I contributed to a piece for Citywire on Retail Impact Investing. You can read it HERE

Too Busy? Got Better Things to Do? Read the Summary…

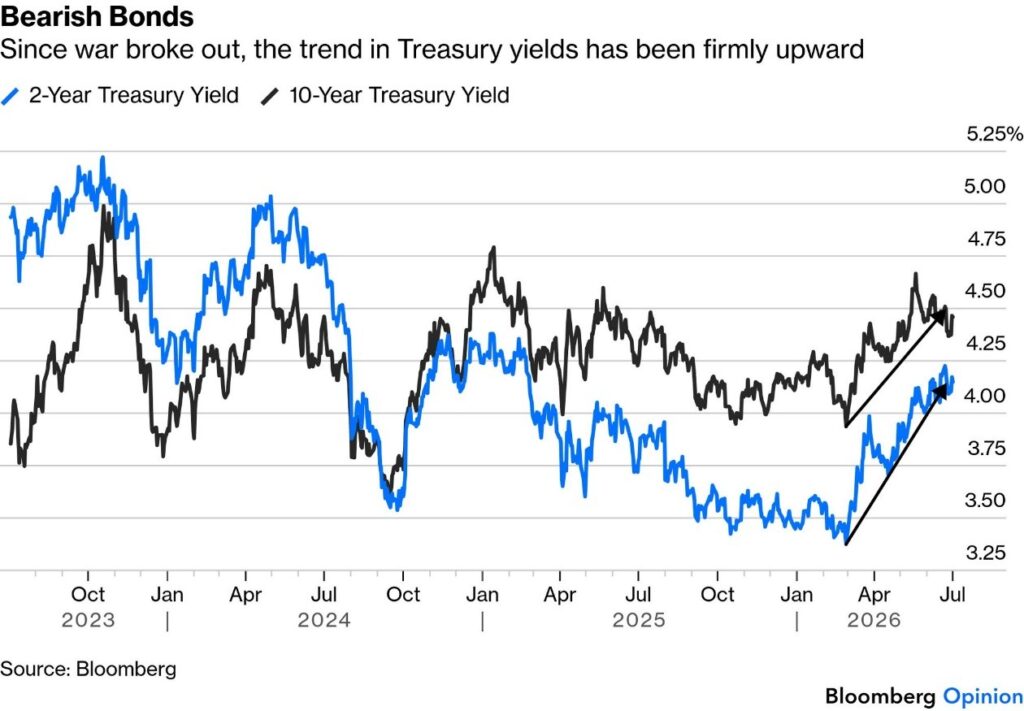

FED: Kevin’s First International Foray: Warsh told the Sintra conference that inflation expectations and risks have fallen, credited as much to lower oil prices as to his hawkish stance. The piece argues the resulting “bear flattening” of the yield curve isn’t benign: it signals tighter liquidity and “higher-for-longer” risk rather than a simple growth/inflation slowdown, with rising two-year yields outpacing 10-year yields and strong JOLTS data giving the Fed little cover to cut. It flags risks in how Treasury issuance and buybacks are managed, and concludes Warsh must let conditions tighten gradually rather than “fight the curve.”

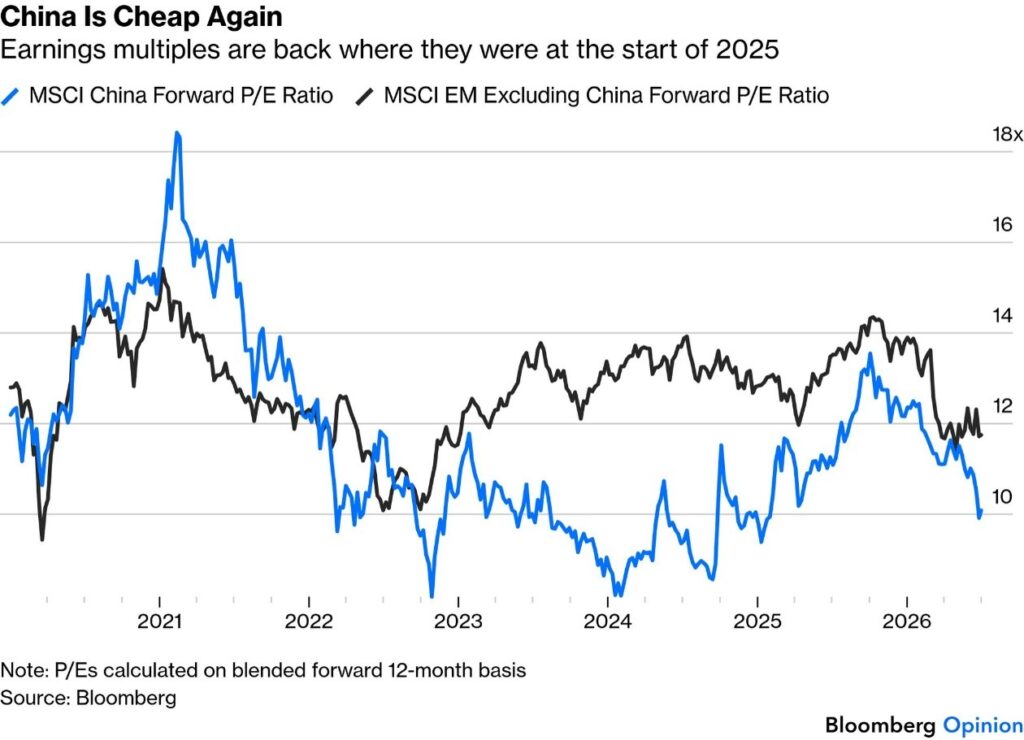

Slow boat for China: Chinese equities have sold off sharply, with the offshore Hang Seng China Enterprises Index in a technical bear market (>20% off its October peak), partly tied to Beijing’s crackdown on Hong Kong-based online brokers. Concerns centre on capital flight, weak tech/consumer earnings momentum, and continued reliance on exports rather than fiscal stimulus.

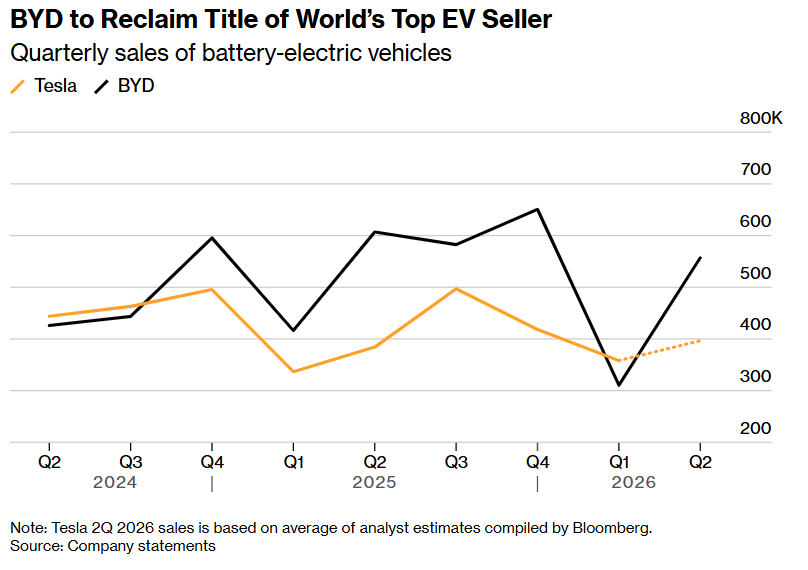

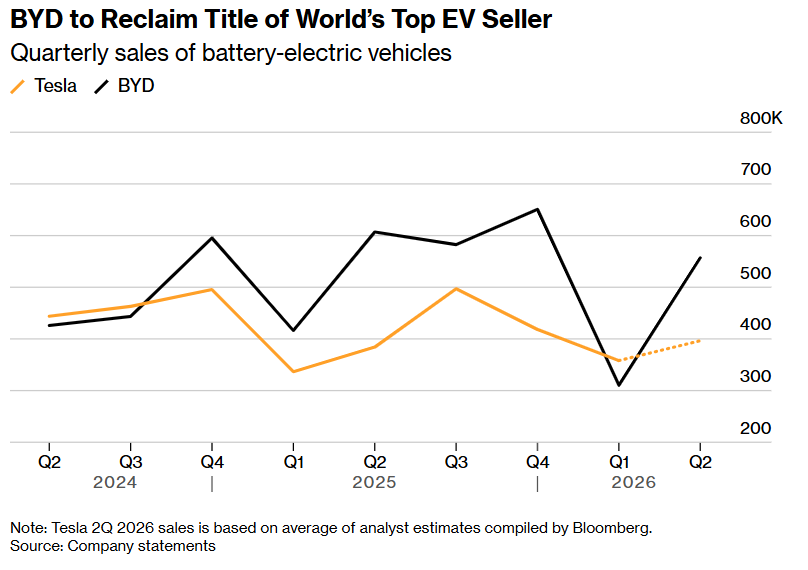

BYD Co: BYD looks set to reclaim the world’s top EV-seller title from Tesla, delivering 557,090 battery-electric vehicles in Q2 vs Tesla’s expected ~396,500; shares jumped as much as 8.4% on the news. Covers the BYD/Tesla lead swings since 2024, BYD’s blade-battery expansion, and a 7.5% y/y drop in China’s NEV sales in May.

When the tail wags the dog: A $13bn CSOP SK Hynix leveraged ETF in Hong Kong has grown large enough to amplify — not just track — swings in SK Hynix and the Kospi (where SK Hynix and Samsung together make up ~57% of the index). On volatile days the ETF and peers account for two-thirds of SK Hynix trading; a recent >20% ETF plunge dragged the stock down over 10% and hit MSCI’s emerging-market index.Consciousness: Distinguishes human consciousness (self-awareness, EQ, moral judgment) from AI’s current “left-brain” function. Argues AI’s lack of consciousness matters less as an assistant tool, but becomes critical if it moves toward autonomous superintelligence, where a collective “moral compass” built from manipulable inputs could sanction outcomes individual human morality would reject.

This Week’s Roundup

FED: Kevin’s First International Foray

Kevin Warsh certainly isn’t taking anything for granted, but he was justified in telling the central banking conference in Sintra, Portugal, that his chairmanship of the Federal Reserve is going according to plan so far – good luck rather than good planning to be fair.

“Expectations of inflation over the first four weeks of this period have come down,” he said, and “inflation risks have come down.”

This is accurate and owes at least as much to the fall in oil prices as to the market surprise that he is setting himself up as an inflation hawk. He also did a good job of sounding markedly different from his predecessors, and without in any way coming over as rude to his European hosts — a trick that American politicians who have visited recently have notably failed to manage.

But while he’s right that the bond market is taking him seriously and dialling down inflation expectations, that’s not necessarily great news. The yield curve — the amount by which yields on longer-dated Treasuries exceed shorter-dated bonds — is reducing, in what is known on markets as a “bear flattening.”

The US yield curve is flattening, but not in a benign way.

In liquidity terms, a flatter curve is consistent with tighter conditions. Less liquidity raises systemic risks and so increases the demand for longer-dated ‘safe’ government debt. The problem is that this implies a bearish flattening… It points to a market increasingly focused on ‘higher-for-longer’ policy risk rather than on a straightforward growth and inflation slowdown.

The rise in two-year yields since inflation fears were revived by the Iran war has been much sharper than in 10-year yields.

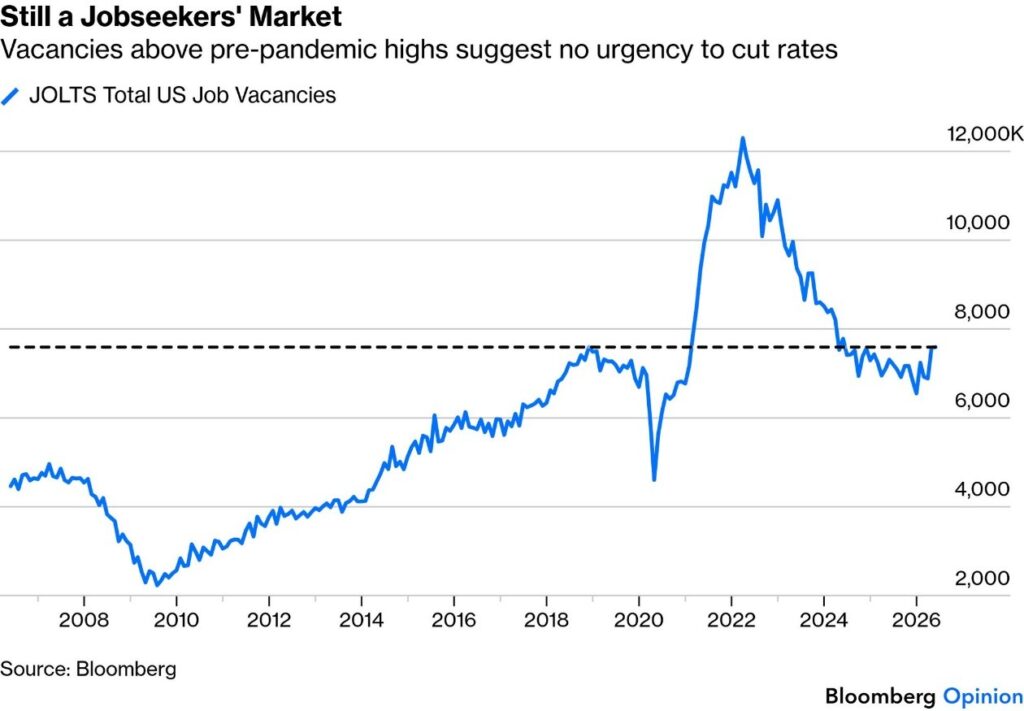

A further reason for rising bond yields is the strength of the incoming data, which continue to offer scant reason for rate cuts. The latest JOLTS (Job Openings and Labor Turnover Survey) numbers, for May, show vacancies now above their pre-pandemic high from 2019:

AI may well eventually have a profoundly negative effect on the demand for human labour, but for the time being, workers are in a strong position in wage negotiations (meaning inflationary risks), and the economy seems buoyant.

That’s good news and suggests that all the Fed needs to do, as Warsh said repeatedly at Sintra, Portugal, is keep a lid on inflation. Which, all else equal, means rates are more likely to be higher for longer. It could also lead to a stronger dollar than currently expected, particularly as Warsh’s counterparts from other central banks sound less likely to raise rates.

Warsh may well be right that the current odd combination of falling inflation expectations and rising rate forecasts shows confidence in the Fed. But it also suggests that rates will indeed be higher for longer. That would tighten financial conditions and create its own risks.

Barring a sudden easing of inflation pressure, suggests that the US might be tempted to concentrate Treasury issuance in short-dated bonds (a policy they’ve already been following). That would lean downward on longer yields, but it would also risk accelerating monetary growth, as bank purchases of debt are a form of monetisation.

Warsh has made plain his opposition to conducting monetary policy through bond purchases, rather than through setting interest rates.

Alternatively, the Treasury could step up its program of buying back bonds, which has had the effect of reducing bond market volatility (and thus easing financial conditions by making it easier to use bonds for collateral).

But such policies are extremely vulnerable to shocks. Warsh has done a good job of establishing his credentials so far, but he now needs to show that he’s prepared to let conditions tighten gradually (whatever the president who nominated him thinks of this) to avoid the risk of a major bond dislocation later.

The key question is whether Warsh is going to fight the trends of the new macro regime or flow with them. If Warsh chooses to fight, delaying necessary rate adjustments will likely force the Fed to hike a lot more down the line. This would have major implications, and it could break the back of the AI equity bull next year with potential negative spillovers on the economy, and it would adversely impact the extent of the dollar rally.

Suppressing the curve today might merely store up a larger bond-market shock tomorrow: Frankly, policymakers should allow the US liquidity cycle to contract naturally. Note to the Fed: don’t fight the curve.

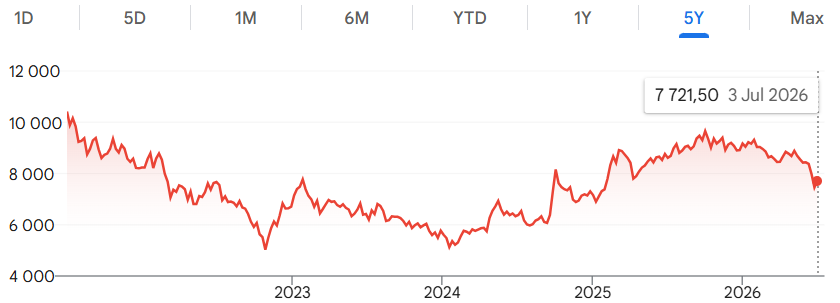

Chinese equities have conspicuously lacked resilience in recent weeks as the Iran war exposed the fragility of a rally that once looked difficult to derail. The advance sparked by the Communist Party’s “whatever it takes” moment nearly two years ago is now giving way to a renewed selloff, just as consumer sentiment sinks to record lows and demand remains stubbornly weak. The slump has the trappings of the broader selloff in global tech stocks but goes beyond that.

The offshore Hang Seng China Enterprises Index (or “red chips”) fell into a technical bear market last week after tumbling more than 20% from its October peak. This might be linked to Beijing’s late-May crackdown on several Hong Kong-based online brokers, which reinforced concerns that policymakers are increasingly determined to keep Chinese savings at home.

That the move possibly reflected growing fears of capital flight as domestic interest rates continue to grind lower — an issue that for many years has bedevilled Japan, which these days has higher yields. The risk of this happening is exacerbated by the upward turn in yields elsewhere.

Graph: Hang Seng China Enterprises Index

But China’s stock market downturn also reflects concerns about the pace of Beijing’s economic recovery and whether it has enough momentum to translate into earnings growth, particularly for technology and consumer-oriented sectors. With tech stocks leading the losses, investors are rotating into defensive sectors:

With Chinese equities down by about 15% for the year, it’s plausible that losses on existing holdings have more than offset the value of new purchases. Attractive valuations, better export data, and the potential for further policy support if stocks sell off much more explained why foreign investors were still adding to Chinese holdings as share prices fell.

One reason Beijing might maintain a tight fist and avoid widespread fiscal stimulus is the continued outperformance of exports, which have propped up growth in the wake of the housing sector’s spectacular collapse.

If exports lose momentum, policymakers would rely more actively on fiscal and quasi-fiscal tools. For now, strong exports have given them room to respond later.

Meanwhile, the wait for the elusive fiscal stimulus continues. China’s reluctance to unleash widespread support for domestic consumption, even as it relies heavily on exports, leaves investors betting more on attractive valuations than on an imminent economic turnaround. If there’s any lesson from the rally that followed the 2024 whatever-it-takes pivot, it’s that until policymakers deliver a stronger demand-side response, the equity market will likely continue appealing to bargain hunters without sustaining a durable rally.

BYD is poised to reclaim the title of the world’s top seller of fully electric cars from Tesla Inc. as the Chinese automaker ships an increasing number of vehicles abroad.

The maker of the Dolphin delivered 557,090 battery-electric models in the three months through June, according to figures released last Wednesday. While that’s fewer than in the same period last year, it’ll probably be enough to beat Tesla. The US manufacturer is expected to report quarterly sales of around 396,500 vehicles next week, according to analyst estimates compiled by Bloomberg

BYD shares climbed as much as 8.4% in early Hong Kong trading on Thursday last week, the biggest intraday gain since February 2025.

BYD first overtook Tesla in the fourth quarter of 2024, and maintained a significant lead through 2025 as Elon Musk’s political activities and close ties with US President Donald Trump disenchanted consumers, particularly in Europe.

However, Tesla retook the lead in the first quarter of this year, outselling BYD by around 48,000 vehicles as softening demand in China dragged down the rival’s sales in its home market.

With China’s auto market entrenched in a fierce price war, BYD is focusing on technology upgrades to compete with rivals like Geely Automobile Holdings Ltd. and Xiaomi Corp.

It is also rapidly expanding the production of its next-generation blade batteries.

A blade battery is a long, flat form factor of lithium iron phosphate (LFP) electric vehicle (EV) battery developed by the automaker BYD. Named for their resemblance to a row of razor blades, they use a “cell-to-pack” architecture that increases structural rigidity and is widely used across the EV industry today Global EV sales are on track for another record year, though growth in major markets is slowing. In China, the world’s largest market, sales of new energy vehicles — including EVs and plug-in hybrids — fell 7.5% in May from a year earlier.

BYD is poised to reclaim the title of the world’s top seller of fully electric cars from Tesla Inc. as the Chinese automaker ships an increasing number of vehicles abroad.

The maker of the Dolphin delivered 557,090 battery-electric models in the three months through June, according to figures released last Wednesday. While that’s fewer than in the same period last year, it’ll probably be enough to beat Tesla. The US manufacturer is expected to report quarterly sales of around 396,500 vehicles next week, according to analyst estimates compiled by Bloomberg

BYD shares climbed as much as 8.4% in early Hong Kong trading on Thursday last week, the biggest intraday gain since February 2025.

BYD first overtook Tesla in the fourth quarter of 2024, and maintained a significant lead through 2025 as Elon Musk’s political activities and close ties with US President Donald Trump disenchanted consumers, particularly in Europe.

However, Tesla retook the lead in the first quarter of this year, outselling BYD by around 48,000 vehicles as softening demand in China dragged down the rival’s sales in its home market.

With China’s auto market entrenched in a fierce price war, BYD is focusing on technology upgrades to compete with rivals like Geely Automobile Holdings Ltd. and Xiaomi Corp.

It is also rapidly expanding the production of its next-generation blade batteries.

A blade battery is a long, flat form factor of lithium iron phosphate (LFP) electric vehicle (EV) battery developed by the automaker BYD. Named for their resemblance to a row of razor blades, they use a “cell-to-pack” architecture that increases structural rigidity and is widely used across the EV industry today

Global EV sales are on track for another record year, though growth in major markets is slowing. In China, the world’s largest market, sales of new energy vehicles — including EVs and plug-in hybrids — fell 7.5% in May from a year earlier.

A Hong Kong fund tied to SK Hynix has grown so large that it’s beginning to move the stock it was built to track.

When Korea’s Kospi index plunged 10% week before last and triggered a tech stock rout that quickly spread across the world, the country’s newfound status as a powerhouse in global markets was evident.

In large part, this is a manifestation of the crucial role South Korean chipmakers SK Hynix Inc. and Samsung Electronics Co. have come to play in the AI boom that’s powering markets higher. The bout of frantic selling that day, which sank the Nasdaq 3%, also spotlighted something else: the emergence of a leveraged exchange-traded fund tied to SK Hynix that has grown so large, so fast, analysts say, that it is magnifying swings in both the stock and the entire Kospi index.

This is something we have talked about often over the years, and nobody seems to mind when an ETF ison the way up, it’s just when it comes down, and comes down hard and fast, that people wake up to the dangers of index tracking (that is based on market cap and not equally weighted) in concentrated markets (found all over the world, including here in RSA and in the US).

In the nine months since the CSOP SK Hynix leveraged ETF (below) was launched in Hong Kong, it has ballooned into a $13 billion fund, the biggest of its kind anywhere, as the chipmaker helped power the Kospi to a nearly 100% gain this year.

On volatile days, the ETF and its smaller peers can account for two-thirds of trading in SK Hynix shares, a staggering figure for a company with a $1.2 trillion market value, forcing banks from Wall Street to Hong Kong to orchestrate a complex web of financing and hedging trades to keep the products running.

So great is this constant drumbeat of buying on up days and selling on down days that investors say the ETF has begun to move the stock rather than simply track it.

It’s a phenomenon popping up more and more across the globe as a rush by investors to turbocharge bets on the AI boom turns leveraged ETFs into a $270 billion business. And as this new financial alchemy ripples through markets, nowhere are the stakes higher than in Seoul, where SK Hynix accounts for 28% of the Kospi index (and rival Samsung another 29%) and increasingly serves as a global barometer to measure AI bubble angst.In other words, selloffs in the CSOP SK Hynix ETF, if sustained long enough, could unleash even more pain. Last Thursday delivered another reminder of that risk: The ETF plunged more than 20%, just as it had done early last week, helping drag the stock down over 10% and triggering a 2% slump in MSCI’s benchmark emerging-market index.

Author: Dawn Ridler

Last week I had the privilege to listen to quite a few people talking about consciousness. Of particular interest is how consciousness relates to AI and visa versa.

As a start, consciousness is the state of being aware of yourself and your surroundings. Ironically, this is how AI defines an attribute which is uniquely human. It’s our consciousness which allows us to frame our lives and how we respond to others. Tone and expressions are learnt. It’s these things which allow us to frame responses so as not to offend or to achieve a certain goal. I find our level of consciousness is really important to exist successfully on planet earth and gives our lives the nuance which makes every day exciting. I watched children interact last week. Their facial expressions were about the joy of discovering new objects and attributes they did not know before, or perhaps did not know fully. This is learned, and their level of consciousness should increase as they continue along the path of their lives. Consciousness requires not only your left brain but also your right. It’s the ability to merge IQ with EQ, and how those two meet gives us our own special level of consciousness.

AI is able to give us outcomes based on all known public information about literally any subject.

This is an amazing tool. Its ability to transcend head knowledge and to combine the knowledge of many different sources, to ultimately dish up this information in an application. It’s something only our forefathers could have dreamt about. But for all its amazing achievements, AI continues to be a left-brain activity. You ask the question and it delivers an answer. No nuance or feelings … there is no consciousness in AI.

But does this matter?

If our purpose for AI is to be an assistant or information source, the issue of consciousness isn’t really that important. This is because this information will be interpreted and used by a human, who will then add the right-brain experience for the real world. But if the founders of AI are to be believed, they are dreaming of a world where AI isn’t just AI but superintelligence. This is the world where AI becomes autonomous and starts thinking for itself. This is the part of AI most people fear as it would not only lead to massive job losses but could rewire the world as we know it.

If consciousness is about our awareness, then morality is embedded in us. It helps us discern what is right and wrong and what is required of us in society. It’s pretty important stuff, but it’s often overlooked. Morality is something which we are partly born with, but is also learned through our interaction with society. Superintelligence can have a moral compass, but it would be a collective moral compass of all its inputs. And this can be manipulated. Let’s look at an example.

We would all agree that mass murder is wrong.

Our morality would kick against it, and our consciousness will give it the dubious context it deserves. The human experience will raise serious red flags. But what if mass murder is ultimately for the good of society? Is this right or wrong? It’s conceivable that a superintelligence, acting on the combined instructions of its inputs, could condone it. It’s all about how robust the inputs are. Manipulate these, and the outcomes change. But if we consider mass murder as individuals, there should be no justification … it’s wrong on every level. And this is the problem with superintelligence today, especially when it has the ability to weaponise. For now, much of AI is still in development. The next phase is going to be a capital hangover as the Dollars spent on AI aren’t all going to yield the returns that were hoped for. But once this has passed, a narrower group of AI players will emerge who will need to hammer out the details of how autonomous AI really can be. It will probably take a disaster somewhere for regulators to start imposing rules. They no doubt will use their own consciousness to give them the context needed to shape superintelligence.

Author: Cobie Le Grange

EXCHANGE RATES and other Indices:

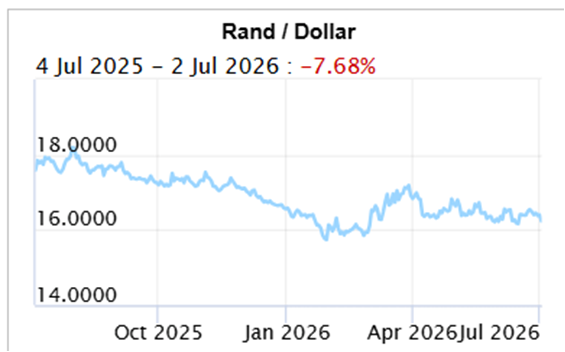

The Rand/Dollar closed at R16.22 (R16.40, R16.39, R16.27, R16.55, R16.23, R16.46, R16.68, R16.39, R16.63, R16.29, R16.41, R17.07, R17.06, R16.89, R16.55, R15.93, R16.01, R15.96, R16,03, R16.15, R16.10, R16.50, …R16.91, R17.13, R17.36, R17.13,16.52 )

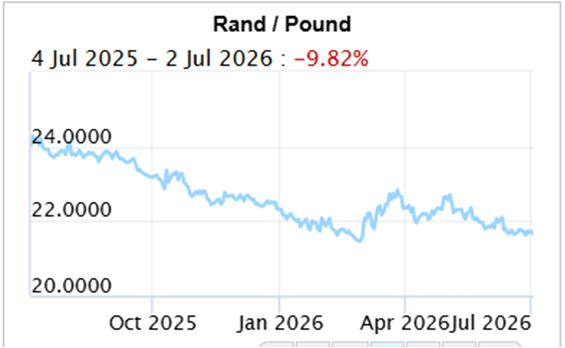

The Rand/Pound closed at R21.64 (R21.64, R21.67, R21.80, R22.06, R21.80, R22.09, R22.21, R22.30, R22.56, R22.35, R22.02, R22.09, R22.77, R22.76, R22.35, R22.20, R21.48, R21.59, R21.78, R21,82, R22.11, R21.97, R22.13, …R22.57, R22.68, R22.74, R22.56,

The Rand/Euro closed the week at R18.52 (R18.66,R18.89, R19.16, R19.08, R18.91, R19.11, R19.38, R19.29, R19.48, R19.37, R19.17, R19.24, R19.70, R19.77, R19.33, R19.23, R18.80, R18.87, R18.94, R18.93, R19.14, R19.04, R19.20)

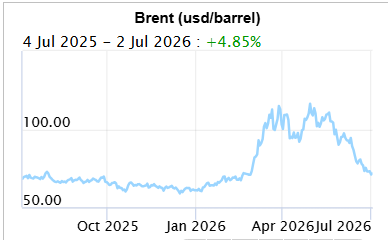

Brent Crude: Closed the week $72.10 ($71.99, $80.59, $87.33, $93.09, $91.12, $104,24, $109.26, $101.29, $108.83, $105.33, $90.38, $95.20, $107.88, $112.36, $103.14, $92.88, $73.19, $71.76, $67.75, $68,05, $69.32, $65.88, $63.34, …$63.71, $63.19, )

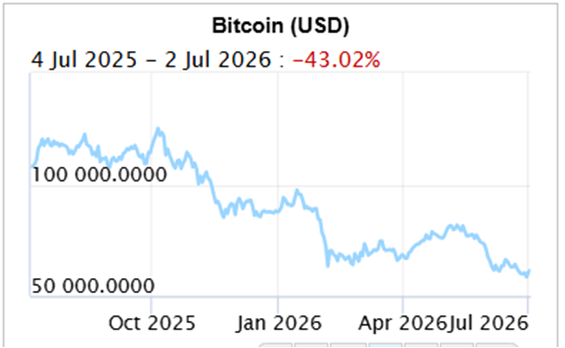

Bitcoin closed at $62864 ($60,063, $64,029, $64,131,$60,762, $73,788, $74,559, $77,879, $80,733, $78,204, $78,049.98, $75,519, $70,904, $68,691 , $68,586, $70,869, $67,310, $63,534, $68,04, $69,649, $68,553, $81,301, $89,295, $90,585,)

Articles and Blogs:

Investment series part 1 (NEW)

Investment series part 2 (NEW)

Legacy Series Part 4

Legacy Series part 3

Legacy Series Part 2

Legacy Series Part 1

Holiday checklist

Next year – Action Plan

Next year – Vision, Mission etc

Medical Risk Mitigation

Next Year – Consolidation

Abdication or diversification?

Carbo-loading your retirement Spoiled for choice

Who needs a plan anyway

8 questions you need to ask about retirement

What to do when interest rates drop

How to survive volatility in your investments

What to do when interest rates drop

Difficult Financial Conversations

Financial Implications of Longevity

Kick Start Your Own Retirement Plan

You matter more than your kids in retirement

To catch a falling knife

Income at retirement

2025 Budget

Apportioning blame for your financial state

Tempering fear and greed

New Year’s resolutions over? Try a Wealth Bingo Card instead.

Wills and Estate Planning (comprehensive 3 in one post)

Pre-retirement – The make-or-break moments

Some unconventional thoughts on wealth and risk management

Wealth creation is a balancing act over time

Wealth traps waiting for unsuspecting entrepreneurs

Two Pot pension system demystified

Cobie Legrange and Dawn Ridler,

Rexsolom Invest, Licensed FSP 45521.

Email: cobie@rexsolom.co.za, dawn@rexsolom.co.za

Website: rexsolom.co.za, wealthecology.co.za