The Legacy Series Blog/Post series is now complete and will be published in a free eBook shortly. If you missed any of them, here are the links again.

Your summary with links, if you’d like to curate your content:

The EU Anti-Coercion Instrument (ACI) – An Explainer The ACI, nicknamed the “trade bazooka,” is the EU’s regulatory tool to counter economic coercion by third countries. It can shut foreign businesses out of the 500-million-consumer European single market, restrict trade licences, public procurement access, intellectual property protections, and foreign direct investment. Originally designed as a deterrent against China (following the Lithuania-Taiwan dispute in 2021), it has never been used. The EU is now consulting on whether to deploy it against both the US (over the Greenland crisis) and China (over record trade surpluses and BYD’s surging European sales). A European Commission debate on China is scheduled for 29 May.

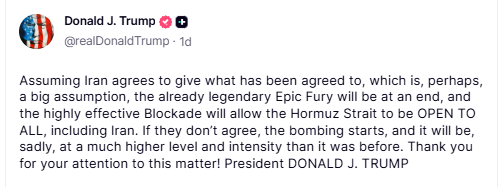

Inflation-Linked Bonds: BlackRock’s $15 billion US TIPS ETF is seeing its largest monthly inflows since 2021, as investors hedge against a prolonged inflation shock from the Iran war. Similar trends are appearing in Europe and Japan. In South Africa, inflation-linked retail bonds carry a ~1.5% premium over standard bonds — only worthwhile if inflation exceeds ~4.5%. The US 10-year breakeven rate has surged past 2.5% for the first time in three years, signalling serious inflation expectations. The newsletter highlights Rexsolom’s “Bond Ladder” strategy as an income-generating alternative to living annuities.

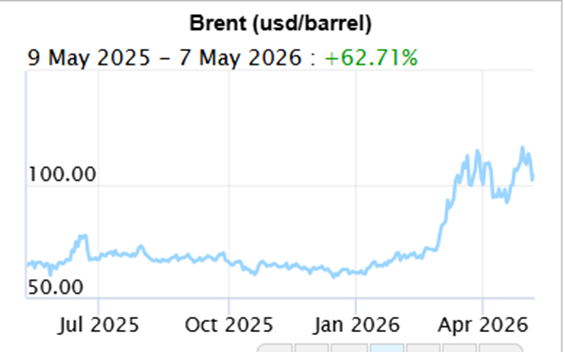

Trump’s Iran War – TACO?: Trump declared the war effectively over after 60 days — likely to avoid needing congressional approval. A preliminary US peace proposal was described by Iran as “more of an American wish-list than a reality.” Iran’s parliament speaker publicly mocked reports of a deal with “Operation Trust Me Bro failed.” Brent crude pulled back to ~$100 on ceasefire optimism, but no substantive agreement exists. A key development: Saudi Arabia suspended US military use of a Saudi base for the Strait reopening operation — a significant diplomatic signal. Preliminary negotiations, led by Steve Witkoff and Jared Kushner, would start a 30-day clock for a full agreement, but key US demands — Iran’s nuclear programme, missile restrictions, and Strait reopening — remain unresolved.

Oil Supply Starting to Bite : Even if a peace deal is reached, oil supply normalisation will take months. An estimated 500–600 million barrels have already been consumed from global stockpiles. Global inventories are expected to drop to ~98 days of demand by end of May, from 105 days at the start of the conflict. Goldman Sachs warns refined product buffers are “approaching very low levels fast.” Europe could face jet fuel shortages as early as June. Ireland has just 10 days of jet fuel stock cover. Asia’s crude imports fell 30% in April year on year. Australia is spending $7.22 billion to build fuel reserves. Rystad Energy estimates the world will have lost 1.2–2.0 billion barrels of supply by the time shipping normalises. South Africa’s own refining capacity is extremely limited, with Natref near Sasolburg and Astron Energy in Cape Town among the few still operational.

US Inflation: Fed officials are openly warning of a sustained inflation shock. Chicago Fed President Goolsbee noted businesses are “using up” input stockpiles and facing intensifying supply chain pressure. St. Louis Fed President Musalem said risks have shifted firmly toward inflation, with rate hikes now a possibility. PCE inflation rose to 3.5% in March (from 2.8%), core PCE to 3.2%. US pump prices have risen from ~$3 to over $4.50/gallon. A New York Fed supply chain pressure index hit its highest since July 2022. Rate cuts are now expected to be delayed well into 2027 or beyond, complicating Kevin Warsh’s incoming chairmanship.

What is Stagflation?: A concise explainer covering the definition (simultaneous stagnant growth, high inflation, and high unemployment), the policy trap it creates (raising rates fights inflation but worsens growth; cutting rates stimulates growth but worsens inflation), and the classic 1970s OPEC oil embargo as the historical parallel. The current Iran/Hormuz oil shock is described as operating through an identical mechanism, with every major central bank — the Fed, ECB, and SARB — now facing the same impossible policy dilemma

Value and Growth: A reflective piece on investment philosophy. The author argues that “value” and “growth” — long treated as opposing fund management styles — are actually two sides of the same coin: value is simply the price paid for future growth. The piece traces the rise of specialist fund managers and DFMs in post-apartheid South Africa, critiques the rigidity of style-based mandates, and introduces the concept of “moats” — competitive advantages that determine a company’s ability to sustain superior returns over time. The core insight: paying a high price for a wide-moat company that can defend its position for decades may itself be a value opportunity.

This Week’s Roundup

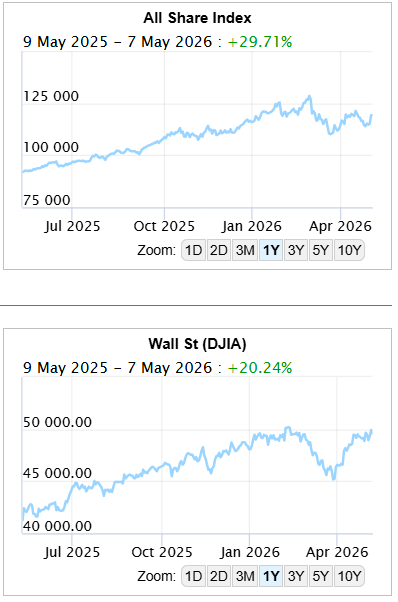

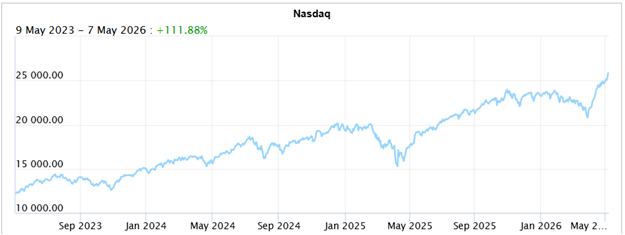

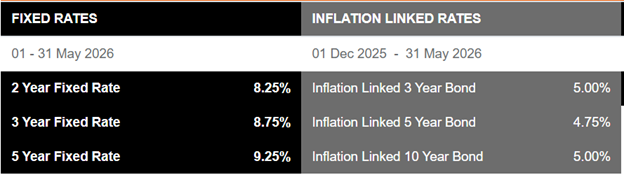

The S&P 500 and Nasdaq Composite closed April at record-high levels, capping what was their best monthly performance since 2020, with the Dow Jones recording its strongest month since November 2024, powered by blockbuster tech earnings and fresh ceasefire optimism.

The EU Anti-Coercion Instrument (ACI) – an explainer

It is one of the most significant and novel tools in European trade policy. Here’s a brief explainer:

What it is

The Anti-Coercion Instrument is a regulation of the European Union proposed in December 2021, adopted in November 2023, and entered into force on 27 December 2023. It aims to protect the EU and its member states from economic coercion by third countries and provides a framework for EU action, including examination, engagement, and the adoption of countermeasures. It is widely nicknamed the “trade bazooka.”

What triggers it

Under the ACI, economic coercion exists where a third country applies or threatens to apply measures affecting trade or investment in order to prevent or obtain the cessation, modification, or adoption of a particular act by the EU or a member state, thereby interfering in the legitimate sovereign choices of the EU or a member state. The key distinction from ordinary trade disputes is intent: the coercing country must be using economic pressure specifically to change EU or member state policy.

What it can actually do

The ACI allows the EU to shut off access to the European single market, representing 500 million consumers, limit trade licences and access to public procurement tenders and for American, Chinese or any foreign services companies, it means the European market would effectively be off the table. More specifically, countermeasures can include imposition of new or increased customs duties on imports or exports, restrictions on the import or export of goods, and exclusion from EU public procurement procedures of economic operators, goods, services, or works from the coercing country. The instrument can also restrict intellectual property protections and foreign direct investment.

How the process works

The tool is not automatic and takes time to implement. Once the question of coercion is raised, the European Commission has four months to assess the case and the actions of the third country in question, after which EU member states must decide by qualified majority whether to activate the instrument. This qualified majority voting was a deliberate design choice, removing the veto power that any single member state might use to block action, which had been a recurring problem under previous EU trade defence frameworks.

Why has it never been used?

EU officials consistently stress that the ACI’s primary aim is deterrence. The Commission’s own guidance notes that the instrument will be most successful if there is no need to use it, signalling that the existence of a clear, credible response mechanism is meant to dissuade coercive behaviour. The aim of the instrument, which has not yet been used, is to deter, sending a message to international trading partners that the EU will not tolerate economic coercion.

Who it was designed for and where things stand now

The ACI was originally developed primarily as a deterrent against China, following China’s imposition of trade restrictions on Lithuania after Lithuania permitted Taiwan to open a representative office there in 2021. As of January 2026, EU leaders are weighing their potential first use against the United States in response to the Greenland crisis. In the current context, the EU is also consulting industry groups on whether to deploy it against China over the trade deficit and overcapacity issues discussed in this week’s news, with a European Commission debate on China scheduled for 29 May. In short, it is a powerful but untested weapon, and the geopolitical pressure to finally use it for the first time is the highest it has ever been.

In RSA, we have been living with higher-than-the-rest-of-the-globe inflation for decades now, and our investment strategies have evolved to mitigate the capital erosion that the West had probably forgotten about until recently.

During the Covid oil crisis in the West, there was a rush into inflation-linked bonds, which, in retrospect, was not really necessary – what about now?

Well, BlackRock Inc.’s $15 billion exchange-traded fund for US Treasury Inflation-Protected Securities is attracting its largest monthly inflows since 2021.

The argument is that, even if energy prices continue to drop, the turmoil caused by the two-month war in Iran will have a long-lasting impact on the global economy. In the US, gasoline prices are near the highest since 2022, while in the Mideast, damaged natural gas facilities may take years to fix. The rise in inflation-linked bonds is also being seen in Europe and Japan.

Let’s add RSA into the mix, using Retail Bonds as an example.

You can see from the graphic above, you’re giving away around 1,5% on a 5-year bond (rounding inflation up to 3% – it is currently at 3,1%). Basically, if inflation spikes over 4,5%, you’ll be winning – less than that is the premium you’re paying for that guarantee. If you don’t need the income, and just leaving it there so interest builds on interest, then a non-inflation-linked retail bond is probably a better bet. Even if you want an income, one way to build in your own ‘resilience’ is to invest back that 1,5% you’re getting ‘extra’ for taking the risk.

Inflation-linked bonds have often been seen as a staid investment, favoured by the likes of pension funds seeking to match assets against their liabilities going out decades into the future. Yet when concerns about inflation grow, they can quickly attract a wider range of investors wagering on the direction of consumer prices.

At Rexsolom, we use bonds extensively as the backbone for our clients’ income-producing portfolios – and not just in compulsory retirement funds. Our new ‘Bond Ladder’ strategy for conservative portfolios in effect ‘mimics’ a Life Annuity (as opposed to a more common Living Annuity) without losing the capital.

Euro inflation-linked bond funds saw nearly €500 million in net inflows in March — the strongest since March 2022, marking a reversal after almost a year of outflows.

The rush is showing up across market metrics. The “extra compensation” (see the paragraph above) investors demand to hold US 10-year nominal bonds versus their inflation-protected counterparts, known as the breakeven rate, surged past 2,5% last week for the first time in three years. The RSA ‘breakeven’ is still only 1,5%. This signals an expectation of an inflation surge. A similar gauge in the euro area also hit the highest since 2023, and Japan’s equivalent has been testing 2% premium for the first time since the nation sold inflation-linked bonds over two decades ago.

Trump has a good reason to declare the Iran war over, as he did early last week, because after 60 days, he needs congressional approval, which he may not get. If he can declare this war over, and it restarts, he’ll just call it a new war – watch.

In a Truth Social Dropping, President Donald Trump on Wednesday last week predicted a swift end to the war with Iran as Tehran considered a U.S. peace proposal that sources said would formally end the conflict while leaving unresolved key U.S. demands that Iran suspend its nuclear programme and reopen the Strait of Hormuz. Winning?

An Iranian foreign ministry spokesperson described the proposal as “more of an American wish-list than a reality.”

A senior Pakistani official involved in the talks said that negotiators were hopeful of reaching a deal but noted gaps between the sides remained.

“Our priority is that they announce a permanent end to war and the rest of the issues could be thrashed out once they get back to direct talks,” said the official, speaking on condition of anonymity.

Iran has been trolling Trump for weeks on social media, and Iran’s parliament speaker, Mohammad Baqer Qalibaf, appeared to mock reports that indicated the two sides were close, writing on social media in English that “Operation Trust Me Bro failed.”

Qalibaf said such reports amounted to U.S. spin following its failure to open the Strait of Hormuz.

Amazingly, the markets still believe Trump, and as of Saturday, the price of Brent is back around $100. Day traders and speculators (some with an ‘uncanny’ knack for predicting the latest Truth Dropping) are having a field day. Perhaps the market is pricing in that no more military action will take place but the cost of this war is mounting up and will make the Midterms increasingly difficult for Trump if it persists – if he cares. There is a school of thought that says that Trump would relish the idea of a Republican loss – a kind of “You’re nothing without me”, scorched earth approach.

Trump, last Tuesday, paused a two-day-old naval mission to reopen the blockaded strait, citing “progress in peace talks”.

However, it is more likely that Trump’s abrupt reversal came after Saudi Arabia suspended the U.S. military’s ability to use a Saudi base for the operation (apparently, he didn’t even give them the heads-up). Saudi Arabia has always been the most powerful US ally in the Middle East, so this is more important than it appears on the surface.

The U.S. military has kept up its own blockade on Iranian ships in the region. U.S. Central Command said forces fired at an unladen Iranian-flagged tanker on Wednesday, disabling the vessel as it attempted to sail toward an Iranian port in violation of the blockade.

The source briefed on the mediation said the U.S. negotiations were being led by Trump’s envoy Steve Witkoff and son-in-law Jared Kushner. If both sides agreed on the preliminary deal, that would start the clock on 30 days of detailed negotiations to reach a full agreement. The memorandum would not initially require concessions from either side; it did not mention several key demands Washington has made in the past, which Iran has rejected, such as the restrictions on Iran’s missile programme and an end to its support for proxy militias in the Middle East. It made no mention of Iran’s existing stockpile of more than 400 kg (882 pounds) of near-weapons-grade uranium. Does this sound like ‘winning’ to you?

You know things are getting bad when flight insurers rewrite their policies to include anything to do with trip cancellations because of oil supply. Even stalwarts like British Airways are ‘consolidating’ trips (note that there are often two BA flights a day out of OR Tambo to Heathrow, so keep checking your flight).

Oil supplies are set to tighten further in the coming weeks, even if the U.S. and Iran agree on a peace deal to end their war, because it will take weeks for oil shipments to resume from the Middle East Gulf and reach refiners worldwide, so oil companies will continue to deplete storage tanks to meet peak summer demand.

The world has used temporary buffers – commercial stockpiles, oil in transit or held in storage at sea and emergency reserves – to offset the shock from the war in the Middle East. The full impact of the disruption to oil supplies has yet to wash through markets and the global economy because it will be many months before Middle East production and exports return to pre-war levels.

The rapid depletion of commercial stockpiles and emergency reserves has come at a time when stockpiles typically build as refiners and retailers prepare for peak travel and agriculture demand during the Northern Hemisphere summer. The global energy system will soon enter peak demand in a weakened position to deal with the spike in consumption from summer driving, aviation, farming and freight. Remember that this oil crisis is also heavily impacting fertiliser production too.

Even if crude supplies through the Strait of Hormuz start recovering soon, it is expected that supply will drop to the lowest since at least 2018, when tracking data became available.

That would stress the global energy system and extend the time it would take for oil producers and refiners to relieve supply shortages and for high fuel prices to return to pre-war levels.

It is estimated that at least 500 million barrels have already been consumed from stockpiles.

For comparison, the U.S. has about 460 million barrels of crude oil in its inventories. The US does not have a supply problem, per se; it is essentially self-sufficient, but the PRICE of ‘gas’ is becoming a potential midterm deal-breaker for Republican voters in the midterms – even for the die-hard MAGA base.

While oil futures would likely fall quickly in the event of a deal, it would be some time before physical crude and gasoline prices fall to pre-war levels as supplies recover from one of the biggest supply disruptions in history. Analysts have steadily raised their forecasts this year, and a Reuters poll last week had them pegging Brent futures to average $86.38 a barrel this year, up from around $62 a barrel in January.

Demand is likely to run higher once the conflict is over, as countries and companies worldwide look to rebuild stockpiles and restart shut-in production facilities, and some countries that have suffered shortages start building new stockpiles.

Australia, which imports roughly 80% of its fuel and has experienced shortages since the start of the conflict, announced plans on Wednesday to spend $7.22 billion to build up fuel reserves.

The European Commission said last month it would consider reviewing the EU’s requirement for countries to hold at least 90 days of oil stocks, to include a specific jet fuel requirement.

Since late February, when the war began, stockpiles have fallen quickly. Global inventories are expected to drop to around 98 days of demand by the end of May from 101 days currently and from 105 days at the end of February, Goldman Sachs said this week, warning that refined product buffers are “approaching very low levels fast.”

So far the world has lost around 600 million barrels of oil supply, according to Rystad Energy. By the time supply returns to normal, assuming normalisation of shipping starts at the end of May, the world will have lost 1.2 billion to 2.0 billion barrels of supply, equivalent to between 16-27% of pre-war global inventories, said Claudio Galimberti, chief economist at Rystad Energy.

Global gas supplies have also taken a big hit due to the closure of Qatar’s liquefied natural gas (LNG) production and damage sustained during the war. The loss of supply will total between 30 million tonnes and 50 million tonnes of LNG, equivalent to between 7%-11% of annual global supply, Galimberti said.

U.S. gasoline inventories would fall to around 198 million barrels by late summer – the lowest level for that time of year in modern records. U.S. gasoline stocks were just under 220 million barrels on May 1, the lowest for this time of year since 2014, government data showed. Rising exports to meet demand from countries experiencing shortages have accelerated the drawdown.

Europe could face jet fuel shortages as early as June if disrupted Middle East supplies are not fully replaced, the International Energy Agency has warned.

Ireland had just 10 days of stock cover for jet fuel supplies, according to a note from Goldman Sachs published last week.

In Asia, crude imports fell 30% in April from a year earlier to the lowest since 2015,underscoring the extent of supply disruption in the world’s largest oil-consuming region.

Onshore fuel oil inventories in Singapore, a major bunker hub, fell to a near one-year low in the week to April 29, as both imports and exports declined, data showed last week.

Picture: Enref’s Durban Facility

Side note : RSA’s refining history and capability

RSA only has very limited refining capacity left – we have to import our energy already refined.

Countries such as the United Kingdom, Norway and Portugal hold no strategic reserves of jet fuel. Others, such as Ireland, have seen their inventories depleting, with the country holding just 10 days of stock cover, down from 118 days of reserves.

Even if supply routes reopen, it would take one to two months for oil flows to normalise after the Strait of Hormuz reopens, as shipping backlogs clear. It takes on average 30 days for ships to move from the Middle East to the European Union, and 40 days to move from there to the U.S.

Meanwhile, the disruption to refining capacity in the Middle East will hamper the recovery in supply with nearly two million bpd of refining capacity offline in the region. Fuel from the Middle East is key to meeting demand in Africa, Asia, and Europe.

As we have mentioned several times in the last few months, the proposed new Fed Chair, Kevin Warsh, is going to be stepping into a world of pain, especially if he wants to please his boss, Mr Trump. Federal Reserve officials said last Wednesday that the ongoing U.S.-backed war with Iran is raising the risk of a sustained inflation shock, with persistently high oil prices and growing concerns about disruptions to global supply chains.

It is interesting to see what the other regional Fed chairs are saying on the record:

Chicago Fed President Austan Goolsbee said business executives told him shortly after the conflict began on February 28 that a short rise in oil prices would not be a problem, but “if this was going to be month after month of really extended high oil prices, they would start to feel pretty intense pressures on the supply chain,” reminiscent of what helped drive the inflation surge during the COVID-19 pandemic.

“You’re starting to see some of these problems developing,” Goolsbee said in a video call with journalists, “The longer it goes, the more you’re going to have these problems, because they’re using up what stock of inputs they had” for industrial chemicals and other inputs whose distribution has been disrupted, while sustained high fuel prices are feeding through to shipping and other costs.

While there was initial concern that the war would hurt U.S. job growth and demand while also leading to higher prices, if stagflation (see explainer below) rears its ugly head, then prospects are even more dire.

Speaking separately, St. Louis Fed President Alberto Musalem said the risks to monetary policy have shifted towards higher inflation, possibly requiring interest rates to stay on hold “for some time,” and perhaps even move up.

“Inflation is running meaningfully above our target,” Musalem said in comments, “We have risks both on the employment side and on the inflation side. In my understanding, risks have been shifting towards … the inflation side,” adding weight to expectations that the Fed would at least keep its policy rate on hold.

While there were “plausible scenarios” in which the Fed could cut rates, if demand slowed and the unemployment rate rose, Musalem said the same was true at this point about the central bank possibly hiking borrowing costs.

“There’s a lot of uncertainty right now, and it’s important to see how things settle,” said Musalem, noting that inflation pressures were moving beyond the impact of tariffs and high oil prices due to the war in the Middle East.

The average U.S. price of gasoline at the pump has risen from around $3 to more than $4.50 a gallon, and citizens are not happy. A New York Fed measure of global supply chain pressure, meanwhile, jumped to the highest level since July of 2022, when manufacturing chains were still snarled from the pandemic and the world faced a systemic surge in prices.

“This is also underlying inflation that we need to worry about,” Musalem said, adding that business executives were telling him that higher prices for aluminium, helium, diesel fuel and other industrial inputs “will all be disruptive … There’s a confidence effect” that may suppress hiring even as it risks higher price increases.

The net result for the Fed may be an extended pause in any change to a policy rate that has been in the 3.50%-3.75% range since December, stalling what had been anticipated continued monetary policy easing and complicating incoming Fed Chair Kevin Warsh’s ability to deliver the rate cuts President Donald Trump has said he expects.

Musalem and Goolsbee are not currently voting members of the rate-setting policy committee (FOMC), but their comments demonstrate what Fed Chair Jerome Powell said is movement at the “centre” of the central bank towards the possibility that rate hikes might be needed to combat inflation risks.The Personal Consumption Expenditures Price Index, used by the Fed to set its inflation target, rose to 3.5% in March from 2.8% in the prior month, while underlying “core” inflation that excludes among other things the recent swings in energy prices, rose to 3.2% from 3.0% in February.

Stagflation is the combination of three economic conditions occurring simultaneously:

The term was coined in the 1960s by British politician Iain Macleod, combining “stagnation” and “inflation.”

It is particularly troubling for policymakers because the two main problems are contradictory to treat. Normally, central banks raise interest rates to fight inflation, but higher rates also slow growth and increase unemployment, worsening stagnation. Conversely, cutting rates to stimulate growth risks making inflation even worse. The central bank is essentially caught in a trap with no clean solution.

The classic historical example is the 1970s, triggered by the 1973 OPEC oil embargo, when oil prices quadrupled almost overnight. This is directly relevant to the current situation because the mechanism is identical: a supply-side energy shock pushes up the cost of almost everything (inflation), while simultaneously squeezing household disposable income and corporate margins, slowing economic activity (stagnation).

Why it is relevant right now is precisely what the FOMC minutes, the ECB, and the SARB are all grappling with in the context of the Iran war and Hormuz disruption. The oil shock is pushing inflation higher at exactly the moment when growth is fragile, leaving every major central bank facing that same impossible choice the 1970s made famous.

With US inflation lodged about a percentage point above the Fed’s 2% target and expectations it may move higher, investors see little chance the U.S. central bank will cut rates for perhaps another year or more.

The US Consumer Price Index for April, due to be released next week, is expected to show a further acceleration. The U.S. employment report for April, scheduled for release on Friday, is expected to show the unemployment rate remained unchanged at 4.3%.

Author: Dawn Ridler

When I started my investment career, institutional fund management was beginning to align with international norms. South Africa had emerged from its days under Apartheid, and the industry was fast adopting trends globally. With that came a rethink of what has become known as a style-based approach to fund management.

The trend in part was driven by what is known as Discretionary Fund Managers’ or DFM’s need for fund managers’ specific skills. DFM’s are fund management businesses that combine the skills of underlying fund managers into a strategy or a portfolio into which an investor can place money. You may also know them as multi-managers.

Their strategies are sold on the pretence that they provide superior risk-adjusted returns over time, and often are marketed by a financial planning community. It was this need that transformed fund managers in South Africa from generalists to specialists. DFM’s wanted fund managers to provide them with their specialist skills only in a specific asset class. This allowed the DFM to combine this skill with other managers to create an investable strategy.

Concepts such as value and growth were born. It was thought that some managers prefer cheap assets and were thus branded as “value” whereas their counterparts which didn’t mind holding assets as they became more expensive were “growth” orientated. With time, other flavours such as “growth at a reasonable price” were born. That was more than 20 years ago, and what one realises with time is that value and growth are actually 2 sides of the same coin. Its not evident when one looks at an attribution system but once you start analysing equities one comes to realise that value is the price one pays for future growth.

Now, that may seem like a no-brainer, but the institutional industry didn’t see it that way for a long time. I saw crazy moments where managers were forced to sell shares that, in the DFM’s opinion, had become growth-oriented. The term for this was style drift and it basically meant that if the specific portfolio didn’t adhere to the initial parameters that was set for it, the fund could negatively affect the whole strategy.

But analyse enough equities and one comes to realise that the job at hand is placing a value on the efforts of a management team that is attempting to create growth.

Pricing future growth correctly is what makes for a good fund manager. Some companies have the enviable position of a business model with an annuity nature, providing management with a steady stream of cash, whereas others need to innovate and sell continuously to achieve this.

How this cash is spent is what creates the future growth.

Cheap companies which are trading at low valuations are invariably priced at these levels because the market questions their future growth. Expensive companies are recognised by the market for their ability to continue to grow. The challenge for fund managers is to either recognise growth where the market has failed to do so or to pay a fair price and let the growth lift the share price over time. Both are equally difficult to do because a company’s ability to defend its business from the onslaught of competition is difficult.

In the industry, we think of companies with moats. Narrow moat companies tend to earn lower returns on invested capital, whereas large moat companies tend to earn higher rates. But moats wane over time as competition intensifies around wide moat players. Everyone is attempting to earn superior returns, and there is nothing quite as attractive as a competitor’s high rate of returns. So, moats erode with time and owning equities requires an understanding of the longevity of such a moat. Paying a high price for a company that can defend its moat for the next few decades may actually be a value opportunity. Value is what you pay, growth is what you get. They aren’t separate concepts; they are very much interlinked.

Author: Cobie Le Grange

EXCHANGE RATES and other Indices:

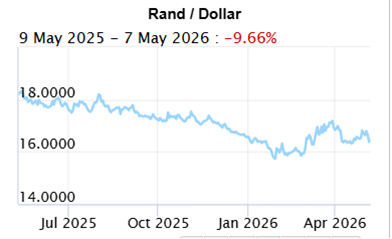

The Rand/Dollar closed at R16.39 (R16.63, R16.29, R16.41, R17.07, R17.06, R16.89, R16.55, R15.93, R16.01, R15.96, R16,03, R16.15, R16.10, R16.50, …R16.91, R17.13, R17.36, R17.13,16.52 R17.27, R17.31, R17.25, R17.38, R17.50, R17.22 , R17.35, R17.33, R17.37, R17.58, R17.65, R17.44, R17.61, R17.74, R18.15,R17.76, R17.72, R17.90, R17.58, R17.89, R17.99, R17.92, R17.77, R17.95, R17.88)

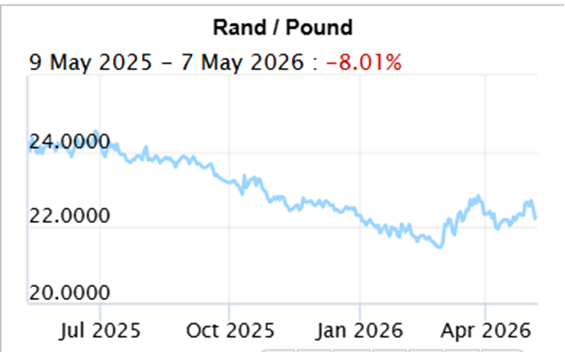

The Rand/Pound closed at R22.30 (R22.56, R22.35, R22.02, R22.09, R22.77, R22.76, R22.35, R22.20, R21.48, R21.59, R21.78, R21,82, R22.11, R21.97, R22.13, …R22.57, R22.68, R22.74, R22.56, R22.69, R22.76, R22.96, R23.34, R23.37, R23.19, R23.22, R23.35, R23.55, R23.73, R23.84, R23.53, R23.84, R23.84, R24.09, R23.88, R23.76, R24.22, R24.08, R24.49, R24.22, R24.35, R24.05, R24.18)

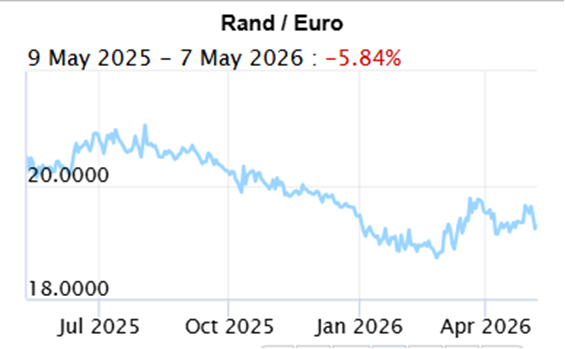

The Rand/Euro closed the week at R19.29 (R19.48, R19.37, R19.17, R19.24, R19.70, R19.77, R19.33, R19.23, R18.80, R18.87, R18.94, R18.93, R19.14, R19.04, R19.20, …R19.68, R19.86, R19.99, R19.96, R19.98, R20.02, R20.06, R20.26, R20.33, R 20.22, R20.30, R20.35, R20.38, R20.61, R20.62, R20.44, R20.56, R20.64, R21.04, R20.86, R20.61, R20.93, R 20.70, R20.91, R20.74, R20.68, R20.24, R20,37)

Brent Crude: Closed the week $101.29 ($108.83, $105.33, $90.38, $95.20, $107.88, $112.36, $103.14, $92.88, $73.19, $71.76, $67.75, $68,05, $69.32, $65.88, $63.34, …$63.71, $63.19, $62.42, $63.94, $63.61 $64.66, $65.04, $61.27, $62.14, $64.28, $69.67, $66.57, $66.80, $65.52, $67.38, $67.73, $66.08, $66.07, $69.46, $68.29, $69.21, $70.58, $68.27, $67.39, $77.27, $74.38, $66.56, $62.61, $65.41)

Bitcoin closed at $80,733 ($78,204, $78,049.98, $75,519, $70,904, $68,691 , $68,586, $70,869, $67,310, $63,534, $68,04, $69,649, $68,553, $81,301, $89,295, $90,585, … $90,809, $86,334, $94,990, $101,562, $109.936, $112,492, $106,849, $111,888, $124,858, $109,446, $115,838, $115,770, $110,752, $108,923, $114,916, $117,371, $118,043, $113,608, $118,139, $118,214, $117,871, $108,056, $107,461, $103,455)

Articles and Blogs:

Legacy Series Part 4 NEW

Legacy Series part 3

Legacy Series Part 2

Legacy Series Part 1

Holiday checklist

Next year – Action Plan

Next year – Vision, Mission etc

Medical Risk Mitigation

Next Year – Consolidation

Abdication or diversification?

Carbo-loading your retirement Spoiled for choice

Who needs a plan anyway

8 questions you need to ask about retirement

What to do when interest rates drop

How to survive volatility in your investments

What to do when interest rates drop

Difficult Financial Conversations

Financial Implications of Longevity

Kick Start Your Own Retirement Plan

You matter more than your kids in retirement

To catch a falling knife

Income at retirement

2025 Budget

Apportioning blame for your financial state

Tempering fear and greed

New Year’s resolutions over? Try a Wealth Bingo Card instead.

Wills and Estate Planning (comprehensive 3 in one post)

Pre-retirement – The make-or-break moments

Some unconventional thoughts on wealth and risk management

Wealth creation is a balancing act over time

Wealth traps waiting for unsuspecting entrepreneurs

Two Pot pension system demystified

Cobie Legrange and Dawn Ridler,

Rexsolom Invest, Licensed FSP 45521.

Email: cobie@rexsolom.co.za, dawn@rexsolom.co.za

Website: rexsolom.co.za, wealthecology.co.za