Your summary with links, if you’d like to curate your content:

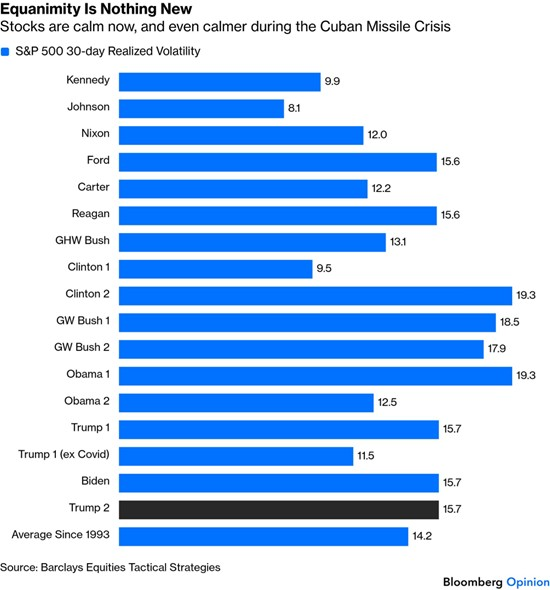

Market Volatility? Despite the Iran conflict and Trump’s executive-order style of governance, the S&P 500 hit a new all-time intraday high. Realised volatility under Trump’s second term has so far matched the calm Biden years — a surprising finding that may signal late-cycle market dynamics.

UK Leadership Turmoil: PM Keir Starmer faces mounting pressure over his appointment of Peter Mandelson as US ambassador, amid poor poll numbers and expected local election losses. Senior cabinet members are openly critical, yet Labour MPs cannot coalesce around a successor. Most observers believe it’s a matter of when, not if, Starmer leaves office.

Argentina: Economic activity fell 2.6% in February, the sharpest monthly drop since 2023. However, a trade surplus of $2.5 billion in March — the highest since 1990 — and rebounding exports offer some hope. Monthly inflation rose to 3.4%, stalling Milei’s disinflation campaign, while his approval rating fell to a record-low 36%.

The Defiant Rally: Global equities have rebounded strongly nearly two months into the Iran conflict, with markets largely looking past geopolitical risk. Key drivers include: markets having already priced in worst-case scenarios, a dip-buying mentality, strategic petroleum reserve releases cushioning the oil shock, strong Q1 earnings (80% of S&P 500 companies beating estimates), and renewed enthusiasm for AI stocks.

Tech Layoffs – People v Datacentres: Meta plans to cut ~8,000 jobs (10% of staff) and leave 6,000 roles unfilled, while Microsoft is offering voluntary buyouts to ~8,750 US employees. Both companies are redirecting spending toward AI infrastructure and data centres, continuing a multi-year trend of workforce reductions funding capital investment.

Japan – New Military Power? PM Sanae Takaichi’s cabinet approved legislation allowing Japan to export lethal military equipment — missiles, fighter jets, and warships — for the first time since WWII. Driven by threats from China and North Korea, Japan is pursuing defence industry growth, with an early warship deal already concluded with Australia and Southeast Asian outreach planned.

The Rebound: April delivered a strong equity recovery after March’s correction, with the S&P 500 reaching an all-time high supported by diplomatic progress on Iran and Fed liquidity. Large-cap tech and AI remain the dominant market drivers. Meta’s new AI tool, Muse Spark — a multimodal medical reasoning assistant developed with over 1,000 physicians — is highlighted as an example of AI’s expanding real-world impact.

This Week’s Roundup

The armed standoff in the Strait of Hormuz grows scarier as days tick by and stockpiles deplete. Meanwhile, the S&P 500 sets another record. Its course to the landmark hasn’t even been particularly bumpy. Has the market really become so desensitised to Trump’s rule by executive order?

Realised volatility in the turbulent second Trump term has so far been identical to vol under Joe Biden. The calmest presidential term since 1960 on this basis, amazingly, was Lyndon Johnson’s. The market digested the fallout from the Kennedy assassination, the civil rights movement, and Vietnam with minimal fuss. Kennedy’s term, including the Cuban Missile Crisis, was also strikingly calm.

The first Trump term was even calmer until the pandemic churned the waters. This is interesting, and may be another indication of ‘late cycle’ dynamics, but we can just wait and see.

When Boris Johnson’s turbulent premiership was finally terminated in the summer of 2022, the political removal was carried out by a demolition crew composed of his own cabinet. Over 40 dramatic hours, a succession of top government figures declared their unwillingness to keep serving a prime minister most voters had long concluded lacked honesty and judgment. By the end, Johnson had lost 50 ministers, including his chancellor of the exchequer and his education, health and work and pensions secretaries.

Prime Minister Keir Starmer is facing similar questions about his own probity because of his reckless decision to appoint Peter Mandelson, a close friend of the deceased Jeffrey Epstein, as UK ambassador to the US. Though he remains wildly unpopular with the public and his party is braced for a trouncing in important local and regional elections next month, Labour lawmakers have been unwilling or unable to reach for the pearl-handled revolver.

Time and again, Starmer’s parliamentary party has stepped back from the brink, largely because it cannot agree on who would succeed him, or even the type of government that person should lead.

The Labour left won’t accept the ambitious Health Secretary Wes Streeting, another Mandelson acolyte, or Home Secretary Shabana Mahmood, who’s too anti-immigration for their tastes. The right has conniptions over union-friendly ex-Deputy PM Angela Rayner and Energy Secretary Ed Miliband, a net-zero champion. The most popular candidate with the public and the party is Manchester Mayor Andy Burnham. Starmer has blocked him from reentering Parliament for purely self-preserving reasons.

That has led to a non-contest, with wannabe contenders, wary of the taint of betrayal which attaches to those who attack first, reluctant to declare themselves while Starmer remains in situ.

It may be that this dynamic continues even after the May 7 elections, expected to be brutal. But Starmer’s authority is so shot that few believe he’ll serve the full term. It’s not a case of if, it’s when.

Wariness about toppling the PM has some logic. Labour members of Parliament don’t know who might enter the fray or what they’d do should they win. They rightly fear that what follows could be even worse.

The prime minister can no longer rely on senior colleagues to show him unconditional loyalty or defend his missteps. Foreign Secretary Yvette Cooper, Work and Pensions Secretary Pat McFadden and Scotland Secretary Douglas Alexander, usually the most cautious members of the government, have all criticised Starmer in recent days. Miliband made clear that he’d opposed Mandelson’s appointment.

There have been critical leaks to the media about Starmer’s sacking and hanging out to dry of Olly Robbins, the official in charge of the Foreign Office, for not telling the PM that Mandelson had failed a security vetting.

The first priority for anyone who thinks they have what it takes for the top job is the intellectual heavy lifting of determining what they want to do with the power they would wield. This is probably Starmer’s biggest failing The UK prime minister still heads up one of the world’s largest economies, one that’s a permanent member of the UN Security Council and a leading member of the North Atlantic Treaty Organisation.

Argentina’s economy contracted sharply in February, posting its biggest monthly decline since 2023, as retail and manufacturing continue to struggle.

Economic activity fell 2.6% from January. A year ago, the gross domestic product proxy fell 2.1%, far below the 0.5% median estimates.

Argentine Economy Minister Luis Caputo said earlier this month in Rosario that the country’s economy will post growth in April, while monthly inflation will also slow. March tax collection data already shows that economic activity has started to rebound.

In March, the trade balance delivered a $2.5 billion surplus, the highest for the month since 1990. The first quarter delivered a $5.3 billion surplus on an export surge, a sharp uptick from $1 billion a year ago, the note said. Exports on the month in March turned around sharply from a 14.5% drop in February to a 19.8% surge, according to the national statistics agency.

Monthly inflation, which Milei vowed to slow below 1% this year, picked up to 3.4% in March and hasn’t slowed in 10 months. It’s still a significant improvement from the crisis Milei inherited, but his disinflation campaign has lost momentum. Milei asked Argentines earlier this month to be patient with the country’s economic turnaround, employing a rare tone of humility amid declining poll numbers and a worsening outlook for blue-collar industries. His approval rating last month hit its lowest since he took office in falling to 36%.

Nearly two months into the conflict in Iran, global stock markets are staging a defiant rally. From the US to Taiwan and South Korea, a disconnect has emerged: while the geopolitical tensions remain high, equities are charging back toward all-time highs.

After an initial shock, financial markets have largely looked past the conflict to focus on corporate fundamentals, even as oil prices remain elevated. Investors are piling back into the artificial intelligence trade and emerging-market stocks, signalling that the worst of the volatility is now in the rearview mirror. The US dollar has mostly given back its gain from the start of the conflict.

Here are some reasons why there hasn’t been a more negative reaction to the geopolitical conflict:

Peak Uncertainty

Analysts say that markets have already priced in a worst-case scenario and believe in a potential offramp from the conflict. With officials in both Washington and Tehran keeping their doors open to talks and an extended ceasefire declaration, markets have remained confident that a deal will be done. In other words, while geopolitical tensions linger, there’s growing belief that diplomacy, rather than a full collapse, is the likely endgame.

Dip-Buying Mentality

Rapid-fire headlines and President Donald Trump’s frequent changes in course have caught many investors off guard. Many are referring to the Ukraine-war playbook from early 2022, when an initial equities selloff and commodity price surge soon reversed to business as usual. Years of headline-driven volatility and a dip-buying mindset have further reinforced investors’ reluctance to stay bearish for too long.

Oil Cushion

The war’s energy supply shock may have pushed oil and gasoline prices higher, but outside of acute shortages in some emerging countries, it has not yet triggered the broad economic shutdown many feared. Record releases from strategic petroleum reserves, some spare capacity among major oil producers and demand destruction have so far cushioned the impact. However, prolonged disruptions in the Strait of Hormuz could still escalate into more severe economic consequences. This suggests that investors are still pricing in a relatively speedy restoration of calm to energy supplies.

Robust Earnings

Company earnings have given markets a much-needed shot in the arm. Nearly 80% of the S&P 500 companies reporting first-quarter results so far have beaten analyst earnings estimates, according to data compiled by Bloomberg. A number of brokers have already revised up earnings growth for the year, leading analysts to turn more upbeat on fundamentals.

AI is Back

Technology shares have been the major driving force behind the stock rally as earnings show resilience amid the war, thanks to solid artificial-intelligence demand. On Thursday, SK Hynix Inc. reported a fivefold jump in quarterly profit as the South Korean memory chipmaker reiterated plans to ratchet up its spending. This comes after Taiwan Semiconductor Manufacturing Co. raised its 2026 revenue outlook while Samsung Electronics Co. posted an eightfold jump in quarterly profit. Analysts say that upcoming earnings and spending plans from hyperscalers will be key catalysts for further upside.

Tech layoffs – People v Datacentres

Meta Platforms Inc. and Microsoft Corp. are planning cuts or announcing buyouts that could affect as many as 23,000 jobs, part of an effort to streamline operations and offset heavy spending on artificial intelligence.

Meta told personnel in an internal memo last Thursday that it planned to cut 10% of workers, or roughly 8,000 employees, starting on May 20. The social-media company also said it wouldn’t fill 6,000 open roles.

Earlier in the day, Microsoft issued its own memo offering voluntary buyouts to thousands of its US employees. About 7% of the US workforce will be eligible for the buyouts, according to a person familiar with the planning. The company has never previously done buyouts of this scale.

Microsoft had 125,000 employees in the US as of June 2025. That would make about 8,750 workers eligible for the program.

Big tech companies have been looking for ways to trim their expenses as they pour billions into data centres and other infrastructure to meet demand for artificial intelligence services.

Microsoft is racing to construct data centres around the world, and this month announced new AI investments in Japan and Australia. Meta, meanwhile, has projected record capital expenditures this year and has announced several multibillion-dollar deals with AI partners over the past few months. Both companies have instituted several rounds of layoffs in recent years.

Meta employees have spent much of the year fretting about job cuts, which already hit the Reality Labs division and other teams. The company was announcing the layoffs early since details of the plan had already leaked.

Microsoft’s buyout program is being offered to workers whose years of service plus their age totals 70 or more, excluding some senior roles or those on sales incentive plans.Both companies are scheduled to report quarterly earnings on April 29.

When Japan’s Mitsubishi “Zero” fighter jet took to the skies in the early 1940s, it quickly gained a reputation as lethal in dogfights thanks to its agility and speed. It was one of the most significant achievements of a defence industry that collapsed following Tokyo’s wartime defeat.

Eight decades after Japan enshrined a commitment to pacifism in its post-WWII constitution, Prime Minister Sanae Takaichi is on a mission to revive the sector.

She’s pursuing a vision of a more powerful nation, able to stand up to rising threats from China and North Korea without simply relying on the US for protection.

Takaichi’s cabinet approved legal changes this week that will, for the first time since the war, allow Japan to export lethal military equipment such as missiles, fighter jets and warships.

Her hope is that the defence industry can flourish by tapping into soaring global demand, in turn developing a more robust supply of home-grown material for Japan’s military. The moment appears ripe.

Conflicts in the Middle East and Ukraine are driving innovation and orders. Takaichi is offering government money for Japanese companies to invest in defence R&D.

China has taken notice, issuing warnings about a revival of Tokyo’s past militarism under which it suffered. There is some domestic concern about the move: A recent poll found 67% of respondents opposed weapons exports.

But one big deal has already been done to provide Australia with warships, and Takaichi’s approval is holding up well.

She is, in any case, not alone, with Germany also casting off postwar reticence and ramping up its defence capabilities.

In the coming weeks, Takaichi and her defence minister are planning trips to Southeast Asian countries that are in the market for equipment to respond to challenges from Beijing. Orders from those nations could be among the first steps to a renaissance of Japanese military manufacturing.

Author: Dawn Ridler

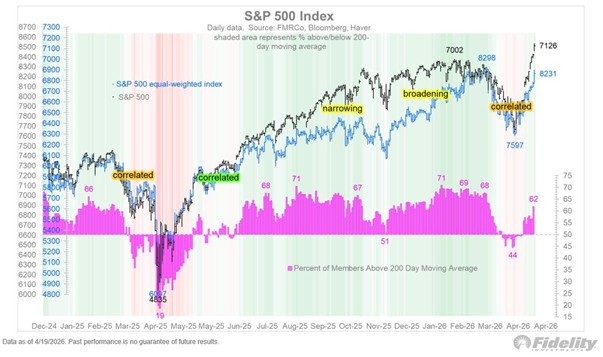

April has proven to be a good month for equities after the sharp correction in March. The following chart from Jurrien Trimmer at Fidelity shows both the S&P500 Index and its equally weighted alternative in blue and black. I continue to believe that in a fiscally dominated world, corrections tend to be quickly reversed as policymakers’ actions allow for markets to change trajectory again. In the case of the Iranian crisis, it was both the diplomatic efforts and the FED’s extra liquidity which sent the S&P500 to an all-time high.

It is clear from the negotiations that there is a road that needs to be walked in the Middle East and that the Strait of Hormuz remains the central piece on the chessboard.

In the absence of the Iranian crisis, focus returns to AI and how this will shape the world that we live in. Consider Meta’s latest AI offering called Muse Spark. It has various applications but one notable one is in the world of health. Here, Meta has collaborated with over 1000 physicians to curate trained data to assist practitioners across the world. In its “Contemplating” mode, it will run multiple reasoning agents in parallel, aggregate their conclusions and then provide a holistic answer which needs to be used in conjunction with a diagnosis.

In short, this becomes the guardrails for a diagnosis and clarifies the problem so that better outcomes can be achieved. Because it is multimodal (it can connect images, text and audio), it allows for the tool to encapsulate more data points, which should lead to a better diagnosis.

Fans of the Netflix series “Dr House” will know that the rather offbeat Doctor with his team are seen trying to come up with a medical diagnosis for tricky cases. Muse Spark should short-circuit much of the guesswork, allowing for treatment to start much quicker.

Somehow, I think Dr Gregory House would not have been amused by Muse Spark, but the good news is that he most certainly would have been used for his input knowledge. Now, is that not much more interesting than the Iran war?

From the chart we learn that the S&P500 gained at a faster rate than the equally weighted Index. This shows that large tech companies and their AI initiatives still hold centre stage.

Author: Cobie Le Grange

EXCHANGE RATES and other Indices:

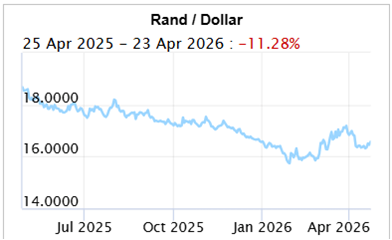

The Rand/Dollar closed at R (R16.29, R16.41, R17.07, R17.06, R16.89, R16.55, R15.93, R16.01, R15.96, R16,03, R16.15, R16.10, R16.50, …R16.91, R17.13, R17.36, R17.13,16.52 R17.27, R17.31, R17.25, R17.38, R17.50, R17.22 , R17.35, R17.33, R17.37, R17.58, R17.65, R17.44, R17.61, R17.74, R18.15,R17.76, R17.72, R17.90, R17.58, R17.89, R17.99, R17.92, R17.77, R17.95, R17.88)

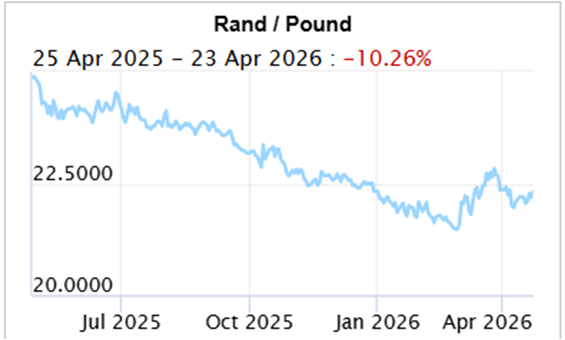

The Rand/Pound closed at R22.35 (R22.02, R22.09, R22.77, R22.76, R22.35, R22.20, R21.48, R21.59, R21.78, R21,82, R22.11, R21.97, R22.13, …R22.57, R22.68, R22.74, R22.56, R22.69, R22.76, R22.96, R23.34, R23.37, R23.19, R23.22, R23.35, R23.55, R23.73, R23.84, R23.53, R23.84, R23.84, R24.09, R23.88, R23.76, R24.22, R24.08, R24.49, R24.22, R24.35, R24.05, R24.18)

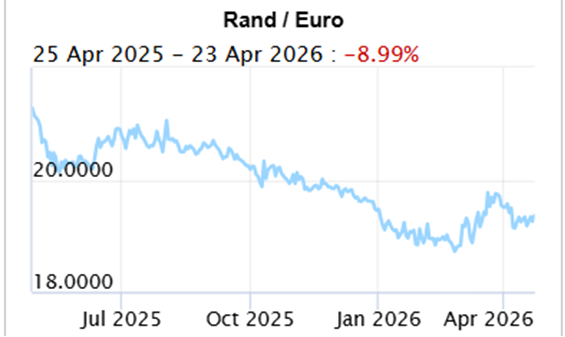

The Rand/Euro closed the week at R19.37 (R19.17, R19.24, R19.70, R19.77, R19.33, R19.23, R18.80, R18.87, R18.94, R18.93, R19.14, R19.04, R19.20, …R19.68, R19.86, R19.99, R19.96, R19.98, R20.02, R20.06, R20.26, R20.33, R 20.22, R20.30, R20.35, R20.38, R20.61, R20.62, R20.44, R20.56, R20.64, R21.04, R20.86, R20.61, R20.93, R 20.70, R20.91, R20.74, R20.68, R20.24, R20,37)

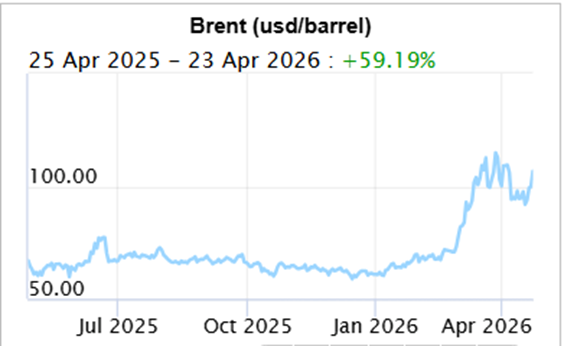

Brent Crude: Closed the week $105.33 ($90.38, $95.20, $107.88, $112.36, $103.14, $92.88, $73.19, $71.76, $67.75, $68,05, $69.32, $65.88, $63.34, …$63.71, $63.19, $62.42, $63.94, $63.61 $64.66, $65.04, $61.27, $62.14, $64.28, $69.67, $66.57, $66.80, $65.52, $67.38, $67.73, $66.08, $66.07, $69.46, $68.29, $69.21, $70.58, $68.27, $67.39, $77.27, $74.38, $66.56, $62.61, $65.41)

Bitcoin closed at $78,049.98 ($75,519, $70,904, $68,691 , $68,586, $70,869, $67,310, $63,534, $68,04, $69,649, $68,553, $81,301, $89,295, $90,585, … $90,809, $86,334, $94,990, $101,562, $109.936, $112,492, $106,849, $111,888, $124,858, $109,446, $115,838, $115,770, $110,752, $108,923, $114,916, $117,371, $118,043, $113,608, $118,139, $118,214, $117,871, $108,056, $107,461, $103,455)

Articles and Blogs:

Dos and Don’ts of Wills and Estate Planning NEW

Planning your legacy, starting with your will NEW

Holiday checklist

Next year – Action Plan

Next year – Vision, Mission etc

Medical Risk Mitigation

Next Year – Consolidation

Abdication or diversification?

Carbo-loading your retirement Spoiled for choice

Who needs a plan anyway

8 questions you need to ask about retirement

What to do when interest rates drop

How to survive volatility in your investments

What to do when interest rates drop

Difficult Financial Conversations

Financial Implications of Longevity

Kick Start Your Own Retirement Plan

You matter more than your kids in retirement

To catch a falling knife

Income at retirement

2025 Budget

Apportioning blame for your financial state

Tempering fear and greed

New Year’s resolutions over? Try a Wealth Bingo Card instead.

Wills and Estate Planning (comprehensive 3 in one post)

Pre-retirement – The make-or-break moments

Some unconventional thoughts on wealth and risk management

Wealth creation is a balancing act over time

Wealth traps waiting for unsuspecting entrepreneurs

Two Pot pension system demystified

Cobie Legrange and Dawn Ridler,

Rexsolom Invest, Licensed FSP 45521.

Email: cobie@rexsolom.co.za, dawn@rexsolom.co.za

Website: rexsolom.co.za, wealthecology.co.za