| The podcast of the newsletter is available and you can download it HERE. We welcome all your input so please don’t hesitate to contact us if you’ve got any queries or suggestions. Market Watch The markets last week gave the new political dispensation a resounding round of applause. The JSE is now up 6.6% year on year – but 4,5% of that was last week. This underlines our investment philosophy – you need to align and allocate your wealth and assets for the long term then be patient. There are so many moving parts to markets and economies that nobody can predict one day to the next, you must have faith in the long-term trends, over decades, that show you where above inflation returns are going to come from. South African businesses have been hamstrung by previous political dispensations and outright corruption and theft – costing the country billions of rand. There is going to be a lot of horse-trading and volatility in the coming months and years – and it is also possible that this governing unity could fall apart – but the country basically has 2 years (before the local elections) to prove that things can work in a different way.   China still on the back foot China left benchmark lending rates unchanged at a monthly fixing on Thursday, in line with market expectations. Why is that important? The steady monthly LPR fixings underscore that Beijing’s monetary easing efforts continued to be limited by narrowing interest rate margins and a weakening currency, despite a flurry of recent data showing more support is needed to shore up an uneven economic recovery. The one-year loan prime rate (LPR) was kept at 3.45%, while the five-year LPR was unchanged at 3.95%. China’s new home prices fell at the fastest pace in more than 9-1/2 years in May, official data showed on Monday, with the property sector in a depressed state despite government efforts to rein in oversupply and support debt-laden developers. New bank lending in China rebounded far less than expected in May and some key money gauges hit record lows, suggesting the world’s second-largest economy is still struggling to pick up the recovery pace. Most new and outstanding loans in China are based on the one-year LPR, while the five-year rate influences the pricing of mortgages. The five-year LPR was lowered by a 25-basis-point in February to support the housing market. This seems to have had little effect. Financial News, a central bank-backed newspaper, said in a commentary this week that China still has room to lower interest rates, but its ability to adjust monetary policy faces internal and external constraints. New home prices – the most important indicator of middle-class wealth in the world’s second biggest economy – dropped at the fastest pace since October 2014, falling 0.7% m-o-m in May (v/s -0.58% in April) and marking the 11th straight decline despite the government’s stimulus to support the property market. On an annual basis, home prices slumped 4.3%, the biggest drop since the summer of 2015. Interestingly, the last time home prices plunged so much Beijing pursued a massive yuan devaluation that led to a $1 trillion in FX outflows to stabilise and sparked the very first mega meltup in bitcoin which sent it from $200 to far over $1000.  This failure to recover from zero-COVID is coming from the consumers – not a good sign for the CCP who are wanting to increase their control over their populace. What is the equivalent Chinese saying to “Happy Wife, Happy Life?”  Rate cuts The Europeans are breaking tradition by front-running the US FED rate cuts, with Switzerland the latest to do so. This 25 bp cut is on the back of another 25 bps in March bringing the interest rate down to 1.25% This is not really surprising as the root cause of inflation in the States was not really a global problem, but had rather been caused by the overly-generous stimulations cheques paid out to Americans – not necessarily based on need or financial hardship (the Socialist approach) but democratically in order to stimulate the flagging economy (the Capitalist approach). The Bank of England has kept the rates steady, despite the CPI print coming in at 2%, in other words on target. This is probably due to the proximity to the elections and the rate cuts could well start next month – following the pattern in Europe and elsewhere of not following the FED this time round.  Our (RSA) next interest rate decision from the Reserve Bank is on 17th of July. This interest rate (repo) will apply to bank credit and savings rates, but if you look at long-term bonds, below, they have already started to come down, having already peaked at the prepandemic highs in April/May.   |

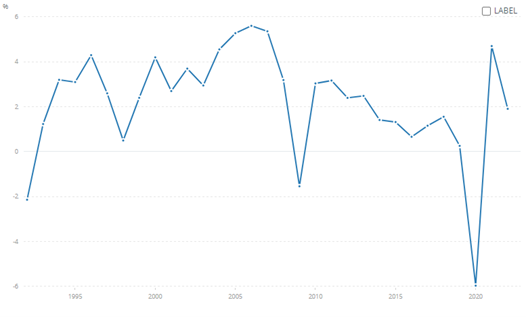

| Magnificent 7 While one day’s movement in a stock market share is usually insignificant in the grand scheme of things, the fact that Nvidia can drop $246b in one day is just eye-watering. That’s 4.4 Trillion Rand – that is almost exactly double the total tax receipts in RSA last year. This reversal in market cap is a new record – beating their own record set on March 5th. Although Nvidia shares had been up as much as 3.8% earlier in the session on Thursday and on pace to expand the company’s market-cap lead over Microsoft Corp. MSFT, -0.14%, they turned lower around midday and closed the day down 3.5%, which translates to a $3.22 trillion valuation, versus $3.31 trillion for Microsoft. In other words, the two behemoth counters are now constantly vying for the top spot. Have investors become aware that this is not a game or competition? The huge volatility, seen in these so-called magnificent 7 shares, is remarkably similar to the sort of volatility we last saw during the Dot Com crash. Nobody seems to know who is pushing these stocks higher, which may just be a clue that it is retail rather than professional investors. In other words, FOMO.  While they are still shining bright let’s just recap the Globe’s Trillion Dollar club • Nvidia: The industry leader in data centre chips, essential for training artificial intelligence • Microsoft: Dominance in enterprise software products (e.g. Windows, Office, Azure) • Apple: Strong track record of innovation and a large, loyal customer base • Alphabet: Leading player in online advertising and other digital platforms (e.g. Google Search, YouTube) • Amazon: Dominance in e-commerce and rising cloud computing market share through Amazon Web Services (AWS) • Saudi Aramco: World’s largest oil producer with massive reserves • Meta: Dominant player in social media (Facebook, Instagram, Whatsapp)  Diversify, Diversify Let’s face it… it’s been a terrible time for SA investors. The overarching principles of diversifying portfolios not only across various asset classes but also geographies had been replaced by the notion that you cannot have enough capital offshore. Many pundits have been telling investors that they should take all of their assets offshore and forego any exposure to South Africa. Last week I wrote about the overall quality on offer in South African equities relative to their offshore counterparts, and even though this may be true, we have never foregone owning the dwindling list of quality equities on offer locally. A few weeks ago, we even did an exercise to see what percentage of a portfolio we could still fill with SA equities once we had risk-adjusted their weightings. The good news is that we could still give a fair representation to SA incorporated. The naysayers were expecting a leftist government borne out of the ANC not being able to achieve a majority. During the GNU negotiations, plenty were calling it the end of South Africa as we know it. But as the country seems to do time and time again, it edges to the precipice and looks down the abyss of failure, and then miraculously self-corrects. In all the time I have lived in the country this has occurred most notably in 1994 at the dawn of democracy. On Wednesday last week, this was another of those times. It’s historical not only because it’s the first time after a long stretch of single-party rule that the country will be led by a grouping of parties but also because we averted disaster. The inaugural speech was all about pushing the country ahead by delivering in key areas with a stark warning to those who wanted to detract from the process through violence or other means. The All Share gained 8%p.a over the last decade up to the end of May. Poor SA-listed property, once a darling asset class, only achieved 3% p.a. But June is setting itself up for the record books as it has already posted a return of around 4% with the banks gaining more than 15% in a week and the likes of Clicks and Vodacom ending more than 10% higher for the week. It’s almost as if markets have sighed in relief that the leftist outcome has been averted. The ZAR decidedly ended below 18 to the Dollar having touched 19 to the Dollar early in May. If you happen to own a diversified set of assets your portfolio has been the beneficiary of your patience. Now the question is will this be a new dawn for SA Incorporated? Well, this may take some time. The right political moves have been made but the delivery now has to happen. Expect Parliament to engage robustly to test individual allegiances and for the naysayers to continue their efforts to scupper the good work done so far. But once there is actual delivery and more importantly the finance minister can stand up and show how our tax Rands are being spent wisely, we may very well be on our way. The fruits of change weren’t evident in 1994, but from 1996-2006 the country grew at a clip (there was a market crash in 1998 causing the near zero growth rate during that year). SA Annual GDP Growth  If we are hoping to be counted on the global stage, we are going to need a lot more of that. If you live in the country you may inadvertently be finding yourself at the proverbial right place at the right time. Only time will tell but at least the seeds of change have now been sowed. Author:- Cobie Legrange EXCHANGE RATES:  The Rand/Dollar closed up at R17.91 (R18.37, R18.90, R18.87, R18.42, R18.26, R18.43, R18.51, R19.09, R18.68, R18.99, R18.76, R18.72, R19.15, R19.30, R18.97, R19.03, R18.80, R18.78, R19.03).  The Rand/Pound is also better at R22.63 (R23.37, R24.18, R23.98, R23.46, R23.11, R23.80, R23.22, R23.62, R23.61, R23.93, R23.90, R24.06, R24.18, R24.47, R23.61, R24.03, R23.87, R23.86, R24.15.)  The Rand/Euro closed the week well up at R19.14 (R19.67, R20.59, R20.42, R19.97, R19.08, R19.86, R19.92, R20.35, R20.25, R20.56, R20.43, R20.47, R20.71, R20.93 R20.38, R20.51, R20.38, R20.40, R20.72.)  Brent Crude: Brent closed the week up at $85.22 ($82.30, $79.91, $81.73, $82.16, $83.43, $82.73, $82.82,$87.39, $90.87, $86.58, $85.33, $81.80, $83.80, $83.40,$83.14 $80.91, $77.36, $83.66, $78.33.) This price rise is due to the building back of inventories and increased tensions in the Red Sea which will interrupt deliveries.  Bitcoin was down slightly again at $65,635 ($ 66.975, $71,257, $68,362, $69,391, $66 328, $60,880, $63,154, $64,135, $68,804, $64,681, $69,078, $68,340, $62,315, $54,649, $52,510, $47,195, $ 42,897, $41,608, $41,680). Articles and Blogs: Taking a holistic view of your wealth NEW Why do I need a financial advisor ? Costs Fees and Commissions The NHI and what do do about it New-Normal for Retirement? Locking-In Interest rates – The inflation story Situs – The Myths and Reality Tax Residency – New Rules new headaches Are retirement annuities dead A new look at retirement Offshore investing – an unpopular opinion Cobie Legrange and Dawn Ridler, Rexsolom Invest, Licensed FSP 45521. Email: cobie@rexsolom.co.za, dawn@rexsolom.co.za Website: rexsolom.co.za, wealthecology.co.za |