Too Busy? Got Better Things to Do? Read the Summary…

This Week’s Roundup: SA’s Q1 GDP beat forecasts at 0.5%, with Fitch delivering its first credit upgrade in 21 years (BB- to BB). Petrol is 35% above January levels, pushing CPI to 4.0%. US May CPI hit 4.2% on soaring energy costs, with PPI at 6.5% signalling more pipeline inflation to come. Payrolls surprised strongly at 172,000. The ECB hiked 25bp to 2.25%. Brent fell to ~$89 on ceasefire optimism; gold hit a 6-month low.

US Inflation – Increasingly Worrying: Energy drives the headline, but the detail is more troubling: supercore, sticky prices, trimmed mean and median inflation are all rising. Services remain stubbornly high. Rate cuts are off the table, and with midterms four months away, affordability is becoming a defining political issue.

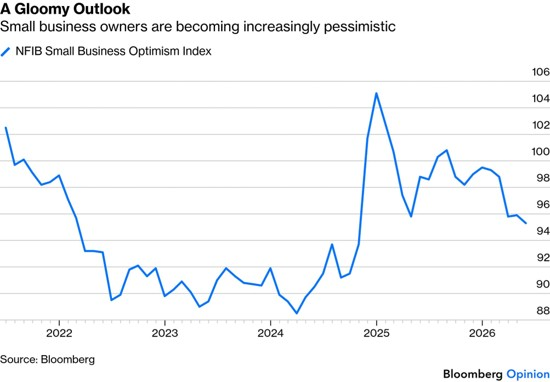

Small US Businesses: The NFIB optimism index gave back all its post-election gains. Over 70% of small business owners cite supply chain disruptions, hiring plans have collapsed, and capex is at its lowest since 2009. Unlike large corporations, most cannot pass rising costs on to customers.

AI Wobbles: The Nasdaq is down 7% from its peak but still up 12% for the year. Oracle fell 25% after flagging higher data centre capex, crystallising investor anxiety about AI return on investment. Excluding US tech, virtually all global equity markets are down since the war began — the AI boom is masking the conflict’s true drag.

Why Aren’t Oil Prices Higher?: China slashing imports by 40% (equivalent to removing Germany and France’s combined demand) is the single biggest reason. Add pre-war oversupply, the IEA’s record 400-million-barrel reserve release, bypass pipelines, Americas production at record highs, and Trump’s repeated peace announcements suppressing speculative buying. The critical unknown: how long can China sustain this without visible economic damage?

The End is Near, and Other Theories: A recommended podcast: Andrew Ross Sorkin on Trumponomics draws “eerie parallels” between today’s markets and 1929 — transformative technology, retail investor euphoria, and guardrails being dismantled.

AI and Jobs – China Showing the Way?: China’s state-run Workers’ Daily is calling for AI labour protections, courts are ruling companies must retrain before firing, and Beijing is warning tech firms not to cut jobs. Up to 70 million Chinese workers face displacement.

The Decline of Original Thought: UC Berkeley’s computer science course failure rates have tripled in two years, directly linked to AI tool dependency. The deeper risk: companies replacing junior staff with AI create a skills vacuum that senior “superusers” currently mask — but won’t forever. Universities must find a way to embed AI without sacrificing deep learning.

US Inflation – increasingly worrying

US consumer price inflation topped 4% last month for the first time in three years, but the market reaction was minimal. That’s partly because energy inflation is such a large part of the problem, and the most recent news flow from Iran tends to be more important for prospects on that front than backwards-looking data.

Obviously, with the on-again-off-again rinse and repeat Iran war news, which seems to depend on what side of the bed Mister Trump gets out of, it’s safe to say the price of oil isn’t going to ‘normalise’ any time soon. Perhaps we are just learning to live with it? In the US, this goes to the political core of the ‘affordability’ issue, which is likely to be a hot button in the midterms, with the midterms just 4 months away. As of Friday, the war is off again, having been on again in full force on Thursday (including the bombing of a desalination plant, in of itself considered a war crime). By the time you read this, who knows?

Also, core inflation, as usually defined — excluding food and energy — rose but came in below expectations.

Most importantly, for the traders, the numbers were immediately adjudged not to be bad enough to put an outright raise in the fed funds rate on the table for Kevin Warsh’s first meeting as chairman of the Federal Open Market Committee next week.

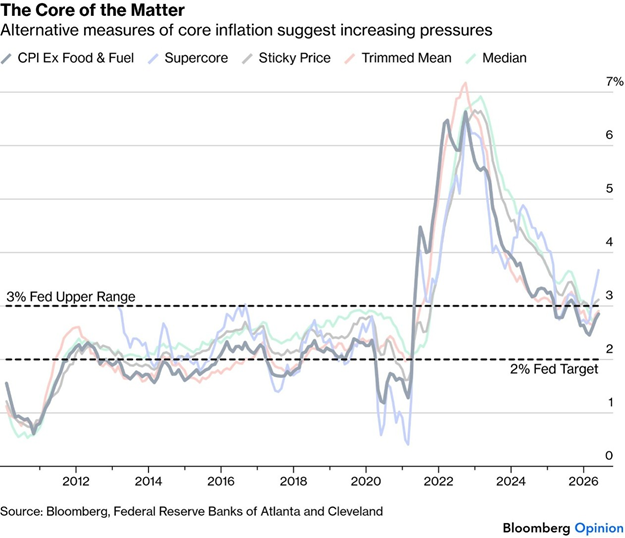

The market might be taking these numbers a tad too calmly. To start, this is the breakdown of inflation into its four main components:

The rise in the energy component is obviously important, but services remain obdurately high, while food inflation — politically salient these days — hasn’t gone away. These numbers rule out a rate cut.

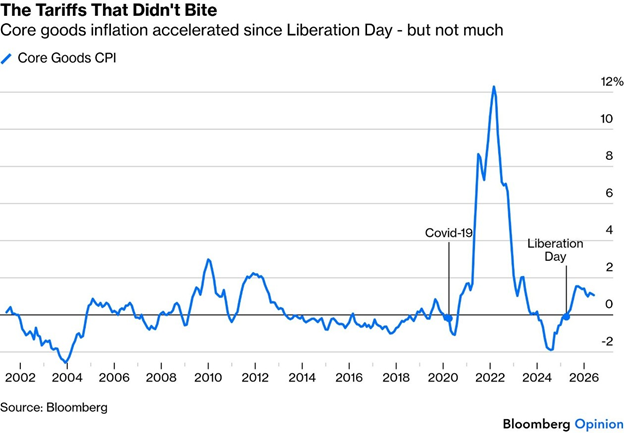

More to the point, alternative measures of core inflation signal that pressure is rising. The Fed’s favoured “supercore” of services excluding housing is rising sharply (the pale blue line pointing north below), while the gauge of sticky price inflation, covering products whose prices take time to change and are difficult to cut, has risen above 3%. (For the analysts among you, both the trimmed mean, excluding outliers in either direction such as oil and averaging the rest, and the median also rose and are higher than CPI excluding food and fuel.) There’s firm upward pressure on prices:

Look deeper and some interesting trends emerge.

This is about the point when last year’s tariffs should begin to drop out of year-on-year comparisons, and that does indeed seem to be happening.

Core goods are most directly affected by Trump levies, and have seen outright deflation for most of this century thanks to globalisation. Standing at zero ahead of the Liberation Day levies, core goods inflation never reached 2% and is now declining. The rise, in my opinion, is not quite the ‘nothing burger’ that Bloomberg are touting below:

If inflation threatens the US economy, it does so through the small businesses that make up its backbone. This strain is reflected in deteriorating sentiment, despite the enthusiasm that many small business executives have for the Trump administration’s agenda.

Following Trump’s election, optimism among small business owners soared to its highest level in more than three years, driven by expectations that Trump would push through pro-growth regulatory and tax policies. The National Federation of Independent Business’s chief economist described it as “a major shift in economic policy,” with owners “eager to expand their operations.”

May’s National Federation of Independent Business’ small business optimism index slipped below expectations, and gave up all its gains since Trump was elected:

We all know how chummy DJT is with the billionaire business owners, but small businesses make up 43.5% of US GDP. There are 36.2 million small businesses in the US, representing 99.9% of all businesses, employing 62.3 million people (45.9% of all private-sector workers), and paying 38.7% of total private-sector payroll. That’s a large chunk of your database to ‘annoy’.

The Middle East crisis is the most important driver of this pessimism. While input costs rise, not all businesses can pass them on to customers, leaving them to navigate the trade-off between survival and profitability (and staff layoffs). Unlike large corporates, which have more flexibility to absorb price rises, more than a third of small businesses have hiked selling prices, while another third plan to raise them. With more than 70% of small-business owners reporting that supply-chain disruptions are weighing on their operations, geopolitical uncertainty is also affecting them. It’s most evident in hiring plans, which, unsurprisingly, took a hit, while capex is at its lowest level since 2009.

The selloff for the biggest names in AI continues, but it’s hard to call it a correction. The Nasdaq 100 is down 7% from its peak last week, but still up 12% for the year, and above its 50-day moving average. And it’s doing this even though the war in Iran, which drove a sharp selloff three months ago, is heating up again, only to be countered by Trump’s 37th announcement that the war is ‘over’.

Oracle Corp., the software group trying to reinvent itself as an AI hyperscaler, has been on an even more exciting ride. Its announcement that it had devoted yet more capex to building out data centres than thought drove a 10% selloff after the market closed on Wednesday. It’s down 25% since its peak last week. But the headlong rally before then left much room for adjustment…

Graph: Oracle

Providers of AI infrastructure are obviously in good shape, with capex continuing (although semiconductor stocks have sold off 12% from their own peaks). But the market is beginning to wonder where the money will come from to pay for them. The divisions between winners and losers could grow more extreme if expenditure grows as some on Wall Street now expect.

The problem is that 2027 hyperscaler capex estimates may be too conservative. Analyst estimates imply hyperscaler capex will equal $920 billion in 2027, representing a sharp deceleration in growth from 84% in 2026 to 22% in 2027.

If incremental investment reaches 2-3% of GDP, similar to the build-out of railroads and autos, hyperscaler capex would reach roughly $1.1 trillion in 2027 (45% growth).

If this is right, we can expect more lurches like Oracle’s latest selloff.

The imminent arrival of new companies that offer a play on AI (like SpaceX last Friday) also churns the waters, as would-be buyers have to make room in their portfolios.

The tech boom obscures the Iran war’s market impact. The latest news is, on the face of it, bad, with hostilities appearing to be their worst since the ceasefire started two months ago. But the events in Hormuz — where traffic remains minimal — have progressively less effect on the stock market, or even on oil.

The oil and AI shocks both have diffuse economic effects far beyond the sectors directly involved in them, which makes it impossible to gauge which is the more powerful. But a crude way to account for the AI boom suggests it’s masking the impact of the war.

The following chart covers major world equity markets as measured by MSCI, excluding the chip-rich South Korea and Taiwan, and for the US, excluding tech from the S&P 500. All are down since Feb. 27, the last day of trading before war broke out:

This isn’t close to the nightmare market scenarios that seemed plausible in early March, but it also suggests that the war is creating more of a drag than many assume. Escalation in the Middle East, or a tumble in AI capex, would put this to the test, one that all will want to avoid.

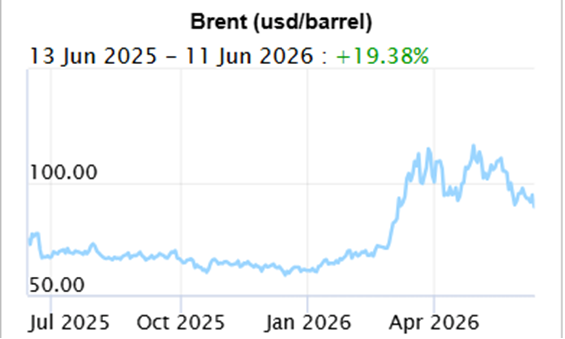

Brent crude prices have remained below the 2008 and 2022 peaks despite a much larger disruption to global supply – and that’s before adjusting for inflation. Why? Because the price of oil is one of the major driving forces behind the rise of inflation globally, it is important to at least try to understand this…

China, China and China

The global oil market is incredibly complex, with myriad factors interacting to keep prices under $100 a barrel. But if we had to pick just one, it would be China. Beijing has managed to slash its oil imports, providing a massive — and unexpected, relief valve. Last month, China imported 6.7 million barrels a day of crude via tanker, down nearly 40% from the 2025 average. That drop of 4 million barrels a day is roughly equivalent to the consumption of Germany and France combined.

How has China managed to dramatically reduce imports without suffering economic damage? We don’t know for sure. The country’s oil demand seems surprisingly weak, and it may also have tapped its strategic petroleum reserves surreptitiously.

This Chinese oil import collapse is the most important story in global finance and geopolitics but hardly anyone is talking about it. If Beijing was buying as much oil as it did in the past, prices would be much higher, global inflation would be rampant and central banks would be forced to hike interest rates quickly, panicking stock markets. Donald Trump would also be in a far weaker position in his talks with the Iranians. In short, it appears that China has essentially bailed out both the global economy and the political fortunes of the US president.

The amount of oil refineries are processing into fuel and petrochemicals has fallen by about 5 million barrels a day. Either consumers are cutting back significantly, or refineries are running down their inventories. Likely, both factors are at play, with demand destruction, mostly in the petrochemical sector, probably accounting for 3 million to 4 million barrels a day.

That’s a lot considering that prices have not increased as much as many expected. Perhaps the world has become structurally more responsive to higher oil prices. Over the last 20 years, the centre of the petroleum market has shifted to Asia, where consumers may be reacting more quickly than those in the US and Western Europe did during previous shocks.

Love them or hate them, the availability of electric vehicles may have moved the needle in China. Or, it could be that fuel simply hasn’t been available.

In India, for instance, cooking fuels like butane and propane have vanished from large swathes of the country. And surprisingly, Asian nations have quickly switched to other options, notably coal and firewood, in a way I very much doubt Western consumers would do.

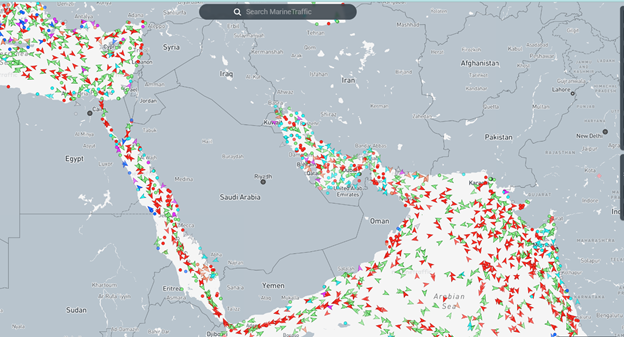

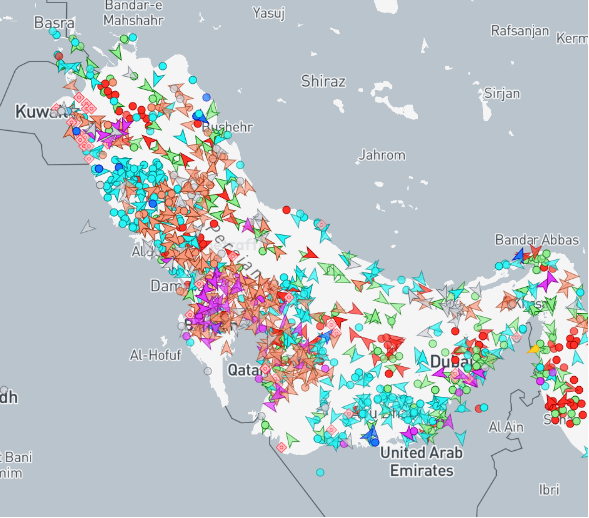

The Strait of Hormuz has been closed for more than 100 days. Yet oil still flows from the Persian Gulf. The first route is obvious: bypass pipelines that circumvent the waterway, crossing Saudi Arabia and the United Arab Emirates. The pipelines, which were previously little known outside the energy industry, have kept about 5 million barrels a day flowing.

More recently, oil has started to leave by tanker, with Emirati and Kuwaiti vessels shuttling from terminals inside the Persian Gulf, through Hormuz, to anchorage areas just outside the bottleneck, and then offloading their cargo to other ships. The tankers cross the strait hugging the Omani coast, and with their beacons off. What started as a trickle has now become a constant flow, to the tune of about 2 million barrels a day. If you’re interested here is a good infograph on the before and after traffic through the strait: https://www.nytimes.com/interactive/2026/04/16/world/middleeast/iran-us-strait-of-hormuz-blockade-map-ships.html

Or here to see it live:

https://www.marinetraffic.com/en/ais/home/centerx:51.1/centery:25.7/zoom:6

If you zoom in a bit, you can see that the Persian Gulf is still effectively a parking lot/marina.

The war has overshadowed a crucial fact: The oil market was oversupplied on Feb. 27, before the conflict started. By how much? Probably 3 million to 4 million barrels a day during the seasonally low-demand period between the end of the winter and the beginning of spring. That oversupply, built on the impact of the US shale revolution and OPEC+ output hikes during the preceding year, has provided an invaluable cushion.

When Iraq invaded Kuwait in 1990, rich nations didn’t tap their strategic petroleum reserves until six months later. This time, the US pushed its allies in the International Energy Agency to tap reserves during the first two weeks of the war. On March 11, the 32 members of the Paris-based IEA announced they would release 400 million barrels over the following months — the largest release in the organisation’s history. Still, it took time for those barrels to hit the market, only gathering speed in late April. Now, the oil is flowing at a rate of about 2.5 million barrels a day. But with the US reserve, a major contributor, already at its lowest level in 40 years, it won’t go on forever. At the same time, the oil industry is burning through millions of barrels of commercial stockpiles that could approach critical levels by August. This pressure might be upping the urgency on Trump to exit this war…

Today’s refineries are far more flexible, both in what they produce, gasoline, diesel, jet fuel, fuel oil, petrochemicals, and in what they process, than those of even a few years ago. The previous facilities were picky, only processing a handful of crude varieties. Now, thanks to investment in new units called cokers, they can process a much wider range. The new refineries can also shift, to a point, the percentage of each refined product they output. That translates into an ability to generate more of what’s needed. Take jet fuel. Before the war, it accounted for 10.5% of the US refinery output. That yield has now climbed to a record high of nearly 13%.

When it comes to oil, the White House seems to have gone into the war with lots of bluster and not much strategy or evidence of thought of the consequences. Still, Trump has excelled in one area: “jawboning” the market. Via social media and interviews, he kept oil traders on their toes, warning nearly 40 times over 100 days that a deal was just around the corner. For any oil trader betting on price hikes, the president’s pronouncements created an enormous risk of being stopped out, with prices often falling as much as 10% after some posts.

The jawboning wouldn’t have worked, however, without a receptive audience. Wall Street not only believes Trump, but it also wants to trust him. If former President Joe Biden had made similar comments, the oil market would have laughed him out of the trading room.

For decades, buying oil futures was the only way to hedge against Middle East conflict. As everyone went long, the buying spree invariably created a self-fulfilling price spiral. The options market, which allows traders to buy insurance without betting prices will rise, simply wasn’t liquid enough. Over the last decade, however, that market has grown exponentially. Back in 2016, the average daily volume of call options — which provide upside price protection — for Brent crude was around 25,000 lots; it now averages 200,000 lots, with recent peaks of 550,000 lots a day.

Trading volumes in “call options”, which allow traders to buy insurance against higher oil costs without betting prices will rise, have exploded over recent years.

Veteran oil traders recall the market-intelligence innovation of the 1990-1991 Gulf War was jerry-rigging a satellite dish to watch grainy night-vision footage on CNN. It was difficult to distinguish between real and rumour. Today, the fog of war is thinner thanks to the availability, at a reasonable price, of commercial satellite photographs that allow traders to observe what’s happening in near real-time. Satellites have also improved the tracking of tankers. Simply put, the current oil market is trading more on information, despite imperfections, and less on speculation.

The oil market is, rightly,so obsessed with the output losses in the Persian Gulf that few are paying enough attention to the production gains elsewhere. But they are real, and very large.

The American continent is enjoying a production boom, with output up about 2 million barrels between the second quarter of 2025 and the same period of 2026. Brazilian output is up a staggering 20% year-on-year, to a record. Guyanese and US production also hit all-time highs in April, according to preliminary data. Canadian output is also strong, and Venezuela’s is recovering. To be sure, the gains are only a fraction of the losses in the Middle East, but in a tight market every barrel helps. Chinese oil production, too, is at a record high.

For 100 days and counting, those factors have kept oil prices under control. The biggest and most crucial uncertainty is China. How long can Beijing continue whatever it is it’s been doing? Oil’s next 100 days may depend on the answer to that unknown.

The end is near, and other theories – a podcast to listen to.

Almost a century after the Wall Street crash of 1929, Andrew Ross Sorkin says he believes some of its most dangerous ingredients are reappearing. Joining Stephanie Flanders on Trumponomics, the financial journalist and author of 1929: Inside the Greatest Crash in Wall Street History argues that today’s market is filled with “eerie parallels” to the late 1920s. You can listen to it here

These include a transformative new technology, a flood of retail investors and a growing willingness to loosen the rules. “We are dismantling the guardrails,” Sorkin says, pointing to everything from cryptocurrency to private-market investments being repackaged for ordinary investors.

AI and jobs- China showing the way?

China’s rapid adoption of artificial intelligence in the workplace has prompted an unusually blunt call from a state-run newspaper to protect labour rights, as Beijing considers how to contain risks posed by the new technology.

An editorial published in the Workers’ Daily, the official mouthpiece of China’s umbrella trade union organisation, they urged government agencies to mount an active response as new threats emerge to the rights of employees. It called on regulators to improve labour standards and strengthen oversight of AI algorithms, including by giving a greater say to trade unions and workers’ representatives.

“The benefits of technological advancement should be shared by society as a whole, rather than becoming a tool for a small number of employers to undermine workers’ rights,” the editorial said. It was titled “With the AI wave surging, how can we build a strong ‘dam’ for workers’ rights?”

The deployment of AI tools around the world presents a special challenge for China, where employment is a politically sensitive issue and maintaining social stability is a priority for top leaders.

As AI spreads across workplaces, China is also having to contend with chronic weakness in the jobs market — a major obstacle for Beijing’s efforts to revive confidence among households. Widespread but still shallow adoption of AI eventually threatens to displace as many as 70 million workers in the country.

The looming disruption has prompted the Workers’ Daily to publish a series of reports devoted to labour protections during what it called the “AI wave.” The newspaper was founded in 1949, the same year the Communists established the People’s Republic of China, to act as a “voice for China’s working class,” and it remains among the leading state media outlets in the country.

In addition to the job losses blamed on AI, the newspaper identified other problems facing employees, such as violations of personal rights through “distilling” white-collar skills. For blue-collar labour such as couriers and drivers working for ride-hailing companies, it said the algorithms used by platforms also failed to provide adequate transparency on how they allocate orders and set unit prices, worsening inequality in the distribution of income.

The newspaper said that AI adoption that aims solely at reducing the use of human labour should be approached with caution. Such decisions “should not be left entirely to market forces, and government authorities need to play a key role”. The Chinese government has reportedly begun warning employers, particularly tech companies, not to cut jobs as they adopt AI. Court rulings in Beijing and Hangzhou have favoured workers in such disputes and held that companies are legally required to retrain or reassign workers before terminating their employment.

Author: Dawn Ridler

The decline of original thought.

According to University of California Berkeley, 35.3% of students only managed F’s for CS10 exams and 10.6% managed the same grade for CS61A exams. These are US acronyms for “Introduction to Computer Science” and “Structure and Interpretation of Computer Programs”. For the same spring exams over the prior 2 years only 10% of students got the dreaded F. There seems to be an increase in students using LLM’s (large language models) to do their homework and problem solve. The problem with this is that during exam time, when they have only their own ability to count on, things start to fall apart.

It was also noted that some students who thought they were proficient when entering University actually weren’t. That is because AI was used in many instances, which took away the ability to learn content deeply. Also from the same university, the spring EECS127 class, “Optimization Models in Engineering,” saw a 16.8% F rate, far higher than the 5% of D’s and F’s that the Engineering department describes as “typical” for an upper division course. The data points to the same thing. All of this leaves a bit of a conundrum.

In the past, if you were proficient in a specific area, it was because you had spent time studying it, failing at making certain observations, and once practical experience had been secured, you became proficient. This is the long yards, the ability to throw yourself at a problem to make a way that others did not see. To be eligible, this required academic proficiency and a profound need to learn.

Add all of these together, and one has a Bill Gates or an Alexander Fleming possibly in the making. AI, in essence, short-circuits this process for students. If it’s not used responsibly, students fail to learn deeply, and this means that their ability to innovate in a specific field will also be hampered. They, in essence, cannot solve tomorrow’s problems because they don’t understand today’s challenges, which can only come through doing the hard yards.

But the problem goes even deeper than this.

Companies are starting to incentivise managers to use AI in their business activities. This means that AI is taking over where junior engineers and analysts once worked. The margins are going to look great on the income statement, but long-term this is going to cause a skills vacuum. You probably won’t see it in the short term, as senior staff act as superusers, blending processes and AI to solve problems. But what happens when these super users are poached by competitors or retire? Then the next human in line, who has hopefully been developing their skills, isn’t there. The next human in line is a student who has failed to grasp all of the basics and, therefore, can only innovate to the point AI will allow.

If one combines the University experience with the world of work, AI is applying pressure from both ends, which could leave us in a worse situation than before. We are losing the ability for original thought. Companies and organisations are about efficiency, and here I understand the use of AI to drive better margins. Any good manager would be embracing this. But universities sit with a real conundrum.

How do they turn out quality graduates whilst also embracing AI. In the early days of AI (only 2 years ago!), some institutions thought they could ban users from using AI. This response doesn’t take the future into consideration and is fruitless long-term. I think we are now at a point where universities need to think carefully about how they use AI as part of the learning experience. The ultimate aim is to create more holistic learning so that the student can deeply learn. Get this right, and one creates a new generation of leaders.

Author: Cobie Le Grange

EXCHANGE RATES and other Indices:

The Rand/Dollar closed at R16.27 (R16.55, R16.23, R16.46, R16.68, R16.39, R16.63, R16.29, R16.41, R17.07, R17.06, R16.89, R16.55, R15.93, R16.01, R15.96, R16,03, R16.15, R16.10, R16.50, …R16.91, R17.13, R17.36, R17.13,16.52 )

The Rand/Pound closed at R21.80 (R22.06, R21.80, R22.09, R22.21, R22.30, R22.56, R22.35, R22.02, R22.09, R22.77, R22.76, R22.35, R22.20, R21.48, R21.59, R21.78, R21,82, R22.11, R21.97, R22.13, …R22.57, R22.68, R22.74, R22.56,

The Rand/Euro closed the week at R19.16 (R19.08, R18.91, R19.11, R19.38, R19.29, R19.48, R19.37, R19.17, R19.24, R19.70, R19.77, R19.33, R19.23, R18.80, R18.87, R18.94, R18.93, R19.14, R19.04, R19.20)

Brent Crude: Closed the week $87.33 ($93.09, $91.12, $104,24, $109.26, $101.29, $108.83, $105.33, $90.38, $95.20, $107.88, $112.36, $103.14, $92.88, $73.19, $71.76, $67.75, $68,05, $69.32, $65.88, $63.34, …$63.71, $63.19, )

Bitcoin closed at $64,131 ($60,762, $73,788, $74,559, $77,879, $80,733, $78,204, $78,049.98, $75,519, $70,904, $68,691 , $68,586, $70,869, $67,310, $63,534, $68,04, $69,649, $68,553, $81,301, $89,295, $90,585,)

Articles and Blogs:

Legacy Series Part 4 NEW

Legacy Series part 3

Legacy Series Part 2

Legacy Series Part 1

Holiday checklist

Next year – Action Plan

Next year – Vision, Mission etc

Medical Risk Mitigation

Next Year – Consolidation

Abdication or diversification?

Carbo-loading your retirement Spoiled for choice

Who needs a plan anyway

8 questions you need to ask about retirement

What to do when interest rates drop

How to survive volatility in your investments

What to do when interest rates drop

Difficult Financial Conversations

Financial Implications of Longevity

Kick Start Your Own Retirement Plan

You matter more than your kids in retirement

To catch a falling knife

Income at retirement

2025 Budget

Apportioning blame for your financial state

Tempering fear and greed

New Year’s resolutions over? Try a Wealth Bingo Card instead.

Wills and Estate Planning (comprehensive 3 in one post)

Pre-retirement – The make-or-break moments

Some unconventional thoughts on wealth and risk management

Wealth creation is a balancing act over time

Wealth traps waiting for unsuspecting entrepreneurs

Two Pot pension system demystified

Cobie Legrange and Dawn Ridler,

Rexsolom Invest, Licensed FSP 45521.

Email: cobie@rexsolom.co.za, dawn@rexsolom.co.za

Website: rexsolom.co.za, wealthecology.co.za