I was covering for Michael Avery on his Classic Business show last week, and had some very interesting interviews. I can recommend listening to my chat with Simon Brown on ETFs.

Your summary with links, if you’d like to curate your content:

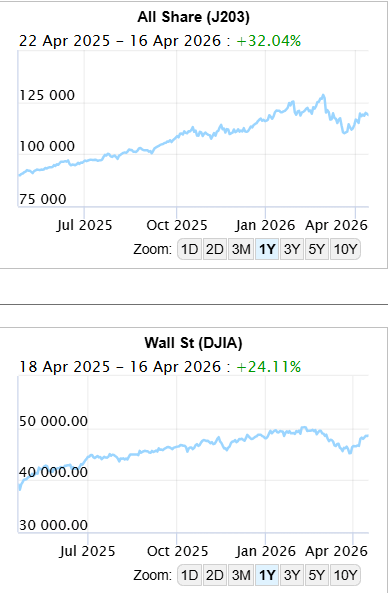

All-Time Highs Are Here Again!

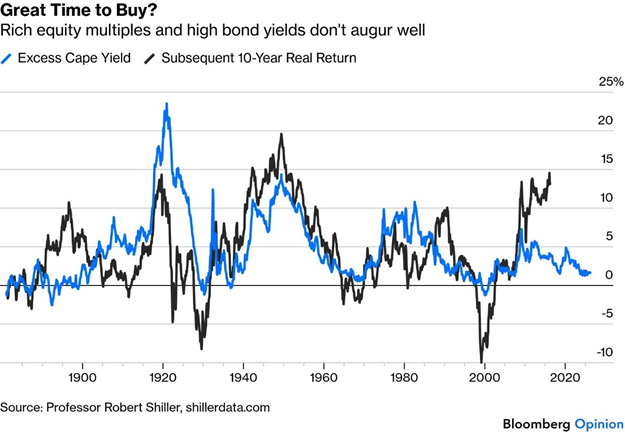

The S&P 500 and Nasdaq 100 surged 10.7% and 14.2%, respectively, since March 30 — a historically rare and fast rally. Valuations look stretched by any measure, with the excess CAPE yield signalling poor long-run returns. The move bears an uncomfortable resemblance to March 2000, just before the dot-com bubble burst. FOMO and the learned “buy the dip” reflex from last year’s Liberation Day appear to be the primary drivers rather than fundamentals.

Fertiliser is almost a bigger problem than oil in this crisis

Persian Gulf nations supply at least 30% of global fertiliser. The Hormuz blockade has sent fertiliser prices to extreme levels, threatening a lagged but serious food inflation shock — potentially worse than the Ukraine disruption — with lower crop yields possible if planting seasons are missed.

The political assault on the Fed continues, with Justice Department officials visiting Fed premises over a dubious probe into Powell. Powell’s term ends May 15; Kevin Warsh’s confirmation is being blocked by Senator Tillis. Markets are largely unmoved, pricing in no rate change at the June FOMC meeting and banking on Trump backing down from firing Powell.

US military and economic influence is seen as declining as warfare shifts to AI, drones, and cyber domains. Allies are increasingly unsettled, building parallel institutions and diversifying away from dollar-based assets at the margins. Europe is positioning itself as a stability anchor, and China may benefit by default if the US continues blurring the line between market economy and command system.

The Iran war has driven aluminium up ~15%, with JPMorgan warning of a supply “black hole” after Iranian strikes targeted key smelters in Abu Dhabi and Bahrain. South Africa’s Hillside smelter at Richards Bay, the southern hemisphere’s largest, stands to benefit from elevated prices, though South Africa effectively subsidises it through discounted Eskom power until 2031.

Why did loadshedding suddenly end

South Africa has had nearly two years without formal loadshedding, thanks to better Eskom plant performance, reduced unplanned outages, growing IPP and embedded renewable capacity, and smarter grid management. The Energy Availability Factor has climbed into the mid-60% range, and Eskom now holds a healthy reserve margin. Structural problems remain, however, and a return of loadshedding cannot be ruled out.

The Price of a War Shock, but AI motors on

Despite geopolitical turbulence, US markets remain central to global capital flows, reinforced by the AI revolution concentrated in American tech. Meanwhile, trust in US institutions is quietly eroding, allies are hedging, the ECB is building alternatives, and China sees opportunity in American unpredictability. The key risk isn’t dollar collapse, but a gradual rise in the cost of capital for the US.

Remembering Mark Mobius Mark Mobius, the legendary “Indiana Jones of emerging markets” who led Franklin Templeton’s emerging markets operation for over three decades under Sir John Templeton, passed away last week in Singapore at 89. His career proved that patience through volatility, concentrated conviction, and long-term compounding in high-growth economies can deliver exceptional returns.

This Week’s Roundup

All-Time Highs Are Here Again!

The S&P 500 and Nasdaq 100 are back at all-time highs — in the latter’s case, the first in six months. Even with the flow of oil through one of the world’s most important arteries at a standstill, it’s been an astonishing bounce.

Since the close on March 30, the S&P and Nasdaq are up 10.7% and 14.2% respectively, rewarding the patient investor. Since 1950, this is only the 21st time that the S&P has managed a 10% rally this fast.

Stocks look expensive by any sensible measure, while the 10-year Treasury yield sits at 4.3%, higher than at any point during the 13-year rally that followed the Global Financial Crisis. Subtract the bond yield from the earnings yield (the inverse of the price/earnings ratio) of the S&P and you get the “excess CAPE yield”.

CAPE itself is the cyclically adjusted price-to-earnings ratio, based on price divided by the average of about 10 years of inflation-adjusted earnings. The CAPE yield flips that ratio around into a yield format, which makes it easier to compare with other yields like government bonds.

The CAPE yield is the earnings yield version of the CAPE ratio: it is usually calculated as 1÷”CAPE” , so a higher CAPE yield means a lower CAPE valuation and vice versa. In practice, many investors use it as a rough estimate of long-run expected real equity return, while “excess CAPE yield” compares that yield with bond yields

For over a century, this offered a great guide to how equities would fare over the ensuing decade, and it currently suggests that this is an unappealing time to buy into the market.

Earnings season is getting underway amid great optimism. That limits potential damage from the war, but can’t explain this two-week rally.

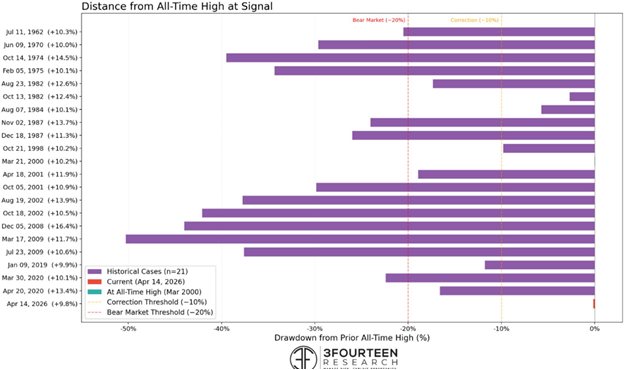

Rallies this violent usually happen only when markets are seriously beaten down and far from record highs. This time, the S&P never fell 10% from its peak. It’s quite unlike any preceding swift rally, with the exception of the chaotic fortnight in March 2000 when the dot-com bubble was about to burst. That was also the only previous 10-day, 10% rally when stocks were more expensive in terms of earnings multiples than they are now. The other rallies are listed in this chart below. Typically, they come at the end of drawn-out bear markets (in 1974 and 1975 or 1982), or after major crises like the GFC in 2009, Long-Term Capital Management in 1998 or Covid in 2020:

The conclusion that this rally is most like March 2000, when the biggest speculative bubble in US history was about to burst. Coincidence?

This rally probably wouldn’t have unfolded as it did without the experience of Liberation Day last year, when stocks sold much harder than they did last month and then started a big rally as soon as the president announced his first “TACO” (Trump Always Chickens Out) by postponing his tariffs. Many missed out. That made traders more reluctant this time to sell, even though the Iran crisis was arguably more threatening than a trade war. They were primed to buy at the first hint of a TACO. Bottom line, this was FOMO at its finest.

The March 31 pivot occurred on the slim evidence that Iran’s president said he was “ready to end the war” but needed concessions first. Fear of missing out drove a rally at this first hint of an end to hostilities.

Market structure has changed since earlier rebounds. Those programmed to buy the dip, drag static and momentum investors with them, leaving traditional rational investors to watch in wonder. The fundamentals-driven investors, or at least those who were still in business, were about to enjoy a big triumph in March 2000. This story is still being written.

Fertiliser is almost a bigger problem than oil in this crisis.

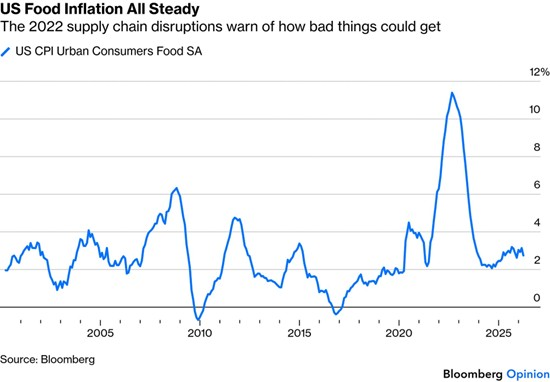

Oil dominates the affordability debate for good reason; the truest measure of the war’s disruption is food. Fertiliser from the Persian Gulf region accounts for at least 30% of the global supply. The effect of the Strait of Hormuz blockade will only be visible months from now, at harvest time.

The conflict has already driven fertiliser prices to astronomical levels. Over the past three years, Gulf countries have emerged as the largest regional exporters of urea and ammonia, both nitrogen-based fertilisers, and the second-largest exporters of diammonium phosphate. Liquefied natural gas is a key input for fertiliser production in countries with limited domestic gas, like India, Pakistan, Bangladesh and Turkey.

This will impact food prices, but with a lag.

Yet given the tight link between fertiliser costs and food inflation, it’s only a matter of time before the effects become visible, perhaps long after the conflict. In a long war, ironically, the best-case outcome may be higher food prices. The alternative would be missed fertiliser-application seasons leading to lower crop yields, and thus even higher prices down the road, plus a broader threat to global food security.

Are these fears warranted? The disruption after Russia’s invasion of Ukraine, another major agricultural hub, and the subsequent closure of the Black Sea offer ample evidence of what could happen.

Pandemic restrictions were only beginning to ease when Ukraine was invaded, while wider inflationary pressures were driving up prices. These exacerbated the effect on food prices. Today’s macro backdrop is healthier, but the nature of the disruption is uncomfortably familiar and the memories of its political consequences are fresh:

The US is likely provide only temporary relief to its farmers. That’s a Band-Aid. And in fact, that could come back to bite even harder, just simply due to inflation and the negative effects of that. The US government needs to take a much more focused approach to building out the country’s technological infrastructure, which will allow it to be more self-sustaining and economically efficient in its farming.

Meanwhile, the Bloomberg Agricultural Commodities Index suggest prices remained fairly contained relative to the Ukraine-related disruptions:

These attacks on the FED are getting tiresome. There is no longer a prospect of wholesale change in the Federal Reserve’s leadership in a Trumpian direction, as the regional governors have been reconfirmed in their posts for another five years. It should be time to put the issue of Fed independence on the back burner.

But we can’t. Trump wont let us.

Justice Department officials have made an unannounced visit to the Fed in pursuit of their flailing probe against Chairman Jerome Powell over building renovation overruns, and also fighting in court, despite a ruling that the case was spurious, for the right to continue it.

Until the legal proceedings end, Republican Senator Thom Tillis has promised to block Kevin Warsh’s nomination to succeed Powell when his term ends May 15. More and more Trump supporters and Influencers are distancing themselves from MAGA and Trump.

Powell has said he’ll stay as chairman if Warsh isn’t confirmed on time, and won’t resign from his remaining two years on the governing board until the prosecution ends. Trump says he’ll fire Powell as chairman if he tries to stay, and a Justice memo from 1979 suggests he has the right to do so.

This hideous mess is not over. But it hasn’t stopped a stock market rally that’s beginning to look historic. Why?

There are two main reasons. First, the war has made the Fed’s finer judgments irrelevant for now. They won’t be moving rates until there’s clarity on the extent of the price shock. Interestingly, even Treasury Secretary Scott Bessent appears to accept this, while the latest Beige Book, a collection of anecdotal evidence from the Fed’s regional branches, suggests an economy in suspense, with no call to move rates.

Whether or not Warsh chairs the Federal Open Market Committee meeting in June, the almost universal expectation now is that rates won’t change, and perhaps that the White House won’t press hard for a cut.

Second, there’s an ongoing belief that even though the Justice Department has to try to satisfy the president’s desire for revenge, these attempts aren’t going anywhere. Powell is expected to leave as a governor by year-end. Polymarket bettors still put a 60% chance on his hanging around for a while until the end of next month, but that’s more an expression of the belief that the Senate won’t have confirmed Warsh by then.

The president might just go through with his threat to fire Powell in May under these circumstances, and elevate a temporary chairman, possibly the ultra-dovish governor Stephen Miran. It could create a mess. For that reason, markets are working on the assumption that Trump won’t do it. The situation is unnecessary and undignified. The chances remain that it won’t cause too much damage.

There is no doubt that US military effectiveness is declining despite technological capability due to modern warfare’s shift to economic, AI, drone, and cyber domains. The US is no longer positioned as a global policeman or democracy upholder. It’s projected that the US will exert reduced economic and military presence globally within 20 years as other countries fill the void. European allies “stupefied” by Greenland acquisition discussions, questioning American commitment to democracy and freedom.

Trump Administration Messaging Challenges are feeding into this changing narrative. Attacks on Pope alienating 20% of US adults who identify as Catholic heading into midterm elections. There is a strained relationship with the UK (Trump vs Starmer) despite King’s upcoming visit. Social media communication style is replacing refined governmental messaging.

Different global audiences are interpreting US actions differently based on geographic location and cultural context.

War threatens to push up global inflation, complicating Federal Reserve policy. Administration needs an “off-ramp” urgently to prevent inflation from ticking up again. Powell’s 2024 decision not to drop interest rates now appears prescient given current instability.

The Trump administration is seeking to fire Powell before the May 15th term end, requiring proof of “gross irregularity”. Lisa Cook firing precedent at the Supreme Court level may inform the Powell situation.

Kevin Walsh is awaiting confirmation as Powell’s replacement; the narrative is already shifting from expected rate cuts to stability. US debt refinancing needs are driving pressure for favourable interest rates. Walsh may face “the shortest Fed tenure in history” if he resists political pressure.

At this point, Scott Bessent is best characterised as a “Trump sycophant” whose messaging is indistinguishable from the president. Midterm election outlook challenging for Republicans, given multiple controversies. Double messaging creates confusion: starting wars while needing low inflation for debt refinancing. Clearly, this foray was not well thought out.

South Africa’s primary aluminium‑smelting history centres on one large, integrated project: Hillside Aluminium at Richards Bay, which has been the country’s only major primary smelter since the 1990s. Smelting is still relatively small in the broader South African industrial landscape, but it plays a key role because aluminium is heavily dependent on cheap electricity and export‑oriented industry.

The first real aluminium presence in South Africa dates to the 1940s, when Aluminium Limited of Canada (Alcan) set up a sales office, then the Aluminium Company of South Africa, and built a rolling mill in Pietermaritzburg.

Primary aluminium smelting in South Africa began in 1971 with Alusaf (later part of BHP Billiton and then South32 – Australia) at Richards Bay. The plant started relatively small, but by the mid‑1990s it had expanded into the Hillside Aluminium smelter, which became the largest primary smelter in the southern hemisphere and South Africa’s only major reduction plant.

Hillside consumes about 5–6% of Eskom’s total sales (around 10 TWh/year) and can be interrupted briefly to help balance the grid. Recent analyses show that Hillside’s discount alone could effectively subsidise electricity for roughly 700,000 households in a year, illustrating the scale of the cross-subsidy. Infuriatingly, this agreement was rolled over in 2021, so it has until 2031 before it can be revisited.

Hillside as the backbone of RSA smelting (but it’s not ‘ours’, we just provide the subsidised electricity- effectively).

Hillside does supply both domestic fabricators (such as Hulamin) and export markets, especially in Europe, Asia, and the Middle East. Obviously the recent price rise is a nice little windfall.

Industrial metals jumped to a record high on the London Metal Exchange, driven by gains in aluminium after the Middle East war disrupted supplies, as well as a recent revival in copper.

The LME Index, which tracks six major metals, has rallied by almost 12% over the past four weeks and reached an all-time high on Thursday’s close. Aluminium has risen about 15% since the start of the Iran war, with around 9% of global output coming from the Middle East.

Aluminium has the biggest weighting on the LME gauge and, together with copper, the two metals make up almost three-quarters of the index.

JPMorgan Chase & Co. has warned the aluminium industry was heading toward a “black hole” as a serious, prolonged supply deficit is hitting the market after supply losses escalated dramatically in the wake of Iranian strikes directly targeting two key smelters in Abu Dhabi and Bahrain at the end of last month. A double blockade of the Strait of Hormuz — by the US and Iran – is also keeping shipments stranded.

But while the waterway remains closed, hopes that a ceasefire between the US and Iran will be extended and signs that the two sides may be moving closer to a peace deal have aided other metals. They were hit by soaring energy costs and fears of slowing global growth due to the war, but have recovered in recent weeks on signs the conflict might be winding down.

Graph: Price of Aluminium.

President Donald Trump claimed last Thursday, without evidence, that Iran had agreed to terms it has long resisted, including giving up ambitions for a nuclear weapon. Tehran hasn’t confirmed it’s made concessions. This story can move quickly, and by the time you read this, of course, it could be completely out of date.

Traders are building back positions in base metals and front-running the move, even though the Iran war has yet to be resolved. They also like to trade on the certainty of aluminium supply disruptions.”

Copper could surpass a record high hit in January. Chinese buyers coming back to the market and a looming decision on tariffs from the White House are encouraging more shipments to the US. Copper has rallied 11% in the last four weeks, and is around 3% off its all-time closing price peak.

The LMEX Metals Index was up 3.6% this week through Thursday. Most metals were down on Friday.

Why did loadshedding suddenly end

South Africa has gone nearly 2 years without formal Eskom load shedding, mainly because its power system has temporarily improved enough to meet demand without cutting supply. That doesn’t mean the structural problems are solved, just that several factors have aligned to keep the lights on for now.

Eskom has seen better plant performance and fewer sudden breakdowns at some coal stations. There has been more disciplined maintenance and fewer forced outages, which raises the amount of power actually available on the grid. There has also been some recovery of capacity at troubled stations like Medupi and Kusile, though they still run below design capacity.

Private and municipal generators have ramped up. Independent power producer (IPP) projects, especially renewables and gas, are adding hundreds of megawatts that previously weren’t available. Municipal and embedded generation (solar, diesel, etc.) has reduced the strain on Eskom during peak hours, shrinking the “gap” that normally triggers loadshedding

Economic growth has been patchy, so some demand growth has slowed compared with earlier years. Households and businesses have adapted (e.g., solar battery systems, shifting usage), which softens the evening peak that historically overloaded the system.

Eskom and the system operator have improved short-term scheduling and “energy only” purchases, using emergency diesel and gas units more strategically. No major simultaneous wave of breakdowns or coal supply shocks has hit the fleet in recent months, keeping the grid further from the edge.

Why it can still return…

The underlying causes are still with us:

Aging coal fleet, maintenance backlogs, and fuel supply issues remain. Generation capacity is still not keeping up with long-term demand growth, so experts expect load shedding to recur unless reforms and new build pace up.

Why did it change so quickly?

Mainly because Eskom’s Generation Recovery Plan started producing measurable results over the past 12–18 months, not because the underlying problems vanished overnight. The shift from frequent load shedding to many months without it reflects a confluence of better plant performance, less unplanned breakdowns, and improved system management.

By late 2025 and early 2026, its Energy Availability Factor (EAF) had climbed into the mid 60% range—roughly 5 percentage points higher than the previous year—meaning markedly more power was actually available. Unplanned capacity loss (breakdowns) fell sharply; Eskom reports that unplanned outages in 2026 are thousands of megawatts lower than the same period last year. The Unplanned Capacity Loss Factor (UCLF) dropped from around 29–30% to about 20–21%, effectively shrinking the daily “gap” that used to trigger load shedding.

There is also More reserve margin and less diesel dependence. Eskom now frequently has 26–29 GW of available capacity against a peak demand forecast of around 22–24 GW, giving a healthy reserve margin where before it was often negative. Diesel-based open-cycle gas turbines are being used far less because the coal fleet is more reliable, which both saves money and stabilises the grid.

Eskom is rolling out hundreds of thousands of smart meters and removing load reduction (targeted cuts) from many feeders, which reduces the need for formal Eskom-level load shedding. This means some areas that used to be “quietly” switched off are now on stable supply, improving the perception and reality of uninterrupted power. In short, the change feels fast because several levers (repairs, maintenance, smart metering and extra IPP capacity) all clicked into place over a year or so, whereas before they were all misfiring at once and causing constant outages.

The Price of a War Shock, but AI motors on.

In global finance, trust is not solely about virtue; it’s also about scale, liquidity and opportunity. Investors who may question America’s politics can’t ignore its markets.

Although a recent Treasury auction of two-year notes unexpectedly drew weak demand (a mark of concern about a potentially protracted war), US government securities remain the world’s deepest, safest asset pool. The AI revolution—real, capital-intensive and concentrated in the US and its tech companies—is reinforcing US economic centrality, even as it destabilises everything else.

A short window of time (years, not decades) may determine not only America’s place in the world but also the course of AI.

Europe has produced hundreds of pages of AI regulation; it’s almost too much to be of any real use. In Washington, policy is erratic, including chip deals, AI use in military operations and a public fight between the Pentagon and leading AI lab Anthropic over how the technology can and should be used in warfare. A new White House framework for AI regulation focuses on power costs, safeguards for children and preventing states from making their own rules.

Meanwhile, executives and workers alike sense an existential threat from AI. The level of alarm in boardrooms and living rooms is not remotely matched by what is on the table in Washington.

Some policymakers see the rise of AI as less of a job-eater than globalisation was. AI is a tool. It’s not going to replace us as human beings, Christopher Waller, a Fed governor, said in a February speech.

What industries are trying to figure out about AI is whether it causes labour reduction versus labour shifting, he said. Other observers are bracing for a different kind of pain.

“We’re going to have a lot of societal stress” over the coming years, Reed Hastings, the co-founder of Netflix Inc., said, “The rate of change in society that’s driven by AI is going to be large.” He compared the change to the Industrial Revolution, except that this one will happen over just a few decades.

Financial markets are already reorganising around AI, pumping up the value of so-called hyperscalers and key chipmakers while punishing the shares of any company suspected of being vulnerable to disruption. Periods of intense financial innovation without adequate oversight have rarely ended quietly, and social upheaval tends to follow economic crises. In this way, the same forces drawing capital into US markets, data centres and semiconductor demand could also intensify geopolitical tensions and competition.

We’re still a long way from the euro or the yen or the renminbi displacing the dollar, yet policymakers around the world are recalibrating. For example, the European Central Bank has begun revamping its euro liquidity facilities, explicitly aiming to make the single currency more attractive to global reserve managers. The move could help make the ECB another global lender of last resort. The Federal Reserve’s dollar swap lines were deployed at massive scale during the 2008 financial crisis and revived in 2020, bolstering the dollar along with US economic power.

The ambition is clear: If the US is less predictable, Europe should become a beacon of stability. ECB President Christine Lagarde speaks openly about the “deliberate weaponisation of dependencies” on America. “Trusted partners do not always remain so,” she said in a speech at the Munich Security Conference in February.

China, too, may see opportunity in American volatility.

The US’s growing appetite to intervene directly in markets, for example, by acquiring equity shares of Intel and other companies, and Trump’s attempts to bully the Federal Reserve, are showing China that the US economic system is less distinct from its own. The contrast between a market-oriented liberal democracy and a command system is no longer as stark in practice as it is in theory. If America blurs that line, China need not win the geopolitical contest outright. It can win by default.

What happens when trust dissolves? What we’re seeing now is allies hedging, building parallel institutions, exploring alternative payment systems and diversifying reserve holdings at the margin. In essence, they’re curbing exposure to America. Even if the US remains a dominant financial power, the margin of that dominance can shrink.

Multipolarity doesn’t require America to collapse. It requires others to develop credible alternatives.

The question for investors and policymakers is not whether the dollar falls from its perch. It’s whether trust erodes enough to raise the cost of capital for the US. Should portfolios diversify more aggressively away from dollar-based assets? These questions are no longer fringe.

Investors know that humility is warranted. The past year has been a cascade of apparent hinge moments like the April 2025 tariff announcements, Trump’s attempt to fire a sitting Fed governor, which seemed epochal and then receded as markets stabilised.

The TACO trade worked.

But accumulation matters, and institutional norms, once bent, may not snap back to their original shape. A central bank pressured once can be pressured again. A generation of workers displaced by automation doesn’t simply learn new skills on command.

The Trump administration is still counting on the benefits of a familiar international order. The US’s position in the global economy is “a key factor in enabling economic security,” Treasury Secretary Scott Bessent said in a February speech in Dallas. “This status rests on confidence in our institutions and, critically, in the health of the US Treasury market,” he said as he cited the importance of continued investment in the US. Unfortunately, Bessent is now seen as nothing more than a Trump mouthpiece, and of late has been using the same disrespectful tactics used by other Trump minions in congressional hearings.

Investors have an insatiable appetite for American federal debt, because it’s underpinned by institutions they still trust more than the alternatives.

It’s worth remembering that not everything is in the hands of the White House. Both the Fed and the courts are still asserting themselves. In a Supreme Court ruling in February, Justice Neil Gorsuch, whom Trump selected for the job during his first term, joined the majority to rule that the administration’s use of a specific law to impose tariffs was illegal. In the ruling, Gorsuch laid out a defence of the authority of Congress in such matters, explaining that its slow decision-making also lent itself to predictability. What the justice writes about congressional authority also speaks to America’s place in geopolitics.Retrieving a lost power is no easy business.

Author: Dawn Ridler

I remember reading news articles espousing the views of Mark Mobius as a student and later as a junior analyst. Mr Mobius had become synonymous with the investment world, leading the Franklin Templeton Emerging Markets Group, a role he would hold for over three decades. This was of particular interest in South Africa as the country was seen as an emerging market. What makes Mr Mobius’s career more remarkable is that he was hired by the legendary Sir John Templeton, who founded the group he was named after. Sir Templeton, was known for finding investment ideas which were out of the mainstream. Up to then, most investors would invest in their home markets only. Trying to invest across borders seemed too risky for many and this left a goldmine of undervalued opportunities in countries outside of the USA.

The Templeton Growth Fund was established in 1954 and became an amazing success led by Sir Templeton. He died in 2008 at 95. It was John Templeton who found a kindred spirit in Mark Mobius. Mr Mobius, always dressed to the tee, would find himself globetrotting while kicking the tyres of the investments he would be making in emerging and frontier markets. This allowed him to build a research network throughout an emerging world which earned him the nickname: “The Indiana Jones of emerging markets” The idea was simple: Hold assets in economies that are growing faster than the developed world, and if one can stomach the currency volatility and political noise, which invariably will happen, great returns can be achieved.

This invariably came during the Asian financial crisis in 1997, the Russian crisis in 1998 and later during the 2008-2009 crisis. This at least proves that through a lifetime, expect markets to go through volatile periods, but by staying the course allows for not only recovery but long-term compounding. Mr Mobius authored several books aimed at both professionals and individual investors, including “Passport to Profits” which blended travelogue and case studies from emerging markets, and “The Investor’s Guide to Emerging Markets” a 1995 primer on the rationale, risks, and methods for investing in developing economies. In 2019 he co‑authored “Invest for Good” laying out an approach to combining emerging‑markets investing with governance and ESG improvement.

After retiring from Franklin Templeton, Mr Mobius founded Mobius Capital Partners, where they focused on concentrated long-only investments in emerging and frontier markets. In a world that espouses diversification and benchmarks as risk-management tools, it is interesting to note that great investors later in their careers end up holding concentrated portfolios. Volatility is no longer seen as the enemy but is embraced, perhaps to add to the investment. Do this for long enough and superior returns seem to follow. But this requires confidence which has been built through a lifetime of investing. Mark Mobius died last week in Singapore at the age of 89.

Author: Cobie Le Grange

EXCHANGE RATES and other Indices:

The Rand/Dollar closed at R16.29 (R16.41, R17.07, R17.06, R16.89, R16.55, R15.93, R16.01, R15.96, R16,03, R16.15, R16.10, R16.50, …R16.91, R17.13, R17.36, R17.13, R17.27, R17.31, R17.25, R17.38, R17.50, R17.22 , R17.35, R17.33, R17.37, R17.58, R17.65, R17.44, R17.61, R17.74, R18.15,R17.76, R17.72, R17.90, R17.58, R17.89, R17.99, R17.92, R17.77, R17.95, R17.88)

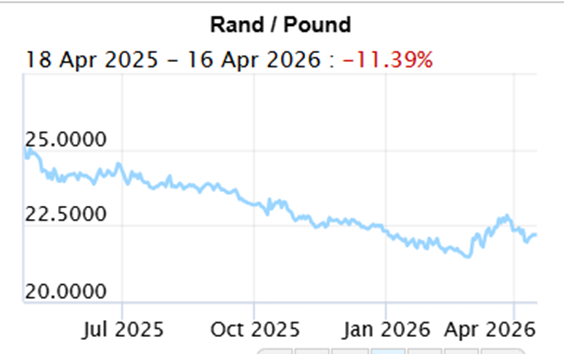

The Rand/Pound closed at R22.02 (R22.09, R22.77, R22.76, R22.35, R22.20, R21.48, R21.59, R21.78, R21,82, R22.11, R21.97, R22.13, …R22.57, R22.68, R22.74, R22.56, R22.69, R22.76, R22.96, R23.34, R23.37, R23.19, R23.22, R23.35, R23.55, R23.73, R23.84, R23.53, R23.84, R23.84, R24.09, R23.88, R23.76, R24.22, R24.08, R24.49, R24.22, R24.35, R24.05, R24.18)

The Rand/Euro closed the week at R19.17 (R19.24, R19.70, R19.77, R19.33, R19.23, R18.80, R18.87, R18.94, R18.93, R19.14, R19.04, R19.20, …R19.68, R19.86, R19.99, R19.96, R19.98, R20.02, R20.06, R20.26, R20.33, R 20.22, R20.30, R20.35, R20.38, R20.61, R20.62, R20.44, R20.56, R20.64, R21.04, R20.86, R20.61, R20.93, R 20.70, R20.91, R20.74, R20.68, R20.24, R20,37)

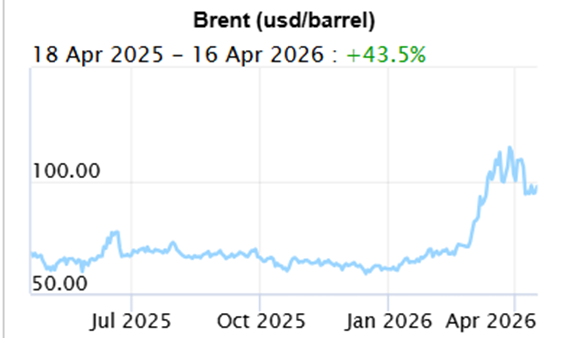

Brent Crude: Closed the week $90.38 ($95.20, $107.88, $112.36, $103.14, $92.88, $73.19, $71.76, $67.75, $68,05, $69.32, $65.88, $63.34, …$63.71, $63.19, $62.42, $63.94, $63.61 $64.66, $65.04, $61.27, $62.14, $64.28, $69.67, $66.57, $66.80, $65.52, $67.38, $67.73, $66.08, $66.07, $69.46, $68.29, $69.21, $70.58, $68.27, $67.39, $77.27, $74.38, $66.56, $62.61, $65.41)

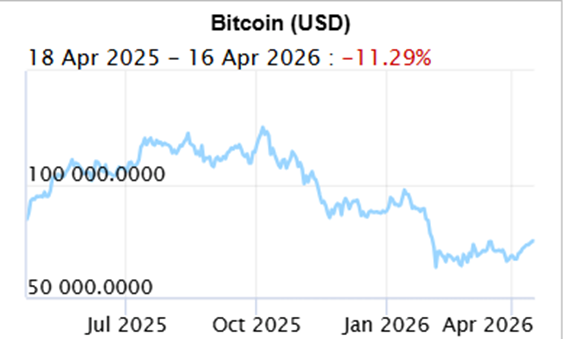

Bitcoin closed at $75,519 ($70,904, $68,691 , $68,586, $70,869, $67,310, $63,534, $68,04, $69,649, $68,553, $81,301, $89,295, $90,585, … $90,809, $86,334, $94,990, $101,562, $109.936, $112,492, $106,849, $111,888, $124,858, $109,446, $115,838, $115,770, $110,752, $108,923, $114,916, $117,371, $118,043, $113,608, $118,139, $118,214, $117,871, $108,056, $107,461, $103,455)

Articles and Blogs:

Dos and Don’ts of Wills and Estate Planning NEW

Planning your legacy, starting with your will NEW

Holiday checklist

Next year – Action Plan

Next year – Vision, Mission etc

Medical Risk Mitigation

Next Year – Consolidation

Abdication or diversification?

Carbo-loading your retirement Spoiled for choice

Who needs a plan anyway

8 questions you need to ask about retirement

What to do when interest rates drop

How to survive volatility in your investments

What to do when interest rates drop

Difficult Financial Conversations

Financial Implications of Longevity

Kick Start Your Own Retirement Plan

You matter more than your kids in retirement

To catch a falling knife

Income at retirement

2025 Budget

Apportioning blame for your financial state

Tempering fear and greed

New Year’s resolutions over? Try a Wealth Bingo Card instead.

Wills and Estate Planning (comprehensive 3 in one post)

Pre-retirement – The make-or-break moments

Some unconventional thoughts on wealth and risk management

Wealth creation is a balancing act over time

Wealth traps waiting for unsuspecting entrepreneurs

Two Pot pension system demystified

Cobie Legrange and Dawn Ridler,

Rexsolom Invest, Licensed FSP 45521.

Email: cobie@rexsolom.co.za, dawn@rexsolom.co.za

Website: rexsolom.co.za, wealthecology.co.za