Your summary with links, if you’d like to curate your content:

The market euphoria following the ceasefire announcement raises serious questions. The truce appears to enshrine Iran’s ability to charge shipping through an international waterway — something that would have been unthinkable weeks ago. Inflation expectations remain elevated, the Fed is priced for no cuts this year, and the ceasefire’s durability is far from certain. The rally reflects relief at reduced tail risk, not a return to normality. Investors should join the relief rally cautiously, pick stocks selectively, and plan for a future that is more expensive and less predictable.

Old Habits Die Hard

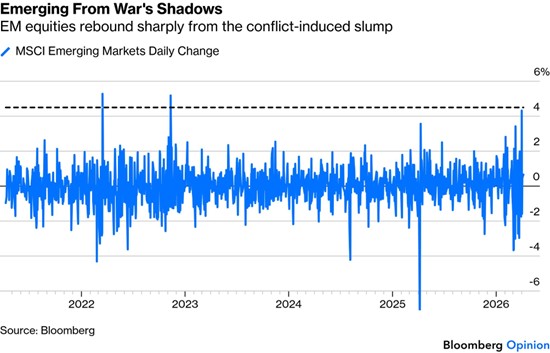

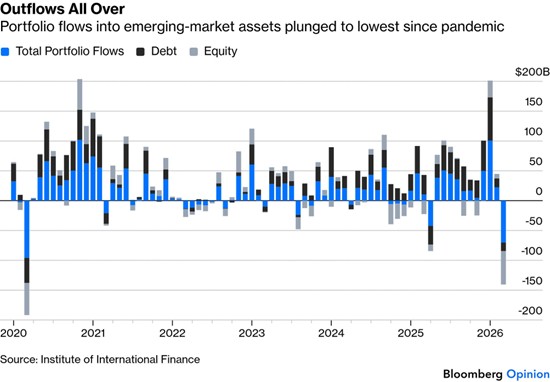

Emerging markets swung from near two-decade highs in portfolio inflows to their worst outflows since the pandemic, with EM ex-China recording roughly $60 billion in net outflows. The post-ceasefire rebound was significant, but inflation pressures are rising, the conflict isn’t fully resolved, and the Magnificent Seven’s dominance is quietly fading as the S&P 500 Equal Weighted index outperforms. A broadening of market leadership is underway, though AI spending has yet to translate into broad-based profits.

China, Sitting Quietly on the Sidelines

Beijing has turned the conflict to its strategic advantage — bolstering its image as a responsible global actor, supplying energy to strained regional neighbours, and observing US military tactics in real time. Meanwhile, the US has depleted advanced munitions and exposed weaknesses in its defence industrial capacity. The long-term implications for the balance of power in the Indo-Pacific could be considerable.

The war has already cost American taxpayers tens of billions, with the bill potentially reaching $100 billion. Beyond the financial toll, the reputational and strategic damage is severe. Iran called Trump’s bluff; his options are now limited, and the ceasefire remains fragile — with Israel continuing to bombard Beirut and the Hormuz chokepoint still closed. Reports that Iran may demand cryptocurrency payments from shipping companies for Strait of Hormuz transit rights set a dangerous precedent that could be replicated by Houthi forces at the Bab el-Mandeb.

End of Rules-Based Order and a Dent in the Dollar Too?

For the first time since the IMF began publishing data in the late 1990s, central bank gold holdings have surpassed valuation-adjusted dollar reserves. The dollar’s erosion is gradual but accelerating — driven by the weaponisation of the currency, reduced recycling of oil revenues into US Treasuries, and a growing global perception that America is no longer a reliable guarantor of stability. Global trade in dollars has fallen to around 40%, and the traditional underpinnings of the dollar system can no longer be assumed. Gold’s rise is one warning signal among many that are growing louder.

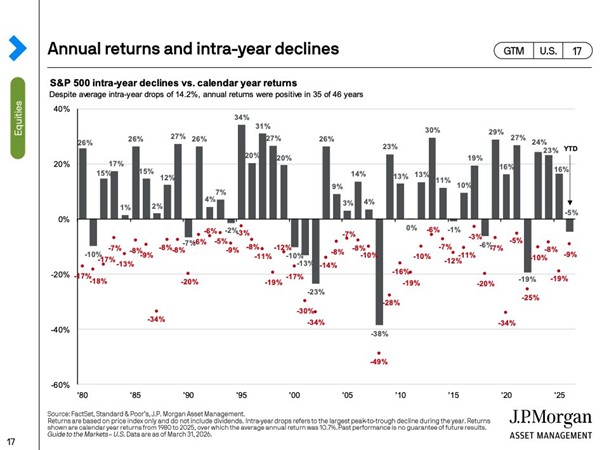

Relief Rally The JSE All Share fell 10.5% in March — effectively in crash territory — while the All Bond index dropped 6.8%, leaving investors with nowhere to hide. The rand’s depreciation ironically cushioned international portfolio holdings in ZAR terms. The ceasefire offers the US a face-saving exit from a costly miscalculation, but oil at around $100 a barrel represents a serious inflation risk and a political problem for an administration that promised prosperity to ordinary Americans. For long-term investors, history offers some comfort — the average intra-year S&P 500 drop is 14.2%, yet most years still end in positive territory. The March selloff may yet prove to be an opportunity rather than a catastrophe.

This Week’s Roundup

Commenting on the Trump/Iran War is like trying to catch lightning in a bottle, and the news can change minute to minute, let alone day to day. The sheer elation the markets displayed in response to the news of the cease-fire was perplexing – have they learned nothing of the chaotic ‘decision-making’ process of the Fifa-Peace-Prize-Winning Warmonger reigning from the Goldhouse in DC?

It’s not clear that the ceasefire in Iran is such a good deal, or whether all parties are holding to it. It seems to enshrine the principle that Iran can charge ships to use an international waterway, which would have been dismissed as unconscionable a month ago. None of this has stopped the global market euphoria.

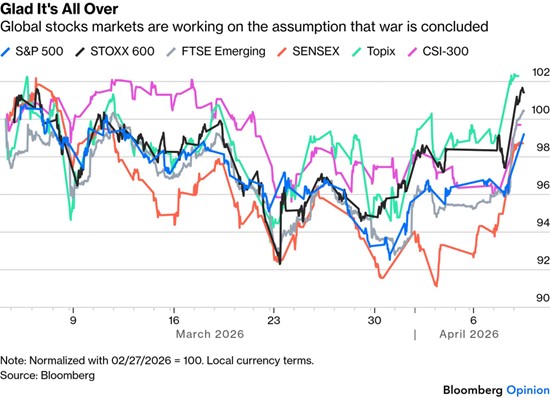

After a couple of days to ponder the ramifications of the pause in hostilities announced by President Donald Trump, it’s still regarded as a cause for celebration and for buying any risk asset that moves. Stock markets enjoyed one of their best days in years — while Asian markets opened Thursday with only minor falls.

By implication, market hopes for growth are also back on course – at least temporarily, and probably more in hope than expectation. Did the war cause a brief dip in the long-running upward trend for US stocks compared to bonds (proxied by the most popular exchange-traded funds tracking the S&P 500 and long-dated Treasuries), or is this just a brief diversion? There is absolutely no doubt that if this war carries on much longer, particularly the closure of the Strait of Hormuz, then a global recession is increasingly likely.

Countries will not just have to deal with shortages; oil producers like the US will be less affected, but inflation will be a global problem. Even countries like Saudi Arabia, where oil is nationalised, are going to feel the effects of inflation because almost everything that isn’t oil, and is produced elsewhere, is going to go up in price. They could also continue to be targeted by Iran, and if Iran focuses on desalination plants and the electricity grid, things in the Gulf could get worse.

Hopes for rate cuts from the Federal Reserve haven’t been instantly reinstated because the impact of the ongoing disruption to the supply of oil and other basic materials is still unclear. The market still expects inflation of more than 3% over the next year, and futures are priced for the Fed to take no action on rates this year. Two cuts had been fully priced before hostilities broke out.

Put this together, and the Wednesday rally is a straightforward reaction to the big reduction in what is called “left-tail risk,” meaning the worst possible outcomes are much less likely. But the rates market shows a belief that costs have increased, and will likely rise further as a result of the extremely murky compromise that has brought the ceasefire. That points to lower profit margins ahead. In previous newsletters, we have discussed the importance of earnings for future stock movements, underscoring the emphasis on profits and earnings.

Affordability is likely to be the rallying cry for the midterms.

Interest in companies that can deal with or even profit from the disruption to globalised trade, such as defence groups or anyone involved in infrastructure to reduce dependence on the Strait of Hormuz, is likely to intensify. Investors must assume that chaos, inefficiencies, and lack of transparency are not bugs but features of the system. Plan accordingly. By all means, join in the relief rally, but be prepared to have to pick stocks much more selectively in a future that is more expensive and less predictable. For now, emerging markets are the greatest beneficiaries (but who knows how long that will last).

Old Habits Die Hard

The war in Iran has made the emerging markets’ (like ours in SA Inc) stellar run to start this year feel like a lifetime ago.

Non-resident portfolio flows (tracked by the Institute of International Finance) surged to a near two-decade high, only to plunge to the lowest since the pandemic.

The degree of weakness amid a geopolitical crisis isn’t surprising, but the scale of this pullback is notable. EM excluding China recorded net outflows of about $60 billion, while debt flows also turned negative, climbing to about $14 billion for March.

What really matters to investors is a nation’s energy dependency, and the degree of its reliance on the Strait of Hormuz.

Wednesday’s post-ceasefire rebound suggests that investors still want to be in EM. The MSCI Emerging Markets index posted its largest gain since the day in November 2022 when global markets reacted to clear signs that inflation had peaked.

We still need to know the full impact of the energy shock on consumer prices — a task made harder by the fact that the war isn’t over, and that Iran seems to be establishing the principle that it can charge for tankers to cross the Strait. The direction of inflation forecasts, however, is definitely upward.

Emerging central banks’ success in tackling post-pandemic inflation shows that their tools are adequate. The major problem is getting clarity on the conflict and whether the worst is truly past, an endeavour that they have little control over. Much of what comes next lies beyond their reach, even for Washington, which helped set this war in motion alongside Israel.

Forecasts imply that the moment is still a way off when the rest of the market steps out of the shadows of AI hyperscalers and turns their heavy capital expenditures into broad-based profits.

Earnings optimism helps justify the weight of the Magnificent Seven, who account for 32.3% of the S&P 500 by value. But the narrative has shifted this year, with the Magnificents lagging and the S&P 500 Equal Weighted index outperforming. A broadening is underway, even as the tech giants continue to grow their profits at the expense of everyone else.

Is the war over? Frankly, I doubt it. I fear that Israel will do as they please, having found a US president weak enough to do their bidding and prepared to headline and fund a war they have been itching for for decades.

Companies that supply the proverbial picks and shovels for artificial intelligence (chips etc) are expected to do very well. The buyers of those goods (datacentres, LLMs), much less so. Good hyperscaler results will likely move other stocks only marginally, absent clear evidence that AI spending is translating into profits.

Regardless, the Magnificents now trade at much the same multiple as Staples. When this last happened, amid the 2022 inflation shock and in the Liberation Day selloff, it turned out to be a cue for hyperscalers’ multiples to expand again. We are living in interesting times.

China, sitting quietly on the sidelines

The US-Israel war with Iran has presented China with two golden opportunities. The conflict provides Beijing with a chance to both widen its global diplomatic sway as the “adult in the room” and to study the military tactics of its chief rival in real time.

Domestically, the conflict has been pushing up energy prices for Chinese consumers, threatening a fragile economic recovery already marked by weak demand and persistent deflation. But the war and its effect on the global energy landscape have reinforced China’s claim to be a steady global actor compared with an increasingly chaotic America. China is not only protecting itself against energy shocks stemming from the blockage of the Strait of Hormuz, but is also using its plentiful oil reserves and renewable energy resources to supply strained Southeast Asian economies.

The longer-term implications of the war for the US-China relationship may be more consequential. Donald Trump’s profligate use of a limited number of advanced munitions, the loss of key military assets, and a diminished defence industrial capacity risk further eroding US military readiness in the Indo-Pacific. At the same time, China gets to study the US military’s successes, failures and weaknesses in real time. Together, these may give China a better chance to defeat the US in any future conflict.

Educating Donald Trump and indulging his whims has been an expensive and perilous proposition for the US and the world.

His war with Iran has cost American taxpayers tens of billions of dollars since it was launched Feb. 28 and the tab seems well on its way to reaching at least $100 billion. American soldiers have died and thousands of Iranians have perished. More than 22 million people in the Middle East are estimated to live near reported military strikes. Oil and gas prices have soared. Inflation has been spurred, and economic uncertainty looms.

The reputational, civic and strategic costs for the US have also been enormous. In the run-up to a two-week ceasefire announced on Tuesday evening, the president took to social media and the airwaves to warn Iran and the world that “a whole civilization will die” and he intended to bomb the country “back to the stone ages.” He brushed off questions about whether he was willing to commit war crimes by noting that Iranians are “animals.”

Trump’s dangerous and reckless flexes in Iran may have been nothing more than bluffing, but sophisticated dealmakers know that undeliverable threats backfire when your bluff is called. Iran called Trump’s bluff. His options now are limited to trying to save face by taking an off-ramp the ceasefire offers or doubling down on an unforgiving war that isn’t likely to achieve regime change or most other practical goals.

The world can hope for the former but should brace itself for the latter. Ceasefires aren’t permanent peace pacts, and Trump is, essentially, a downed power line: easy to put back up but still dangerous.

Not a single bomb has dropped on America. Republicans like Marjorie Taylor Greene are belatedly seeing the president for who he is, and invoking a constitutional amendment (25th) that Trump’s own Cabinet and vice president are unlikely to wield, isn’t reassuring, however.

The Iran ceasefire is a recess of sorts for the world’s most powerful and incendiary schoolyard bully, and he may return to class having failed to absorb his studies.

Make no mistake, Iran is run by a vicious, oppressive theocracy that doesn’t share Trump’s predilections for short-term bursts of violent performance art. They’re willing to absorb extraordinary punishment to protect their faith and country. Trump failed to recognise that before he went to war, and may not even understand it now. His cognitive boundaries are circumscribed by wealth, celebrity, self-aggrandisement, and self-preservation and little else.

Trump remains a blinkered, close-minded leader, as well. The New York Times’ illuminating account of what led Trump to go to war in Iran, and how Israel helped speed things along, is a study of a student surrounded by largely incompetent instructors whom he really has no interest in minding anyhow. That resulted in a handful of oblivious amateurs committing the US to a bloody, seismic confrontation in a faraway land they don’t understand.

A possibly devastating escalation of the Iran war was only avoided last Tuesday evening because brighter minds successfully intervened. That effort “was dominated by allies from across Trump’s coalition warning him not to follow through on a genocidal threat to end Persian civilisation.” “Trump’s decision was a last-minute one.”

Captain Bonespurs has gone to war with the self-assurance of someone who wrangled multiple deferrals from military service during the Vietnam War, and who remains insulated from most of the consequences – economic and social – of what he has described as his “little journey” or “excursion” to Iran.

The ceasefire’s breathing room hasn’t fully extricated Trump from the quagmire he created in Iran. A serious student would try to learn from that tough lesson, grow and move on. But a Trump cornered and left without his preferred options can become even more dangerous and thuggish.

The ceasefire deal in the six-week US-Iran conflict remained in doubt by late week, as Israel intensified its bombardment of Beirut, Tehran kept the Hormuz chokepoint closed, and negotiators prepared to meet again even as both sides declared victory.

With the Hormuz chokepoint now in continued focus, reports have circulated that Iran may demand cryptocurrency payments from shipping companies for oil tankers transiting this critical waterway.

Imposing tolls at the maritime chokepoint would set a dangerous precedent and break with established international maritime norms.

Such a precedent would almost certainly not go unnoticed by Iran-aligned Houthis in Yemen, who already have a history of launching missiles and low-cost, one-way attack drones at vessels transiting the Bab el-Mandeb chokepoint between Yemen and the Horn of Africa.

Any copycat tolling regime there would only deepen maritime bottlenecks and compound the risks for global shipping.

End of rules-based order and dent in the dollar too?

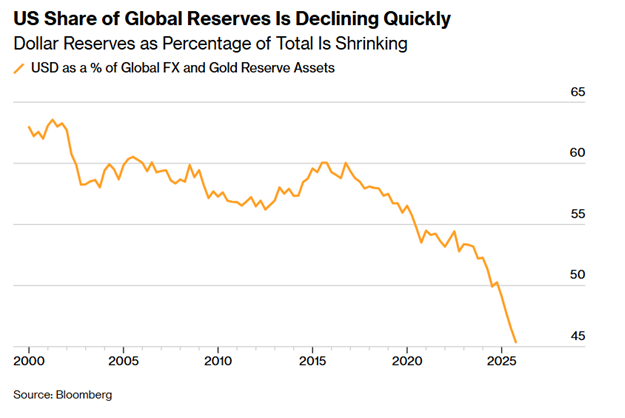

The US’s war with Iran has put a potentially irreversible strain on the global trading system, with gold reserves having eclipsed central bank holdings of valuation-adjusted dollar assets for the first time in several decades. It’s very early days after the announcement of a ceasefire between the US and Iran, yet even if it holds, the conflict is likely to have created lasting effects on the dollar system as President Donald Trump appears to rip up the rules-based order in place since World War II.

The dollar’s demise has been greatly exaggerated on many previous occasions. But it will not be a dramatic point-in-time event. Sterling’s fading as a reserve currency was punctuated by several milestones over an extended period — the end of World War I, coming off the Gold Standard, Bretton Woods and the Suez crisis.

After the increasing weaponisation of the dollar, culminating in the seizure of Russian assets in the wake of the war in Ukraine, and the mooting of a Mar-a-Lago accord, the US currency has just passed another milestone in its declining dominance.

Dollar-denominated reserves – i.e., central bank holdings – adjusted for valuation effects, are now lower than gold reserves for the first time since the International Monetary Fund started publishing the data in the late 1990s.

Holdings of central banks could simply be passively benefiting from the metal’s historic rise in recent years. But if we consider the adjusted value of dollar reserves as the currency’s “weight,” then it has fallen 15% since official holdings of the US currency peaked around 2014. Whereas (almost exclusively emerging markets) central banks have increased their physical holdings of bullion, in tons, by 15%. It’s thus hard to refute that the actual demand for dollars has been materially softening.

Until the seizure of Russia’s assets, Central Banks were opportunistic traders of dollars, buying them when the currency fell, and selling them after it had rallied. No longer. The decline in the dollar exchange rate in recent years has not been met by meaningful purchases.

Pressures on the dollar system are also coming from higher energy prices and ongoing supply constraints. Oil and gas prices are significantly lower after the ceasefire announcement, but are still much higher than they were before the war. That is putting increased strain on energy importers to raise dollars by liquidating assets.

Further, energy exporters unable to sell their product have been facing their own cash flow pressures. Together, these dynamics led to gold and Treasuries rallying when tensions eased and vice versa.

However, there’s a much deeper and long-lasting issue. The quid pro quo that forms the backbone of the global monetary system — that trade proceeds are recycled into dollar assets, allowing the US to fund cheaply, in return for security guarantees and the stability of the global system — can no longer be taken as read.

Normally, we would expect that as the Strait of Hormuz is fully reopened, dollars should eventually flow back to oil exporters, who in turn should buy Treasuries or other US assets. Similarly, as oil prices normalise and importers get back on their feet, they’ll eventually have surplus dollars to reinvest in the US.

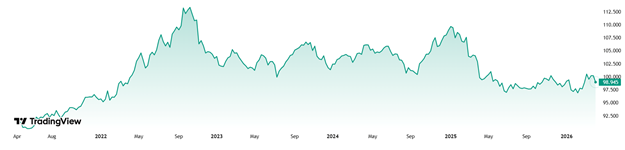

That can no longer be assumed, though. If you have a look at the DXY chart below, there has not been a significant strengthening of the dollar that one might have expected during the last few weeks, in fact it has started to fall again.

Chart: DXY

First, Middle Eastern exporters such as Saudi Arabia have less excess savings to recycle as their economies diversify and invest more domestically.

But it’s more critical than that. If the US is no longer seen as a reliable guarantor of stability and security, then there is a diminishing incentive to trade in dollars and recycle them back into the US. The dollar carousel that has underpinned the global monetary system is coming under increasingly grave strain.

As stated, this is not an overnight phenomenon. A current lack of alternative reserve and financing assets ensures that, but that doesn’t mean there isn’t a puncture and the air won’t continue to escape.

Gold’s ascendancy is but one warning, but others are getting louder. Global trade in dollars has fallen to around 40% in the last few years while that in euros and the yuan has picked up; dollar-denominated international loans have slipped back to 60% of the global total; central bank holdings of Treasuries are now less than their holdings of gold; and the dollar as a share of global FX and gold central bank holdings is falling rapidly.

Common knowledge is often what it takes to upset accepted norms and overturn ingrained thinking patterns. After the unilateral actions of the US in the Iran war, everyone knows the rules of the game have changed. Owning fewer dollar assets becomes increasingly logical. Now that is common knowledge; it’s hard not to see the dollar’s dominance continuing to ebb away over time, and gold’s fortunes further revived.

Author: Dawn Ridler

The war that gave America nothing politically but showed its military might has hit a pause. The fragile 2-week ceasefire for negotiations is really a way for the US to extract itself from a fiasco which will go down in the history books, but talks in Pakistan are not going the US’s way. It showed how military might has now become less effective against an opponent which can fight with drones and a stranglehold on the world economy by controlling energy flows through the Strait of Hormuz. A serious miscalculation by the Americans sent world markets sharply lower in March.

I would contest that the JSE All Share probably was in crash mode after it finished the month, 10.5% lower as compared to the MSCI ACWI, which ended 0.7% higher in ZAR terms (-6.3% in $). The local pain wasn’t isolated to equities; it was also evident in bonds, as the All Bond index ended the month -6.8% lower. There was really no place to hide during the month showing again that during a crisis the negative correlation between equities and bonds don’t traditionally hold.

The Rand’s depreciation against the Dollar during the month was due to international investors seeking safety and pushing the value of the Dollar higher. Ironically, this is what caused the MSCI ACWI to end 0.7% higher in ZAR terms, allowing for the portfolio’s international holdings, when measured in ZAR, to hold its own.

It is in the US’s interest to bring this war to an abrupt end and to make concessions which they would not have ordinarily made during peace negotiations. And this is the travesty for them, having created this mess. The US administration doesn’t have the public’s consent for a protracted war, which makes a ground invasion most unlikely.

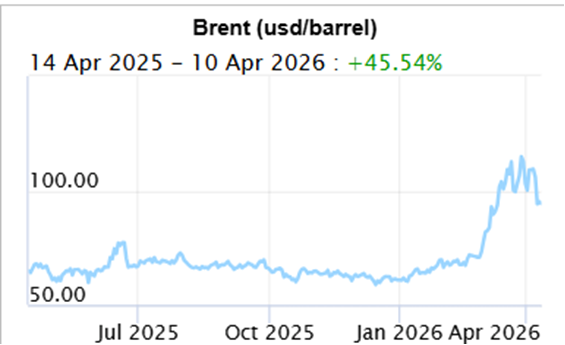

I would argue that the US is more isolated today than it ever was before, thus making its political aims anywhere else in the world so much more difficult to achieve. And then they may very well have caused a spike in inflation, as oil prices are now trading at $100 a barrel, a far cry from $60 before. This is not the winning hand that they are normally accustomed to playing. Inflation is important in the US. Part of the election promises was that they would kick-start the US economy for the average American. These are people who rely on job security, low mortgage rates and rising GDP, which they can share in.

Higher inflation makes achieving this much more difficult. Rising bond yields are showing that inflation may very well tick higher, thus making it more difficult to lower interest rates. A serious political blow for the trump administration.

The stakes are high for the US, and “making a deal” has never been more important. Ultimately, the US needs a cheaper Dollar and lower interest rates. This will allow them to deal with their ever-ballooning debt issues, which are even worse now after the war. This allows for long term allocators of capital to focus on the sell down in March not as an Armageddon moment but an opportunity to readjust and allocate capital where they deem fit. The chart below from JP Morgan Asset Management is telling:

It shows the annual returns for the S&P 500 (grey bars) against the intrayear drops that investors would have experienced in a given year. Interestingly, the average intra-year drop experienced is -14.2%. Despite this, the S&P 500 ends most years still in positive territory.

Will this be such a year? No one knows, but the good news for long-term investors is that if this year proves to be negative, the next year will make up for this again. This is the beauty of long-term investing.

Author: Cobie Le Grange

EXCHANGE RATES and other Indices:

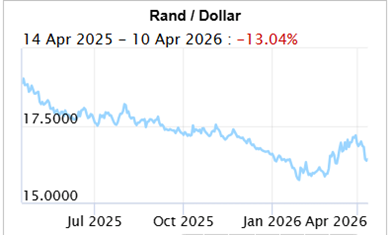

The Rand/Dollar closed at R16.41 (R17.07, R17.06, R16.89, R16.55, R15.93, R16.01, R15.96, R16,03, R16.15, R16.10, R16.50, …R16.91, R17.13, R17.36, R17.13, R17.27, R17.31, R17.25, R17.38, R17.50, R17.22 , R17.35, R17.33, R17.37, R17.58, R17.65, R17.44, R17.61, R17.74, R18.15,R17.76, R17.72, R17.90, R17.58, R17.89, R17.99, R17.92, R17.77, R17.95, R17.88)

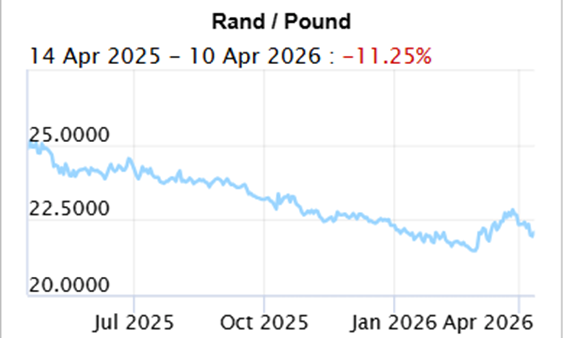

The Rand/Pound closed at R22.09( R22.77, R22.76, R22.35, R22.20, R21.48, R21.59, R21.78, R21,82, R22.11, R21.97, R22.13, …R22.57, R22.68, R22.74, R22.56, R22.69, R22.76, R22.96, R23.34, R23.37, R23.19, R23.22, R23.35, R23.55, R23.73, R23.84, R23.53, R23.84, R23.84, R24.09, R23.88, R23.76, R24.22, R24.08, R24.49, R24.22, R24.35, R24.05, R24.18)

The Rand/Euro closed the week at R19.24 (R19.70, R19.77, R19.33, R19.23, R18.80, R18.87, R18.94, R18.93, R19.14, R19.04, R19.20, …R19.68, R19.86, R19.99, R19.96, R19.98, R20.02, R20.06, R20.26, R20.33, R 20.22, R20.30, R20.35, R20.38, R20.61, R20.62, R20.44, R20.56, R20.64, R21.04, R20.86, R20.61, R20.93, R 20.70, R20.91, R20.74, R20.68, R20.24, R20,37)

Brent Crude: Closed the week $95.20 ($107.88, $112.36, $103.14, $92.88, $73.19, $71.76, $67.75, $68,05, $69.32, $65.88, $63.34, …$63.71, $63.19, $62.42, $63.94, $63.61 $64.66, $65.04, $61.27, $62.14, $64.28, $69.67, $66.57, $66.80, $65.52, $67.38, $67.73, $66.08, $66.07, $69.46, $68.29, $69.21, $70.58, $68.27, $67.39, $77.27, $74.38, $66.56, $62.61, $65.41)

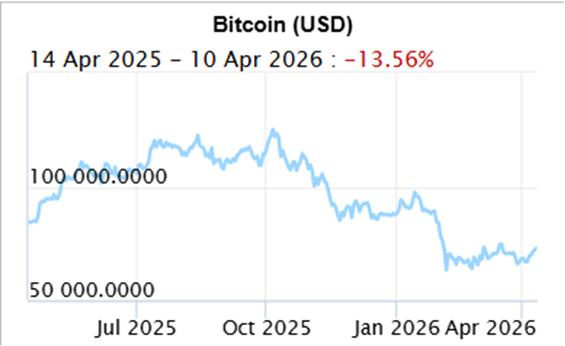

Bitcoin closed at $70,904 ($68,691 , $68,586, $70,869, $67,310, $63,534, $68,04, $69,649, $68,553, $81,301, $89,295, $90,585, … $90,809, $86,334, $94,990, $101,562, $109.936, $112,492, $106,849, $111,888, $124,858, $109,446, $115,838, $115,770, $110,752, $108,923, $114,916, $117,371, $118,043, $113,608, $118,139, $118,214, $117,871, $108,056, $107,461, $103,455)

Articles and Blogs:

Dos and Don’ts of Wills and Estate Planning NEW

Planning your legacy, starting with your will NEW

Holiday checklist

Next year – Action Plan

Next year – Vision, Mission etc

Medical Risk Mitigation

Next Year – Consolidation

Abdication or diversification?

Carbo-loading your retirement Spoiled for choice

Who needs a plan anyway

8 questions you need to ask about retirement

What to do when interest rates drop

How to survive volatility in your investments

What to do when interest rates drop

Difficult Financial Conversations

Financial Implications of Longevity

Kick Start Your Own Retirement Plan

You matter more than your kids in retirement

To catch a falling knife

Income at retirement

2025 Budget

Apportioning blame for your financial state

Tempering fear and greed

New Year’s resolutions over? Try a Wealth Bingo Card instead.

Wills and Estate Planning (comprehensive 3 in one post)

Pre-retirement – The make-or-break moments

Some unconventional thoughts on wealth and risk management

Wealth creation is a balancing act over time

Wealth traps waiting for unsuspecting entrepreneurs

Two Pot pension system demystified

Cobie Legrange and Dawn Ridler,

Rexsolom Invest, Licensed FSP 45521.

Email: cobie@rexsolom.co.za, dawn@rexsolom.co.za

Website: rexsolom.co.za, wealthecology.co.za