Ukraine. And he then said he’d be lifting oil sanctions, a move that would inevitably reward Russia with fresh revenues to pursue its invasion of Ukraine.

This is so perverse that it has to raise the question of whether there is anything Putin could do that would sour Trump’s relentlessly optimistic view that he can make a friend of the Kremlin. I suspect the answer is “no.”

For no matter how random and undisciplined Trump may often be, just consider his latest flip-flopping over whether the Strait of Hormuz was open or mined, he has proved enormously consistent in his core beliefs, many of which were formed some 40 years ago. The supreme “When-We”. Among the highlights of his golden oldies: Befriending Moscow, bombing Iran, belittling NATO and making trade tariffs great again.

The impact of this back-to-the-future phenomenon is hard to exaggerate, because of the enormous military, political and economic power that Trump now has at his disposal. His playlist is forcing the world down a range of unexpected, unhealthy and potentially transformative paths.

Take Russia. Trump has been a fan of Moscow since at least 1986, when he was first courted by the Soviet Union’s then-ambassador to the US Yuri Dubinin and his daughter Natalia. They flew him to the USSR by private jet the next year, to look at the potential to build and manage two “Trump Tower” hotels in a joint venture with the Soviet tourist agency,

On his return from Moscow in 1987, he hinted at running for president and spent close to $100,000 on full-page newspaper ads that argued the US should stop letting Japan and Saudi Arabia freeride on US defence dollars. He said the same of the North Atlantic Treaty Organisation (NATO) on the TV talk show Larry King Live, soon after.

When Trump entered the White House for a second time in 2024/2025, the USSR was no more. Russia had invaded Ukraine with demands that included dismantling much of NATO. But Trump’s views remained as they’d been in the 1980s. He still saw Russia as an untapped financial opportunity that the US should court. Captain Bonespurs still believed he could resolve any impediment (in this case, a hot war) in hours. He still wanted NATO members to pay more (indeed, the case was by now stronger) and remained unconvinced of the alliance’s benefit to the US. Same rhetoric, decades on.

Trump’s views on Iran have been just as consistent.

As far back as 1980, he said in a TV interview that the US should have sent troops into Iran and taken over the nation’s oil supplies as soon as the new regime seized American hostages. In 1988, he said the US should take Kharg Island, Iran’s primary oil export terminal, the moment it next misbehaved. According to some reports, taking Kharg Island is under White House consideration/ has already been bombed again today. More than 90% of Iran’s oil is exported through this terminal. If the US were to destroy this terminal, then Iran would have zero incentive to open the Strait of Hormuz.

It would make sense for Iran to allow shipments to pass for allies and neutral parties, which includes Europe at this time. Irritatingly, only 2,5% of oil bound for the US goes through this Strait, BUT the higher price of oil will of course impact everyone, the US included.

Trump’s zero-sum views on trade also took shape in ‘80s. He complained in the same Larry King Live interview that free trade was an illusion and that the US was being ripped off. The one thing that has changed since is the identity of his main villain of global commerce. Back then it was Japan. Now it’s China.

There is value and integrity to being consistent. But having a point of view is one thing. Forming a strategy and the adaptive policy suite to achieve your goals is another. Events change things. This deeply embedded ‘nostalgia’ is one of the few consistencies we see with The Don.

Months ago, Ukraine’s President Volodymyr Zelenskiy made a PowerPoint pitch to Trump, offering to provide the US with counter-drone technology in the Gulf. White House officials told to look at it dismissed the offer as grandstanding — despite the clear need and Ukraine’s unique, demonstrated ability to deliver. Even when the US was building up Gulf air defences in preparation for war, nobody thought to call Kyiv until the Shaheds were already raining down.

This was a mistake that had high costs. It was born of prejudice against a leader who was trying to persuade Trump to take his country’s side against Russia, plus a fundamental failure to understand how the Iranian regime would react to an attack it saw as existential, and if Iran’s Thursday statement in the name of new Supreme Leader Mojtaba Khamenei is any guide, it’s digging in for a long war.

In the last 2 weeks, have you heard one consistent reason out of the White House for this war? The latest reason is ‘feelings’, and essentially, Jared’s feelings

Basically, this was something Trump had wanted to do since 1979, in revenge for Iranian attacks and slights against the US, and that he now had an opportunity he couldn’t pass up.

Trump has a consistent vision for the Middle East that’s longstanding and embodied by the Abraham Accords he negotiated during his first term. This involves the logic of the market replacing religious fanaticism, enabling Israel’s regional integration and the reintroduction of Iran and its energy-rich economy to a US-dominated global economy. It just isn’t clear that the actions he’s taking are the way to achieve it. We’re finding out in real time whether either Trump or the seven prior Oval Office occupants who made the cost-benefit analysis of going to war with Iran and decided against were right.

Author: Dawn Ridler

It’s almost cliché to write about oil now, as I am sure this is all you have heard about the whole week. On Monday last week, we saw a spike above $108 per barrel, which quickly ended when President Trump suggested that the US Navy would escort tankers through the Strait of Hormuz. For the most part, oil has stayed just shy of $100 per barrel, a number we last saw in 2022. But Iran starting to blow up oil tankers in the Gulf was a new development later in the week, causing prices to lift again. I don’t know where the price of oil is going or what the outcome of the US/Israeli war is going to be, but a few things have become clear to me as I watch all of this unfold:

US/Israeli efforts

It’s not difficult to see that they have superior firepower. Since 28 February, they have unleashed a barrage of weapons against not only the Iranians but also in Lebanon as they pound Hezbollah command centres. For the Israelis, this is a repeat of what they engaged with during the Gaza conflict. Their objective is to neutralise Iran’s influence in the region so that neighbours, in particular Israel can feel safer. This conflict has been a long time coming. For decades, there has been warnings about Iran’s nuclear capabilities and their human rights violations. All efforts at mediation have led to this point of conflict.

Iran isn’t powerless

Perhaps the reason previous US administrations have failed to engage Iran militarily is that the Persian Gulf is on their doorstep. The Strait of Hormuz is a great place to bomb oil tankers and disrupt the flow of global oil. Iran knows this matters because 20% of the world’s oil and LNG Gas flows through here. Last week, their efforts saw the end of an oil tanker near Iraq. This joins a further 8 vessels which have also been blown up. And this is where Iran has current sway. Their guerrilla efforts, driven by their armoured drones, can inflict damage, and ending them will require more than just superior firepower. To make matters worse, they are not only targeting ships but also their neighbours in an effort to maximise the amount of pain being felt all around.

Outcomes

What Iran is hoping is that they will force a negotiation where they hold the power… not the US. But what leads to this? Possibly US allies forcing them to the table as oil continues to spike higher. Oil prices going up is a real threat as countries start using their emergency stockpiles and companies adjust the prices for their goods and services higher to reflect increasing oil prices. This has now become a game of time.

The US and Israel have to neutralise Iran quickly to allow for the flow of oil again. A protracted battle will only see inflation going up globally, putting growth under pressure. Exactly what President Trump doesn’t need as he continues to the mid-term elections later this year. Their plan for now is to neutralise as many launch sites as possible and to whittle away the stockpiles of drones and missiles Iran currently owns. This could be achievable but think of the implications in the near-term future when a lone drone hits a neighbouring country, an airport or another ship… even as the US has declared victory? One could be looking at a future where lone groups in Iran launch cheap weapons to inflict damage in a war that ravages their country. This is why a negotiation or a regime change is so important. The Iranian uprising, which was seen a while ago, has gone quiet. This is strange. Surely this is now the opportunity for them to effect the lasting change that they wanted. The US is certainly hoping for this, as it would make its job so much easier. The outcome of the US & Israel not winning this war is equally dire. Russia and China are watching from the sidelines, knowing that failure would start ushering in a new world order where they would play a more dominant role. The Gulf States are also reliant on a win, as many of them have been allies of the US for many years. So failure isn’t an option, but a war that drags on for months is equally unpalatable. It’s a tough situation to be in. At the beginning of the year, I looked at the price of oil relative to the price appreciation in other commodities. Oil had not yet joined the price appreciation felt across other commodities, and I remember thinking what it would take for this to happen. That has now been answered. Commodities are turning into strategic assets, and oil has joined. Those who control and trade them have power as the world becomes more fluid.

EXCHANGE RATES and other Indices:

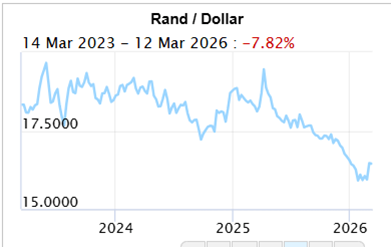

The Rand/Dollar closed at R16.89 (R16.55, R15.93, R16.01, R15.96, R16,03, R16.15, R16.10, R16.50, …R16.91, R17.13, R17.36, R17.13, R17.27, R17.31, R17.25, R17.38, R17.50, R17.22 , R17.35, R17.33, R17.37, R17.58, R17.65, R17.44, R17.61, R17.74, R18.15,R17.76, R17.72, R17.90, R17.58, R17.89, R17.99, R17.92, R17.77, R17.95, R17.88)

The Rand/Pound closed at R22.35 (R22.20, R21.48, R21.59, R21.78, R21,82, R22.11, R21.97, R22.13, …R22.57, R22.68, R22.74, R22.56, R22.69, R22.76, R22.96, R23.34, R23.37, R23.19, R23.22, R23.35, R23.55, R23.73, R23.84, R23.53, R23.84, R23.84, R24.09, R23.88, R23.76, R24.22, R24.08, R24.49, R24.22, R24.35, R24.05, R24.18)

The Rand/Euro closed the week at R19.33 (R19.23, R18.80, R18.87, R18.94, R18.93, R19.14, R19.04, R19.20, …R19.68, R19.86, R19.99, R19.96, R19.98, R20.02, R20.06, R20.26, R20.33, R 20.22, R20.30, R20.35, R20.38, R20.61, R20.62, R20.44, R20.56, R20.64, R21.04, R20.86, R20.61, R20.93, R 20.70, R20.91, R20.74, R20.68, R20.24, R20,37)

Brent Crude: Closed the week $103.14 ($92.88, $73.19, $71.76, $67.75, $68,05, $69.32, $65.88, $63.34, …$63.71, $63.19, $62.42, $63.94, $63.61 $64.66, $65.04, $61.27, $62.14, $64.28, $69.67, $66.57, $66.80, $65.52, $67.38, $67.73, $66.08, $66.07, $69.46, $68.29, $69.21, $70.58, $68.27, $67.39, $77.27, $74.38, $66.56, $62.61, $65.41)

Bitcoin closed at $70,869 ($67,310, $63,534, $68,04, $69,649, $68,553, $81,301, $89,295, $90,585, … $90,809, $86,334, $94,990, $101,562, $109.936, $112,492, $106,849, $111,888, $124,858, $109,446, $115,838, $115,770, $110,752, $108,923, $114,916, $117,371, $118,043, $113,608, $118,139, $118,214, $117,871, $108,056, $107,461, $103,455)

Articles and Blogs:

Dos and Don’ts of Wills and Estate Planning NEW

Planning your legacy, starting with your will NEW

Holiday checklist

Next year – Action Plan

Next year – Vision, Mission etc

Medical Risk Mitigation

Next Year – Consolidation

Abdication or diversification?

Carbo-loading your retirement Spoiled for choice

Who needs a plan anyway

8 questions you need to ask about retirement

What to do when interest rates drop

How to survive volatility in your investments

What to do when interest rates drop

Difficult Financial Conversations

Financial Implications of Longevity

Kick Start Your Own Retirement Plan

You matter more than your kids in retirement

To catch a falling knife

Income at retirement

2025 Budget

Apportioning blame for your financial state

Tempering fear and greed

New Year’s resolutions over? Try a Wealth Bingo Card instead.

Wills and Estate Planning (comprehensive 3 in one post)

Pre-retirement – The make-or-break moments

Some unconventional thoughts on wealth and risk management

Wealth creation is a balancing act over time

Wealth traps waiting for unsuspecting entrepreneurs

Two Pot pension system demystified

Cobie Legrange and Dawn Ridler,

Rexsolom Invest, Licensed FSP 45521.

Email: cobie@rexsolom.co.za, dawn@rexsolom.co.za

Website: rexsolom.co.za, wealthecology.co.za