Too Busy? Got Better Things to Do? Read the Summary…

Good news for RSA Inc? Bank chief economist Goolam Ballim sees South Africa’s economy gaining momentum as electricity, ports and rail fixes start paying off, forecasting 1.7% growth next year and 2% in 2028. Separately, Justice Malala’s piece on anti-immigrant violence highlights reputational and economic risks, urging stronger AU leadership to address root causes of migration.

Fed Independence, an update: The Supreme Court split on independent agencies: it ruled the president can fire FTC members at will, but blocked the attempted removal of Fed governor Lisa Cook. The rulings sit in tension, with Justice Barrett noting as much in dissent. Central bank independence remains critical for market confidence, though the protection looks tentative rather than settled.

Sigh, On again: Renewed Iran-Israel-US hostilities sent oil sharply higher after Iran struck shipping in the Strait of Hormuz and President Trump declared the ceasefire over. Markets’ reaction has been muted rather than shocked, since the key questions (Strait closure and ground escalation) still look unlikely to turn worse. Expect oil to settle higher than prewar levels, with AI spending remaining the bigger market driver.

Inflation, emerging markets under pressure: The Fed’s hawkish tone under new chair Kevin Warsh reflects concern that AI demand, Middle East tensions and tariffs will keep inflation elevated. Emerging markets, particularly energy importers like India, are feeling the strain through weaker currencies and higher bond yields. South Africa faces a modest impact from imported inflation, though the broader picture remains one of muddling through rather than a crisis.

Monetising AI: Token prices have fallen more than 90% since 2023, even as AI and data centre order backlogs stretch out to nearly three years. Hyperscalers are pouring cash into capex, narrowing their valuation edge over old-line industrials, while chip stocks look due for a correction. Longer-term, AI’s productivity gains look real but uneven, with adoption shaped by cost, capacity and demand elasticity rather than by a smooth, universal rollout.

Quality under fire: Fundsmith’s Terry Smith is adapting his quality-investing approach after GBP11.5 billion in outflows over three years, as momentum, rather than valuation, now drives markets. Adobe illustrates the problem: strong EBITDA and free cash flow growth hasn’t stopped a 40.9% share price decline over the past year. The takeaway is that quality investing still holds, but needs sharper judgement on which companies qualify, alongside more attention to index-level liquidity dynamics.

This Week’s Roundup

I came across this good news story on Bloomberg – I won’t rehash it, you can read it in full here, but in summary:

Standard Bank chief economist Goolam Ballim says South Africa’s economy is gaining momentum as fixes to long-standing governance and infrastructure bottlenecks — notably in electricity, ports and rail — begin to pay off; he forecasts growth of 1.7% next year and about 2% in 2028, stronger than the IMF’s outlook, and argues that improving the rule of law(highlighted by the Madlanga Commission probe) should boost investor confidence and lift growth across southern Africa.

Then there was another interesting, but not so good news story on the illegal immigrant situation by Justice Malala:

South Africans’ violent anti-immigrant protests — led by the new group March and March and echoed in attacks on homes and businesses — represent a sharp betrayal of the continent that once sheltered and supported the anti-apartheid struggle, damaging South Africa’s reputation and risking economic retaliation; while leaders and commentators rightly condemn the xenophobia, they also urge African governments to confront the root causes driving mass migration (authoritarianism, kleptocracy, poverty and conflict) and to revive collective accountability through stronger AU leadership and enforcement of agreements like the Lomé framework (since replaced) to reduce refugee flows and restore regional solidarity.The Lomé Framework refers to the system of trade, aid, and cooperation created under the Lomé Conventions (1975–2000) between the European Economic Community (EEC) and African, Caribbean, and Pacific (ACP) countries. It provided non-reciprocal trade preferences, duty-free access for most ACP exports, and large development funding through the European Development Fund. It also introduced stabilisation schemes (STABEX and SYSMIN) to protect ACP countries from volatile commodity prices. The framework shaped ACP–EU relations for 25 years before being replaced by the Cotonou Agreement in 2000.

The Supreme Court has recognised the Federal Reserve as a special case among the government’s numerous independent agencies — one that requires protection from White House interference. The distinction is less than clear-cut in legal terms. As a practical matter, however, preserving the central bank’s independence in monetary policy is considered vital.

Last week, the six conservative justices united against the court’s three liberals in finding, in effect, that the president can fire members of the Federal Trade Commission (and, it follows, most other independent agencies) at will. At the same time, the liberals plus Chief Justice John Roberts and Justice Brett Kavanaugh voted to block the president’s attempt to sack Lisa Cook, a Fed governor, “for cause.”

As Justice Amy Coney Barrett noted in her dissent regarding the Fed, the two decisions appear to be “in serious tension.” If the very idea of independent agencies violates the constitutional separation of powers, as the FTC ruling contends, what makes the Fed so special? And if the answer is that exposing the Fed to political pressure would cause great harm, why shouldn’t that factor carry the same weight when it comes to other agencies?

Rather than resolving such questions, the court has swerved around them. In the FTC case, the court found that agencies, once created by Congress, are part of the executive and not a fourth branch of government. As such, they’re accountable to the president, and hence to the electorate. In the second, the majority focused less on the harm that denying Fed independence would cause than on strained historic understandings about “national banks” and procedural defects in the administration’s efforts to get its way.

It seems that Roberts, author of both opinions, has tried once again to strike a balance between the conservatives’ understanding of strict constitutional propriety and real-world consequences. Time will tell whether placing the FTC and other bodies more squarely under the president’s thumb will be to the nation’s advantage.

If technical experts are replaced by incompetent partisans at agencies that regulate election financing, the environment, food safety and other critical issues, the risks of disruption or worse are clear. Congress could supply the remedy by exerting more control and passing less ambiguous laws for agencies to implement, but lately it’s shown no such capacity.

In the meantime, though, there’s no question about the harm that putting the Federal Reserve in any such subordinate position would cause.

The evidence is overwhelming that central bank independence in the conduct of monetary policy is indispensable — so overwhelming, in fact, that few politicians any longer challenge the idea. They know that destroying the central bank’s credibility would immediately alarm investors, cause long-term interest rates to spike in anticipation of higher inflation, and trigger financial instability. They also know that this would work against their own short-term (Trump isn’t going to be around forever, and Supreme Court judges have lifetime terms – so far) political interests.

Worryingly, it seems that support for this principle can no longer be taken for granted in the US. And regarding the Fed, the court has granted a reprieve at most. The administration didn’t assert a right to dictate Fed policy, only to fire governors for serious misconduct. The block on Cook’s removal pending further litigation leaves that question open. Statutory defences of Fed independence and accountability to Congress might ultimately be required. For now, even strained, tentative and untidy judicial protection is something to celebrate.

The umpteenth renewal of hostilities between Washington and Tehran has sent oil surging by the most since April. At the time of writing, Brent crude is trading at $75.59, but has gone over $80 in the last week. Overall, markets’ reaction feels jaded. This is not a major turning point, and the latest events aren’t so much shocking as distressing for economies that had hoped that the truce laid out in last month’s Memorandum of Understanding would hold.

It seems to have been more of a Memorandum of Misunderstanding.

Broadly, events in the Middle East matter to markets only to the extent that they affect the oil price. The deeply controversial situation in Gaza, for example, has barely had any financial impact as it doesn’t call oil supply into question.

In the Iran conflict, we will be looking at the following:

The market sold off aggressively in March when it turned out that the answer to the first question was “yes.” The turnaround at the end of that month was prompted by clear evidence that the US was determined not to escalate into a ground conflict (and so the answer to the second question was “no”). That’s been followed in recent weeks by what now looks like an overreaction to the Memorandum of Understanding as a virtual peace treaty, rather than the pause it barely was, and its likely effect on the Strait.

The risk of an escalation involving ground troops seems as slim as ever. President Donald Trump said in Ankara that this would be a “waste of time.” His reluctance to risk American lives keeps the conflict’s overall risks manageable for markets, while ensuring that volatility for those most affected will persist, as the US is not prepared to deter Iran from flexing its muscles in the Gulf.

That entails a non-disaster scenario in which oil prices stabilise significantly higher than at prewar levels. What has been most surprising in the last few weeks has been the scale of their fall, even as movement through the Strait remains limited.

Thus, when things go wrong, as in the last few days, oil prices need to rise again, and other assets need to fall. But the broader binary approach continues: This is not going to lead to destruction and death on the scale of Iraq or Vietnam, and the scope for market damage is limited. While risks of geopolitical disaster remain contained, the immense amounts of money being spent on AI will continue to move markets more. Paying too much attention to macro risks, consuming a lot of energy without requisite returns, appears to be one of the lessons of the Iran conflict so far.

Inflation – Emerging markets under pressure

Only days ago, the discussion around oil supply had shifted to an imminent glut as producers opened the spigots after the Strait reopened. That left inflation expectations significantly lower than they had been on Feb. 27, the eve of the war.

Elevated inflationary pressures had already prompted a hawkish stance from the new leadership at the Federal Reserve. The minutes of the first Federal Open Market Committee meeting chaired by Kevin Warsh, released last Wednesday, made clear that the war was putting upward pressure on rates. A “few” members even saw a case for a hike last month.

Most participants pointed to scenarios in which, under stable labour market conditions, inflation would remain elevated due to strong AI-related demand, the conflict in the Middle East, or the effects of tariffs. In such scenarios, almost all of these participants indicated that some policy firming would likely be warranted.

Emerging Markets response to renewed tensions

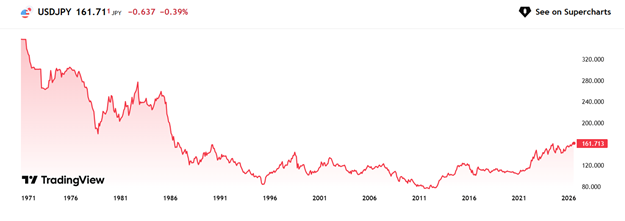

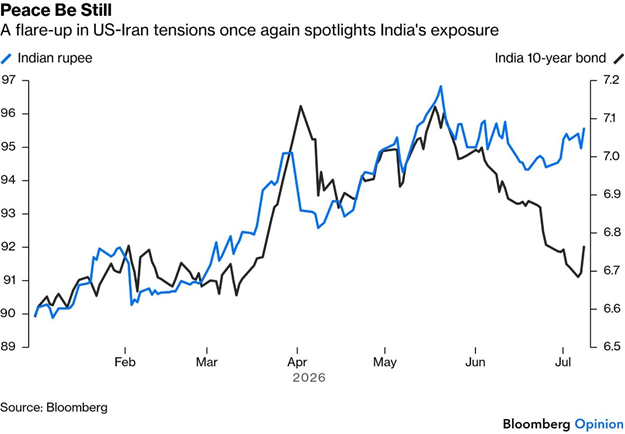

That complicates monetary policy for emerging markets. For countries like India, precariously exposed to the energy shock, the renewed fighting was felt almost instantly. Trump’s declaration that the ceasefire was over sent the rupee tumbling to a month low, as Indian bond yields rebounded:

Trump’s threat of further strikes, irrespective of whether they’re carried out, means that debilitating uncertainty for countries that depend on Middle East oil will continue.

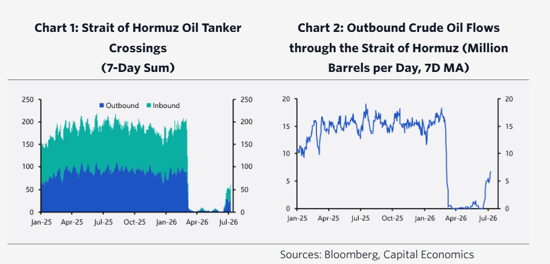

The best scenario would be a messy ceasefire that allows oil flows to increase while crude prices settle around the $80 per barrel mark — still more than 30% up from the start of the year ($60).

This is partly because the exodus of oil-laden tankers that had been trapped in the Strait for months accounts for some of the recent increase in oil flows, and so loadings would need to rise further to sustain the current rate of oil flowing out of the Strait.

There could even be bigger troubles should Iran further restrict traffic through the Strait and/or the US reinstate its naval blockade of Iranian ports. A return to prewar levels quickly was always unlikely, and the renewal of hostilities will likely keep it that way. But the recovery seen in recent weeks has been meaningful.

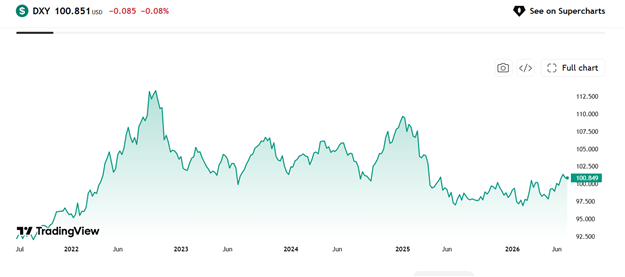

The return of risk provided a tailwind for the strengthening dollar. Emerging-market currencies had been the conspicuous victims of the Iran conflict, which snuffed out an impressive rally.

Imported inflation is a big problem for RSA.

The import price shock will have a moderate long-term impact of around 0.4% on the median Central and Eastern Europe and Middle East and Africa economies and a much more modest 0.1% impact on Latin America and Asia. Persistence could be lower than history suggests. All of this tends to confirm why the market reaction has been jaded rather than shocked. A return to hostilities is undeniably bad news, but most of the world has shown that it can muddle through.

Amid the ever-growing array of metrics of the artificial-intelligence boom, one relatively useful, straightforward measure tracks how much is being spent on large language models. Why not just count the total number of tokens — the tiny packets of data that are the building blocks of AI models — people buy to use them? It’s as close to an AI currency as we currently have, and while it might not ultimately prove the best gauge of the technology’s trajectory, it’s a real-time gauge of AI companies’ pricing power.

There appears to be a shift in demand toward cheaper models, or a softening in how much buyers are willing to pay. The price of a single token had plunged by more than 90% since 2023.

The big news is that the order backlogs for AI and data centre-related companies surged to nearly a three-year backlog, so the data centre boom is expected to persist at least through 2029.

Investors looking to find AI winners will ultimately gravitate toward hyperscalers such as Microsoft Corp. (currently down 28% from the all-time high it set last October), Amazon.com Inc., and Meta Platforms Inc., given the strength of their core businesses. Virtually all of the cash these companies produce is now going to capital expenditures (meaning chips).

As investors have grasped that these companies now depend on capital as much as old-line industrials, eliminating a key perceived advantage that the tech sector has enjoyed for decades, so their shares have stalled. Attention has naturally turned to the massive sums they have to pay to the chipmakers.

Chips’ momentum will fade as investors grow increasingly wary of their ballooning valuations, rising competition, and potential overcapacity, and remember the potential payoff from massive AI investments for hyperscalers.

I expect the hyperscalers now to stabilise; that’s what’s been going on in the last couple of weeks, and the semiconductor stocks are going to correct… That’s a good development. You can’t have this divergence continue; it’s not sustainable.

The likelihood remains that AI will positively affect productivity, which should ultimately drive the technology’s attractiveness — even if competition pushes down prices for cost-sensitive consumers.

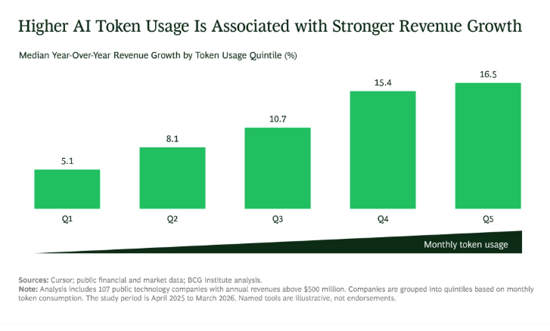

A recent Boston Consulting Group paper by Matthew Kropp and his team analyzed token consumption at more than 100 public technology companies with more than $500 million in trailing 12-month revenue. It concluded that tokens multiply what knowledge workers can produce, much as the assembly line did for manufacturing.

The firms pulling ahead are redesigning their processes around AI, with people applying expertise to direct and improve the system. These companies operate at a pace and scale that human-only organisations cannot match.

Ultimately, they find that if the winners get it right, they’ll create workflows that improve organically as AI becomes better, faster, and cheaper, and the rewards could be significant.

For all AI’s promise, the path to realising significant productivity improvements isn’t straightforward. The journey will be more selective and cost-conscious than markets once assumed.

The key variable is not productivity alone but the elasticity of demand for the tasks and services whose costs are falling. Where demand is elastic, AI-enabled efficiency gains can expand output enough to raise demand for complementary factors of production, such as labour.

Over the medium term, improvements in model efficiency and power infrastructure can offset some of today’s physical constraints. Markets, however, should avoid anchoring themselves to a world in which AI is ubiquitous, frictionless, and immediate, even though that is close to what eventually happened after the introduction of the internet. Ultimately, a more plausible path is one of uneven diffusion: Frontier deployment concentrated where the returns justify the computing power, broader adoption shaped by cost and capacity, and asset prices periodically forced to reconcile ambition with physical constraints. Put differently, the period of vertical ascent is probably over.

Author: Dawn Ridler

Probably the front runners in quality investing are a UK-based fund management outfit called Fundsmith. Terry Smith who is the founder of the business is a vocal supporter of the understanding of quality companies and their long-term compounding properties driven by their ability to drive free-cash flow and return’s on invested capital. This is something which has made Terry Smith both famous and wealthy. The problem that he faces today is that this style of investing is out of vogue, having been replaced by money chasing the AI race and the companies which are investing in this space.

Fundsmith’s latest quarterly letter to investors is telling. With GBP11.5 billion having left the fund in the 3 years to June and GBP3.8 billion in the first half of the year these outflows at some point start becoming critical to the longevity of the outfit. At what point does it become the “hill on which this management business dies”? To deal with this, Mr Smith has decided to adapt his strategy. He talks about how the market today is momentum-driven and that valuation has taken a back seat. This is arguably one of the toughest periods for fund managers who rely on valuation to drive future returns. He further manages open-ended funds, which means investors can ask for their money today and expect it tomorrow. If, for three years, one has seen the outflows that he has experienced, one is battling the forces of rebalancing all the time to facilitate the liquidity required for the outflows. No easy task.

In the past, quality investors, who we purport to be, could rely on valuation as a good signifier of future returns. As Mr Smith says, when these companies hit a glitch, this becomes a buying opportunity. But many of these opportunities are just not yielding the desired results. Take Adobe as the poster child:

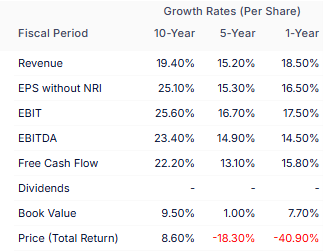

Adobe Incorporated Here is a company which has grown its EBITDA by 23.4% p.a over the last decade. It takes just over 4 years for this business to double in size. This is no small feat! At the same time, free cash flow has grown by 22.2% p.a. Now look at the shape price… 8.6% p.a. This business continues to be a head-scratcher and one we have owned and debated many times over. You can find many reasons for the share price weakness today, but what stands out to me is how it is being punished even if you believe that AI will change its business model somewhat. Note the -40.9% return in the last year! And this is what Mr Smith is talking about when he says that “In order to finish first, you must first finish” So the choices for a fund manager is stark. Do nothing and hope the market agrees with you sometime soon, or adapt. I choose adapt.

This doesn’t mean one has to abandon quality investing. It merely means that one has to become more circumspect as to what is included. Valuation alone won’t save the day. Some time needs to be spent on understanding the “why” and “how” of a quality company. The second thing to consider is that the indices have become a real risk to ignore. Yes, these can fall in value when AI is out of vogue. But what if global liquidity is the main driving force for the level of the index and can be switched on by policymakers in a heartbeat? And then consider that many of the hyperscalers are actually profitable organisations with large cash flows…. I exclude Starlink here, which is really just an idea stock. These companies aren’t going to go bust as was the case with many players in the Dotcom bubble. So active management today should at least consider the index.

Author: Cobie Le Grange

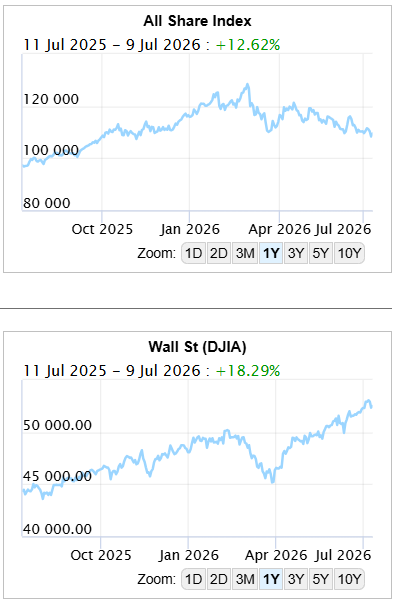

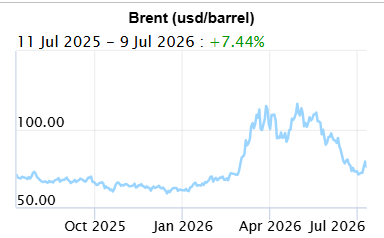

EXCHANGE RATES and other Indices:

The Rand/Dollar closed at R16.31 (R16.22, R16.40, R16.39, R16.27, R16.55, R16.23, R16.46, R16.68, R16.39, R16.63, R16.29, R16.41, R17.07, R17.06, R16.89, R16.55, R15.93, R16.01, R15.96, R16,03, R16.15, R16.10, R16.50, …R16.91, R17.13, R17.36, R17.13,16.52 )

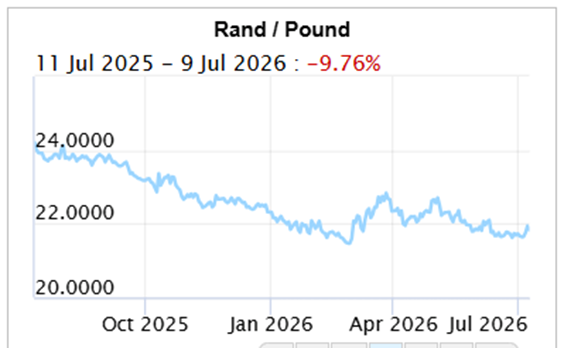

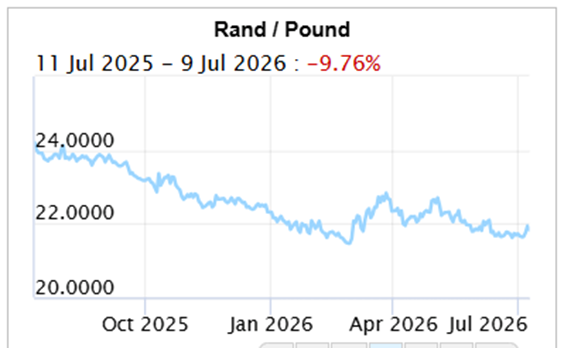

The Rand/Pound closed at R21.86 (R21.64, R21.64, R21.67, R21.80, R22.06, R21.80, R22.09, R22.21, R22.30, R22.56, R22.35, R22.02, R22.09, R22.77, R22.76, R22.35, R22.20, R21.48, R21.59, R21.78, R21,82, R22.11, R21.97, R22.13, …R22.57, R22.68, R22.74, R22.56

The Rand/Euro closed the week at R18.62 (R18.52, R18.66,R18.89, R19.16, R19.08, R18.91, R19.11, R19.38, R19.29, R19.48, R19.37, R19.17, R19.24, R19.70, R19.77, R19.33, R19.23, R18.80, R18.87, R18.94, R18.93, R19.14, R19.04, R19.20)

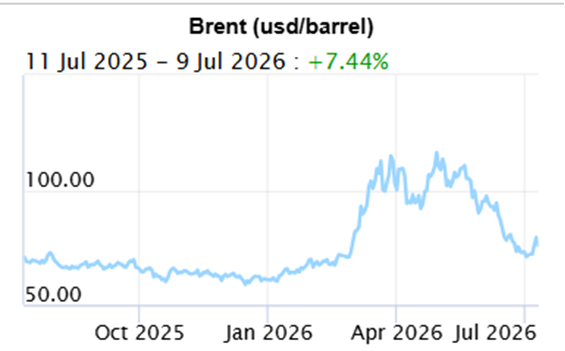

Brent Crude: Closed the week $76.01 ($72.10, $71.99, $80.59, $87.33, $93.09, $91.12, $104,24, $109.26, $101.29, $108.83, $105.33, $90.38, $95.20, $107.88, $112.36, $103.14, $92.88, $73.19, $71.76, $67.75, $68,05, $69.32, $65.88, $63.34, …$63.71, $63.19, )

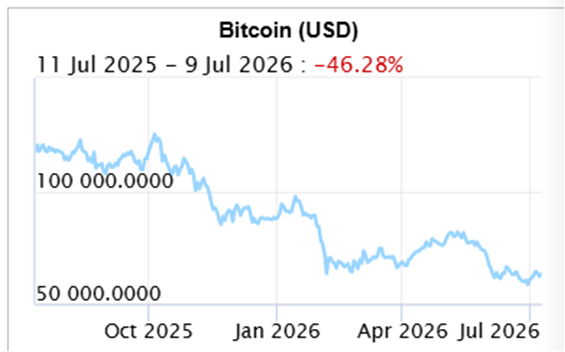

Bitcoin closed at $63,815 ($62864, $60,063, $64,029, $64,131,$60,762, $73,788, $74,559, $77,879, $80,733, $78,204, $78,049.98, $75,519, $70,904, $68,691 , $68,586, $70,869, $67,310, $63,534, $68,04, $69,649, $68,553, $81,301, $89,295, $90,585,)

Articles and Blogs

Investment series part 1 (NEW)

Investment series part 2 (NEW)

Legacy Series Part 4

Legacy Series part 3

Legacy Series Part 2

Legacy Series Part 1

Holiday checklist

Next year – Action Plan

Next year – Vision, Mission etc

Medical Risk Mitigation

Next Year – Consolidation

Abdication or diversification?

Carbo-loading your retirement

Spoiled for choice

Who needs a plan anyway

8 questions you need to ask about retirement

What to do when interest rates drop

How to survive volatility in your investments

What to do when interest rates drop

Difficult Financial Conversations

Financial Implications of Longevity

Kick Start Your Own Retirement Plan

You matter more than your kids in retirement

To catch a falling knife

Income at retirement

2025 Budget

Apportioning blame for your financial state

Tempering fear and greed

New Year’s resolutions over? Try a Wealth Bingo Card instead.

Wills and Estate Planning (comprehensive 3 in one post)

Pre-retirement – The make-or-break moments

Some unconventional thoughts on wealth and risk management

Wealth creation is a balancing act over time

Wealth traps waiting for unsuspecting entrepreneurs

Two Pot pension system demystified

Cobie Legrange and Dawn Ridler,

Rexsolom Invest, Licensed FSP 45521.

Email: cobie@rexsolom.co.za, dawn@rexsolom.co.za

Website: rexsolom.co.za, wealthecology.co.za