Too Busy, Got Better Things to Do? Read the Summary…

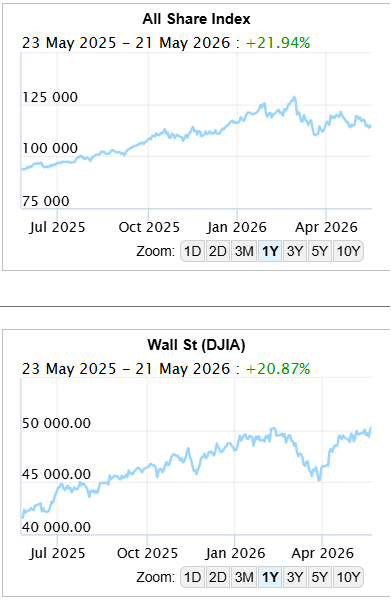

This Week’s Roundup: SA inflation jumped to 4.0% in April, markets pricing two rate hikes by year-end with a 25bp hike expected at the May 28 MPC meeting. IIF cut SA’s 2026 growth forecast to 1.3%. Q1 trade surplus tripled to R77bn. US deficit projected at 5.8% of GDP, rising to 6.7% by 2036. Brent near $105/barrel complicates Fed easing. S&P 500 remains 12% up for the year despite volatility. Eurozone inflation at 3%, three ECB hikes priced in for 2026.

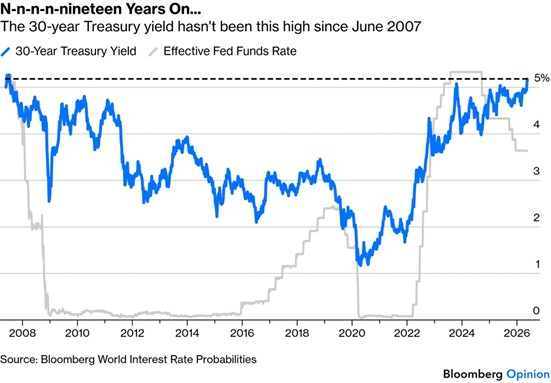

Bondage – and not in a good way: 30-year US Treasury yields hit 5.19% — last seen just before the GFC in June 2007. Parallels are unsettling: equities roaring, fund managers at record equity allocations, and the CAPE ratio at 39.6, only exceeded at the dot-com peak. Government debt has doubled to 120% of GDP since 2007, making higher rates far more dangerous. The wildcard difference is AI — a genuine economic force that wasn’t present in prior cycles.

Emerging Markets : EM classifications vary by institution, with China’s status actively debated. India’s 10-year yield sits at 7.1% as the RBI weighs rate hikes to defend the rupee. SA’s 10-year yield is at 8.91%, reflecting 4% inflation driven almost entirely by imported oil price pressures.

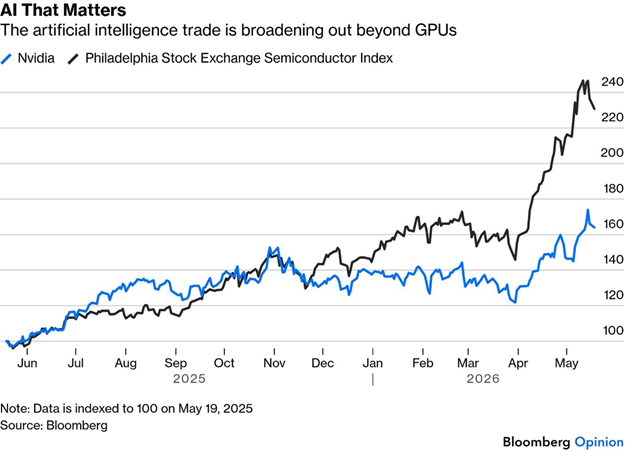

NVIDIA – the key to everything AI: NVIDIA posted 85% revenue growth, $215.9bn full-year revenue and an $80bn buyback — then was upstaged by SpaceX’s IPO. China access remains complicated despite some H200 approvals, with Huawei’s Ascend chips advancing fast. The broader SOX index is up 60% year to date as the AI trade widens beyond NVIDIA.

Warsh and Peace: Kevin Warsh sworn in as Fed Chair. Nominated as a dove, the Iran war has shifted expectations — fed funds now seen above 4% next summer. The FOMC is more hawkish than previously thought; Warsh’s realistic best outcome for Trump is maintaining the current pause on rates.

Joburg Woes: Africa’s financial capital is functionally broken — 10 mayors since 2016, an 18-party coalition, rampant corruption and a deepening financial crisis. Treasury is threatening funding cuts, and Eskom is threatening power cuts over unpaid debt. The private sector is filling basic service gaps. November elections unlikely to deliver a majority. No bottom in sight.

Objectives, Incomes: Investors are often their own worst enemy. Compounding rewards patience but is invisible in the short term, causing many to abandon sound strategies too early. Excessive portfolio withdrawals in retirement erode capital permanently. The solution: understand what you own, why you own it, and treat your capital with long-term care.

Bondage – and not in a good way

It’s been a while since the US has been here, and it’s not a good place to be. The yield on 30-year Treasury bonds rose Tuesday to 5.19% for the first time since June 2007:

Back in June 2007, the concern was that rates at these levels might burst higher, bringing down the then-booming stock market and putting unbearable pressure on credit markets. It turned out that a bond selloff did indeed signal the end of an era for equities. Within weeks, subprime credit was selling, two Bear Stearns hedge funds collapsed, and the long spiral into what we now call the Global Financial Crisis had begun. (Why? If you can get a ‘risk-free’ return of 5%,why would you risk everything in a risky bubble market?)

Could we be seeing the same scenario today?

The earnings now produced by US companies are impressive (just like banks’ earnings in 2007), but will financial conditions let this continue? No two market conditions are ever the same, but these seem to be written in the same font (and this time it’s Trump Comic Sans).

Now as then, equities are roaring despite the warnings from bonds.

The latest Bank of America survey of global fund managers shows that they had increased their equity allocations last month by the most in history. Now as then, they’re buying stocks despite concerns about the economy.

June 2007 was characterised by a period of peak economic optimism and robust risk appetite, right before the initial tremors of the subprime mortgage crisis. It reflected a global economy in its late-cycle expansion, in which institutional investors heavily favoured equities over cash and fixed income.

It’s concerning that corporate balance sheets were “perceived as healthy” on the eve of an epochal credit crisis. Then, as now, there was optimism about corporate profits.

Of course, there are differences. The Fed was on hold at the top of a tightening cycle then; it’s now on a temporary hold during a loosening cycle, but appears likely to have to hike before it cuts.

Government debt has risen in round numbers to 120% of gross domestic product from 60% then, making higher interest rates much more of a problem for Uncle Sam. And while 19 years ago the Iraq war had become a miserable fact of life, investors are still assimilating what is going on in Iran; it’s shifted expectations for oil prices and financial conditions sharply upward.

And stocks were cheaper the last time bond yields were this high. At that point, the cyclically adjusted price/earnings multiple was 27.4; it’s now 39.6. It’s only ever been higher than now for the top 20 months of the internet bubble, which burst in March 2000.

The combination of equities like 2000 and bonds like 2007 is unnerving. The big difference is that this time, there is a genuine force powering positively through the economy — the artificial intelligence revolution. Nothing remotely comparable was afoot in 2007. If AI delivers as hoped, people could live to think that stocks were fairly valued in May 2026. But much is expected of AI – will it show its promise – in time to keep all this euphoria afloat?

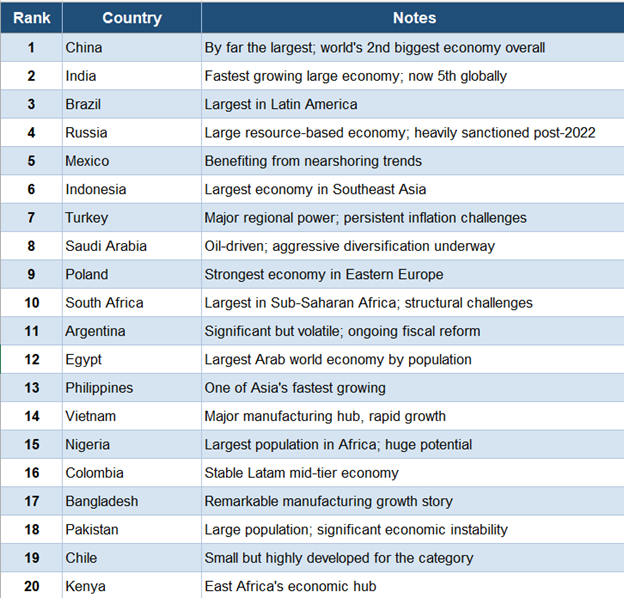

Emerging markets play an important role in global economics and investment portfolios.

Here’s a ranking of the major emerging economies, most commonly grouped and ranked by GDP (nominal) as the primary measure of economic scale and influence:

A Few Important Caveats: Groupings vary by institution. The MSCI, IMF, FTSE Russell, and World Bank each classify emerging economies differently. Some lists include around 24 countries, others over 40. China’s status is debated. Many analysts now argue China has graduated beyond “emerging” given its sheer size, though it retains structural characteristics (capital controls, state dominance) that keep it in the category for index purposes.

BRICS expansion (now including UAE, Ethiopia, Egypt, Iran, and Indonesia as of 2024–2025) has reshaped how the bloc of large emerging economies is discussed politically. South Africa, while ranked relatively low by GDP, punches above its weight as the most sophisticated financial market on the African continent and remains the primary gateway for institutional investment into Africa. With all the talk in this newsletter around government bonds, let’s have a look at RSA and India, just as examples.

The yield on India’s 10-year G-Sec is hovering around 7.1%. Sentiment was driven primarily by reports that the Reserve Bank of India is weighing all options to support the rupee, including a possible rate hike, additional currency swap operations, and steps to attract overseas dollar inflows. The rupee’s slide toward 97 per dollar has intensified internal discussions at the RBI, keeping policy tightening in focus ahead of the June 3–5 monetary policy meeting. Additional support came from a rise in US Treasury yields, with the 10-year note edging up to around 4.59% as markets tracked firmer oil prices and Fed minutes that reinforced a cautious but still inflation-sensitive stance, keeping expectations of potential future tightening in play.

South Africa’s 10-year bond yield was around 8.91% last week, holding close to the highest since early April, after local inflation data signalled rising pressures from the Iran-driven energy shock that could lead to higher interest rates. Inflation accelerated to 4% in April, the highest since August 2024, from 3% in March and slightly above forecasts of 3.9%. It now sits well above the central bank’s 3% target and is expected to climb further in the coming months. This is almost exclusively the result of ‘imported’ inflation from the surge in the oil price. Economists say that even if a peace deal is reached, crude oil prices are unlikely to quickly return to pre-war levels and should continue to exert upward pressure. The South African Reserve Bank is increasingly expected to raise rates by at least 25 basis points to 7% at its May 28 meeting, its first hike since May 2023. Governor Lesetja Kganyago recently cautioned that the central bank stands ready to act if price pressures intensify and stressed the need to contain second-round effects.

NVIDIA – the key to everything AI

An epic earnings season for the hyperscalers that we spoke about a few weeks back is set for its great operatic encore. NVIDIA Corp. steps up after trading on Wednesday with the ultimate numbers on the durability of the gravity-defying AI trade. Thanks to the hyperscalers’ splurge on AI datacenters, the world’s biggest chipmaker has consistently posted healthy margins. That trajectory won’t change as long as mega caps keep building. We can only watch in wonder, and perhaps some trepidation – because if this falls, then it’s not going to be pretty.

Wednesday’s earnings should offer a glimpse into the steam left in its engine, which cannot run in perpetuity. Analysts project revenue to surge 79% to $78.9 billion, with datacenter revenues representing roughly 90% of that growth.

Its chief executive, Jensen Huang, accompanied President Donald Trump to China last week, and says access to Beijing is within reach. (He spent most of his free time on a ‘side quest’ to the streets of Beijing, connecting with locals and trying local cuisine (he is a self-confessed foodie) – a smart move on his part. None of the execs got any time with Xi but was dumped with low-ranking officials instead. That would build on Trump’s December decision to allow the sale of H200 chips to Chinese firms. This doesn’t mean that China is low-hanging fruit.

Restoring access to China is far more complicated. Despite recent reports that about 10 Chinese firms were granted access to buy H200 chips, no deals have been reached so far. On top of that, the deal structure itself creates confusion. There is a 25% revenue cut and a requirement that chips pass through a US lab, which could delay or complicate transactions. This could give the Chinese more reason to justify blocking any deals. Further, US-imposed restrictions have fast-tracked domestic ingenuity, with Huawei and others poised to fill the gap. The Chinese company expects AI chip revenue to climb dramatically with its latest Ascend model entering mass production. This may mean China’s domestic competitors can move on without Nvidia.

Beyond that, there’s broad confidence that Nvidia can continue its remarkable outperformance since ChatGPT jump-started the AI trade four years ago. It has beaten earnings expectations in 18 of its last 20 reports and exceeded revenue estimates in 19, suggesting a high but not insurmountable bar. Clearing it will depend on hyperscalers’ outlays.

NVIDIA’s stock price movements have been led by a combination of its evolving AI product roadmap, along with consistent “beat and raise” results. This leadership is not without blemish. Since last year’s buzz around sovereign AI and neoclouds, no new narrative has emerged.

Sovereign AI

Sovereign AI refers to a nation’s or region’s strategy to build and control its own AI capabilities, rather than relying on foreign technology companies, models, or infrastructure. The core idea is AI self-sufficiency as a matter of national interest.

This typically involves:

Countries actively pursuing sovereign AI strategies include the UAE (Falcon models), France (Mistral), India, Saudi Arabia, and various EU member states collectively. The EU’s broader digital sovereignty push is a major driver. NVIDIA has been a vocal proponent of the concept, as it positions itself to sell GPU infrastructure to governments directly.

Neoclouds

Neoclouds are a new category of cloud infrastructure providers that have emerged specifically to meet AI compute demand — distinct from traditional hyperscalers (AWS, Azure, Google Cloud).

Examples include CoreWeave, Lambda Labs, Crusoe, and Voltage Park. They’ve grown rapidly because hyperscalers couldn’t provision AI-grade GPUs fast enough during the 2023–2024 demand surge.

The two concepts intersect significantly. Governments pursuing sovereign AI strategies often turn to neoclouds or neocloud-style domestic providers to build national GPU capacity, rather than routing sensitive workloads through US hyperscalers. This has made sovereign AI a meaningful revenue opportunity for neocloud players and for NVIDIA, which supplies the underlying hardware either way.

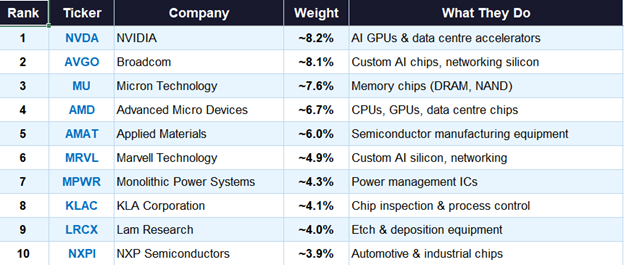

Nvidia is no longer the top dog when it comes to stock performance. The AI trade has broadened from GPU makers to SOX index companies in networking, memory chips and power management:

NVIDIA & Broadcom dominate the AI narrative. NVIDIA reported revenue of $215.9 billion for fiscal year 2026, up 65% year-on-year, with data centre revenue reaching $194 billion. Broadcom’s AI semiconductor revenue is projected to exceed $30 billion in fiscal year 2026.

The index has been a strong performer. SOXX is up roughly 60% year to date, with AI infrastructure demand driving the hardware cycle as spending continues to widen across accelerators, CPUs, networking chips, memory, and manufacturing equipment.

AMD is gaining ground. AMD’s Q1 2026 revenue came in at $10.25 billion, up 38% year-on-year, with the Data Centre segment delivering $5.78 billion, a 57% jump.

The SOX is essentially a barometer of the global AI buildout, virtually every company in it is a direct beneficiary of the infrastructure spending wave.

The role of Capex in share valuation

The Nvidia excitement highlights a strange new development: Investors have decided they like companies making capital expenditures. It wasn’t always thus. Generally, shareholders prefer firms to pay them cash through dividends or buybacks, so they don’t waste it on vanity expansion projects.

This is the established theory of shareholder value, and it’s borne out empirically.

Markets are driven by narratives; George Soros, Robert Shiller and others tell us that, and it’s true. We also love to attack hubris (excessive pride, arrogance), a sin ever since the Greek tragedians coined the word.

AOL’s merger with TimeWarner was the prideful peak of the dot-com bubble, Citi’s CEO disastrously called the top in 2007 by saying “as long as the music’s playing, you’ve got to get up and dance,” and Glencore’s IPO called the end to the bull market in metals in 2011.

What will hindsight make of Wednesday’s Nvidia earnings?

NVIDIA Corp. announced 85% sales growth and 62% margins, and its stock dropped because investors wanted more; then SpaceX announced an IPO in which Elon Musk keeps 85%, with plans for data centres in space and asteroid mining (I kid you not).

SpaceX’s prospectus is literally jaw-dropping, and it rendered Nvidia’s incredibly strong earnings a non-event:

The focus has shifted to whether the chipmaker can keep its dominant share of the artificial intelligence “cake.” NVIDIA’s revenue growth shows that the momentum of the AI data-centre buildout is if anything, accelerating. The company rammed home its confidence with an additional $80 billion in share repurchases, in what ranks among the largest capital return commitments in corporate history. And profit margins continue to tower over industry benchmarks:

Wednesday’s earnings suggested Nvidia’s grip on pricing remains remarkably firm. Gross margins came broadly in line with analyst expectations. It still has pricing power, even if the latest sales forecast wasn’t as bullish as markets had hoped.

So far, Nvidia’s pipeline of increasingly powerful chips is preserving its edge.

Chief executive Jensen Huang says the Vera Rubin AI supercomputing platform, built around next-generation processors, remains on track to ship in the second half of the year. It will likely remain supply-constrained, which should be good news for investors on pricing, though less welcome for customers.

All of this contributes to a narrative that fits a market top (or alternatively, fits a market that shoots to the moon and thence to Mars). Valuation can never help with timing, but might show we’re close to a peak. But the catalysts are lacking. Hikes in rates are a necessary condition for a major market top. US rates are falling (but, to be fair, have been on hold for a few months)

Another necessary condition is an inverted yield curve, when short rates are higher than longer-term. That happened in 2022, when rate hikes provided a catalyst for the start of a bear market. But that inversion is over.

Circumstantial evidence proves nothing, but it looks like 2022 was the moment when the next secular bear market was fated to happen, and ChatGPT thwarted destiny. AI is of macroeconomic importance. While earnings keep growing on the scale of Nvidia, and optimism remains strong enough to persuade people to buy IPO shares in SpaceX, Anthropic or OpenAI on what seem to be terrible terms, it’s hard for the market to go down.

Then we run into market logic’s final obstacle. Over history, whenever earnings have risen like this, they have always brought interest rates up with them. It will be hard to avoid a bear market if the Fed hikes rates. And on that subject, the Fed is about to change hands…

On Friday, with unusual pageantry, President Donald Trump swore in Kevin Warsh to chair the Federal Reserve.

Warsh, 56, will lead the Fed at a time when its independence has come under scrutiny amid political pressure on the historically non-partisan institution.

US President Donald Trump, aware of that critique, in his opening remarks said, “I want Kevin to be totally independent and do a great job. Don’t look at me and don’t look at anybody. Just do your own job”.

During his confirmation hearing before the Senate Banking Committee, ahead of a vote by the full Senate, Democratic Senator Elizabeth Warren accused Warsh of being a “sock puppet” for Trump. Warsh denied the allegations and said he would remain independent in his monetary policy decisions.

When Joe Biden was president, Warsh advocated against cutting interest rates, but changed his tune when Trump took office. In December 2025, Trump said that he would only appoint someone to lead the central bank who agreed with him on cutting rates.

Regardless, Warsh cannot unilaterally make policy decisions. He is one of 12 voting members.

The first policy meeting Warsh will lead will be on June 16-17.

It happens just as the Iran war seems to have swallowed the entire saga over choosing Warsh, along with the pitched debate over how independent the central bank should be. But it still matters.

When nominated in January, Warsh was a dove who intended to cut rates. A month later, war broke out in Iran, and with it changed the entire nature of his job. On Feb. 27, futures implied that the fed funds rate would be about 2.8% next summer; now, even with Warsh in place, it’s expected to top 4%.

The Federal Open Market Committee that Warsh will now chair appears from the minutes of Jerome Powell’s final meeting to be comfortable with these expectations, and more hawkish than previously thought. The Fed is coy about the exact numbers of votes, but word choices paint a picture of a building consensus for tightening.

The sole change in the committee will see Warsh replace Stephen Miran, its most extreme dove. So his chances to corral a majority for cuts look negligible. He will have delivered for Trump if he can just dissuade his colleagues from hiking. The general feeling is that no June hike is essentially a rate cut.

He does, however, have more weapons at his disposal as chairman. He gets to assign his colleagues to the committee and appoint the Fed’s staff of economists. Only time will tell if he is his own man or yet another Trump sock-puppet.

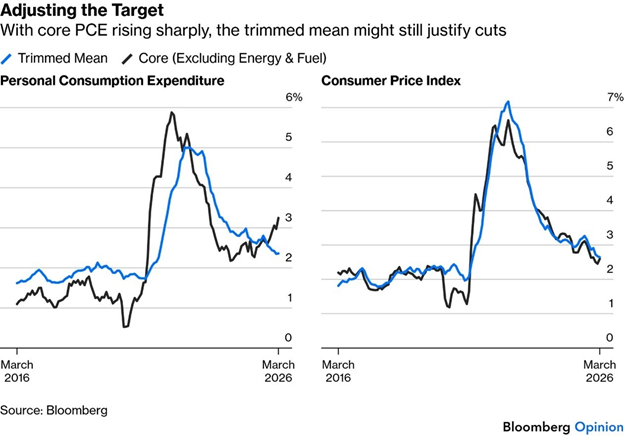

He also says he prefers trimmed-mean inflation (in which outlying components are excluded and the average is taken of the rest) to core measures, most closely watched at present, that exclude food and fuel.

To be fair, there’s a good statistical case for this. It’s also very convenient for doves to make the change now, because core PCE is surging higher as the trimmed mean falls.

It boils down to lies, damn lies and statistics all over again, but for those of you who are interested in mathematical shenanigans, this is really quite interesting… (and not necessarily going to help the doves either). The best that Trump can hope for is a continued ‘pause’ rather than a cut, and that is, thanks to an own-goal called Excursion Epic Epstein Fury. Hiking rates would intensify the risk of stagflation; there are arguments to stay on hold. But many worry that Trump’s position could still have a malignant impact.

I came across this interesting article on Johannesburg on Bloomberg. It could be behind a paywall, so here is a summary.

Johannesburg has more millionaires than anywhere else in Africa, hosts the continent’s biggest stock exchange, and generates roughly a third of South Africa’s economic output. Yet the city is functionally broken.

The symptoms are everywhere: crumbling infrastructure, frequent water and power outages, potholed streets, half-built transit projects abandoned for over a decade, abandoned buildings taken over by armed gangs, and even the city’s famous art gallery is in disrepair — its Monets and Picassos moved out for safekeeping.

The root cause is political. Since the ANC lost its majority in 2016, the city has cycled through 10 mayors and is now governed by a fractious coalition of 18 political parties. The constant instability means no consistent policy, rampant corruption, wasteful spending, and every decision becoming an opportunity for extraction rather than governance.

The financial crisis is now acute.

The national Finance Minister has threatened to cut R480 million in funding unless the city addresses $1.4 billion in wasteful spending. The state power utility has publicly threatened to cut Johannesburg’s electricity over a $320 million unpaid debt. The city has also failed to collect billions in outstanding debt of its own.

The private sector is plugging gaps — Discovery is fixing potholes, a mining company is putting up streetlights, and a bank is storing the art gallery’s masterpieces. The outlook is grim. With November local elections approaching and polls suggesting yet another hung council, academics and business leaders don’t see a turnaround coming. As one researcher put it: “I am not sure that we have hit bottom yet.” Just on Thursday, a 19-day water outage was announced (starting next weekend) for yet more ‘maintenance’.

Author: Dawn Ridler

This week, I thought I would forgo my usual technical piece in favour of some thoughts on investor behaviour. These can be among the biggest challenges when managing a client portfolio. It’s meant to act as a conversation piece and to provoke some thought.

We are often our own worst enemy. I have seen more value destroyed by investor actions than by portfolio action. A patient investor stands to gain the benefit of long-term compounded gains. We all know it, but few of us follow through. Those who do tend to be calm, assured individuals who can act rationally. They tend not to watch their portfolios too closely because they know that month-on-month performance is really just noise. More important to watch how years and decades roll into compounded returns. But our obsession with having it all now, unrealistic income requirements or the negative voices of friends and family are all enemies of long-term portfolio gains. I have experienced this firsthand many times in my career.

Most investors don’t truly understand compounding.

When we invest, we prefer companies which exhibit a high or growing rate of reinvestment. These companies have a track record of reinvesting profits to gain further returns. If this in turn drives a larger moat with which the company can defend its business model, one has truly found an amazing opportunity. These companies tend to grow through time and provide compounding power to a portfolio. You won’t see it in year 1 or 2, but given a long enough period, the compounding becomes evident.

The problem is that we want the market to agree with our assumptions about these businesses today or at least soon. If the absence of that, investors start questioning the investment thesis. On numerous occasions, investors would single out a holding and question why it hasn’t delivered a return yet. The reality is that other market forces are at play whilst you are waiting for a share price to rise. Liquidity, rates, exchange rates, newsflow or even a war can derail returns in the short term. But if you are prepared to look a bit further out, a day will come when the market starts understanding the value in owning the company. This is when gains start materialising. Can you patiently wait alongside the fund manager for this to occur? If you can, the gains are well deserved and all yours. But if you’re looking to chop and change investment strategies because your current choice just isn’t working fast enough, not only are you incurring the cost of change, but you are in effect destroying value that you have built through time.

Don’t get me wrong, there is a place and time to change strategy. Consider a change in circumstances or risk appetite as examples of this. But these tend to be “one-in-a-while” decisions. The moral of the story is to understand what you are invested in. If that philosophy appeals to you, there will be little reason to change, and you may very well save yourself money.

Generally, investors, once they are retired, will start living within the means that their money provides. What I mean by that is that investors will tend to listen to their advisors to ensure that they don’t place too great an income burden on their portfolios. Generally, this is the case. But as with anything, there are exceptions. From large one-off payments to ongoing large withdrawals, these can all deplete portfolios over time. What these investors are doing, in essence, is robbing their future self of an income.

There may be legitimate reasons for doing this. There may be individuals who require support in a family, a divorce or a large once-off purchase that is required. What is important is that these drawdowns are thoughtfully considered and done in the light of understanding their long-term implications. As an example, there may be a higher income requirement today, but this will be adjusted down within a reasonable time to allow the portfolio to recover from the larger drawdown.

This is reasonable. What is unreasonable is drawing from a portfolio without giving it a chance to recover.

You are, in essence, killing your own capital by doing this. Other than getting lucky with returns, no well-diversified portfolio can deliver on these requirements. This is a one-way street to long-term poverty. And as much as we would all like more money to retire on, I have seen individuals with modest portfolios cope just fine, whereas others with far more means have an insatiable desire to spend more every day. Don’t get me wrong, I am not suggesting one becomes a miser. There is a reason miser and misery rhymes! What I am suggesting is that there is thought given to lifestyle needs by treating one’s assets as if they were a member of the family.

Author: Cobie Le Grange

EXCHANGE RATES and other Indices:

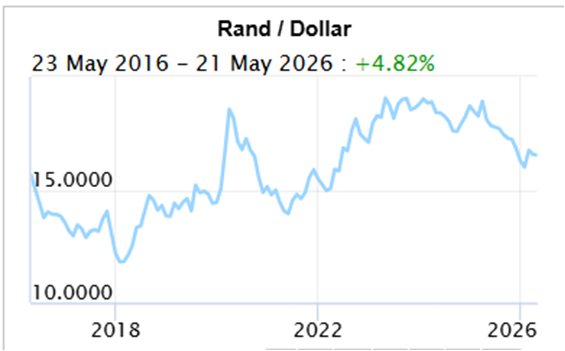

The Rand/Dollar closed at R16.46 (R16.68, R16.39, R16.63, R16.29, R16.41, R17.07, R17.06, R16.89, R16.55, R15.93, R16.01, R15.96, R16,03, R16.15, R16.10, R16.50, …R16.91, R17.13, R17.36, R17.13,16.52 R17.27, R17.31, R17.25, R17.38, R17.50, R17.22 , R17.35, R17.33, R17.37, R17.58, R17.65, R17.44, R17.61, R17.74, R18.15,R17.76, R17.72, R17.90, R17.58, R17.89, R17.99, R17.92, R17.77, R17.95, R17.88)

The Rand/Pound closed at R22.09 (R22.21, R22.30, R22.56, R22.35, R22.02, R22.09, R22.77, R22.76, R22.35, R22.20, R21.48, R21.59, R21.78, R21,82, R22.11, R21.97, R22.13, …R22.57, R22.68, R22.74, R22.56, R22.69, R22.76, R22.96, R23.34, R23.37, R23.19, R23.22, R23.35, R23.55, R23.73, R23.84, R23.53, R23.84, R23.84, R24.09, R23.88, R23.76, R24.22, R24.08, R24.49, R24.22, R24.35, R24.05, R24.18)

The Rand/Euro closed the week at R19.11 (R19.38, R19.29, R19.48, R19.37, R19.17, R19.24, R19.70, R19.77, R19.33, R19.23, R18.80, R18.87, R18.94, R18.93, R19.14, R19.04, R19.20, …R19.68, R19.86, R19.99, R19.96, R19.98, R20.02, R20.06, R20.26, R20.33, R 20.22, R20.30, R20.35, R20.38, R20.61, R20.62, R20.44, R20.56, R20.64, R21.04, R20.86, R20.61, R20.93, R 20.70, R20.91, R20.74, R20.68, R20.24, R20,37)

Brent Crude: Closed the week $104,24 ($109.26, $101.29, $108.83, $105.33, $90.38, $95.20, $107.88, $112.36, $103.14, $92.88, $73.19, $71.76, $67.75, $68,05, $69.32, $65.88, $63.34, …$63.71, $63.19, $62.42, $63.94, $63.61 $64.66, $65.04, $61.27, $62.14, $64.28, $69.67, $66.57, $66.80, $65.52, $67.38, $67.73, $66.08, $66.07, $69.46, $68.29, $69.21, $70.58, $68.27, $67.39, $77.27, $74.38, $66.56, $62.61, $65.41)

Bitcoin closed at $74,559 ($77,879, $80,733, $78,204, $78,049.98, $75,519, $70,904, $68,691 , $68,586, $70,869, $67,310, $63,534, $68,04, $69,649, $68,553, $81,301, $89,295, $90,585, … $90,809, $86,334, $94,990, $101,562, $109.936, $112,492, $106,849, $111,888, $124,858, $109,446, $115,838, $115,770, $110,752, $108,923, $114,916, $117,371, $118,043, $113,608, $118,139, $118,214, $117,871, $108,056, $107,461, $103,455)

Articles and Blogs:

Legacy Series Part 4 NEW

Legacy Series part 3

Legacy Series Part 2

Legacy Series Part 1

Holiday checklist

Next year – Action Plan

Next year – Vision, Mission etc

Medical Risk Mitigation

Next Year – Consolidation

Abdication or diversification?

Carbo-loading your retirement Spoiled for choice

Who needs a plan anyway

8 questions you need to ask about retirement

What to do when interest rates drop

How to survive volatility in your investments

What to do when interest rates drop

Difficult Financial Conversations

Financial Implications of Longevity

Kick Start Your Own Retirement Plan

You matter more than your kids in retirement

To catch a falling knife

Income at retirement

2025 Budget

Apportioning blame for your financial state

Tempering fear and greed

New Year’s resolutions over? Try a Wealth Bingo Card instead.

Wills and Estate Planning (comprehensive 3 in one post)

Pre-retirement – The make-or-break moments

Some unconventional thoughts on wealth and risk management

Wealth creation is a balancing act over time

Wealth traps waiting for unsuspecting entrepreneurs

Two Pot pension system demystified

Cobie Legrange and Dawn Ridler,

Rexsolom Invest, Licensed FSP 45521.

Email: cobie@rexsolom.co.za, dawn@rexsolom.co.za

Website: rexsolom.co.za, wealthecology.co.za